The long-awaited Indonesia's tax amnesty bill was finally passed by the parliament on Tuesday, 28 June 2016. The new tax amnesty scheme will apply from July 2016 until the end of March 2017, with a recent government announcement clarifying that the Bill will only take effect after Hari Raya Puasa, which falls on 6 and 7 July.

The new tax amnesty provides a waiver of tax dues, administrative sanctions, and tax crime sanctions if the taxpayer makes redemption payment as stipulated by the legislation.

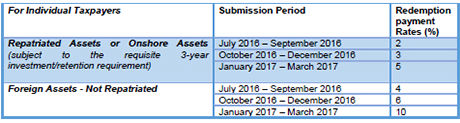

Redemption payment rates

The redemption payment rates for declared assets/funds

repatriated back to Indonesia are: 2% for declaration done before

end of September 2016, 3% before end of December 2016 and 5% before

end of March 2017, and the redemption payment rates for declared

assets which continue to be maintained overseas are 4%, 6% and 10%,

for the same corresponding 3-monthly period.

The announced rates of 2% to 10% are higher than the proposed rates

under an earlier bill where the proposed rates then were 2% to

6%.

The Bill passed also clarifies that the lower rates of 2% to 5% are

applicable not only to foreign assets remitted back to Indonesia

but also assets currently within Indonesia provided that the

applicant commits to retaining such assets within Indonesia for at

least the next 3 years.

There is also an expanded list of assets that the remitted funds

must be invested in for at least 3 years after repatriation. Other

than Government securities/State Owner Enterprise bonds, it also

includes private company bonds the trading of which is supervised

by the Financial Services Authority, certain infrastructure

investments effected through government cooperation with business

entities, and certain real estate investments based on priorities

set by the government through a separate MoF Decree and other

investment forms. Further announcements on the range of permitted

investments will therefore have to be made to elaborate on this

list and this will impact on the rate of repatriation of declared

funds. Remittances have to be done by 31 Dec 2016 for taxpayers

seeking the 2% and 3% rates and by 31 March 2017 for the 5%

rate.

Applicable Rates Summary Table:

Tax Amnesty application & procedure

To apply for the tax amnesty, the applicant must submit a

Declaration Letter disclosing the net value (assets minus

liability) of the under-declared assets (ie assets not declared in

their last income tax return for year 2015. The applicable

redemption payments are computed by multiplying the relevant rate

and the net value of the additional assets declared. Each applicant

is allowed to submit not more than 3 separate Declaration Letters

up to 31 March 2017.

There is however a limitation on deductible debt for the purpose of

determining the net value. For an entity taxpayer the debt must be

no greater than 75% of the value of the additional assets and for

an individual the limit is 50%.

The amnesty terms also require the applicant to settle all assessed

tax arrears, to withdraw requests relating to outstanding tax

objections/appeals and to make full payment of the redemption

payment. It also specifies that the taxpayer must submit the latest

tax return and a detailed list of assets together with information

on the ownership of the assets that are reported.

For taxpayers with foreign trusts, foundations or holding entity

structures with professional nominees in place, it will be

important to have more clarity and confirmation on what constitutes

sufficient information on the ownership of the assets held through

such foreign structures, in order to avoid future disputes on the

completeness of their submitted declarations.

It is provided that the Minister or his appointed official shall

issue a Tax Amnesty Certificate within 10 working days from the

date of receipt of the completed application with attachments. If

the applicant does not receive such a Certificate within the

promised 10-day period, then the Declaration Letter itself shall be

deemed to be received as a Certificate. With such Certificate, the

applicant is then entitled to the indemnity against tax audits and

investigations for tax offences under the terms of the amnesty. For

taxpayers who have already been subject to on-going tax audits or

investigations, such process must also cease upon receipt of the

Certificate.

However if it should be discovered subsequently that data or

information were not completely disclosed in the Declaration Letter

then additional taxable income (with applicable penalty) could be

deemed to have been received or earned by the taxpayer at the time

of such discovery. Clarity on what constitutes complete disclosure

for the amnesty application purposes is therefore important to

avoid lingering negotiations and disputes.

The amnesty also requires taxpayers to transfer title in any

declared land, building and/or stocks back to the name of the

taxpayers. Such title transfer shall be exempt from Indonesia

income tax if the application for transfer of rights/title is done

by 31 December 2017 or in the case where the title cannot yet be

transferred, then a notarial statement done before 31 December 2017

stating that the assets is truly owned by the taxpayer.

The taxpayer should therefore understand the full legal and tax

implications not only in but also outside Indonesia in connection

with the unwinding of any foreign holding (and also local nominee

holding) structures.

If the assets are retained in foreign holding structures, the

continuing Indonesia tax exposure on such assets may be higher than

holding the assets directly through Indonesia holding company or in

individual names. The applicability of the Indonesia's

Controlled Foreign Corporation (CFC) laws and the deemed domiciled

and permanent establishment rules will depend on the ownership and

management of the assets and structures. If the foreign holding

structures are only unwound beyond the above specified period, then

the taxpayer will have to factor in the additional Indonesia tax

costs for doing so.

The tax amnesty only includes obligations of income tax, value

added tax and sales tax on luxury goods up to 31 December 2015. If

any income or gains have accrued this year (whether due to current

year restructuring, transfers or receipts not otherwise producing

tax exempt income/gains) then such income and gains would not

appear to fall within the scope of the amnesty.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]