On 22 December, 2014 the Basel Committee on Banking Supervision (BCBS) published a consultation paper on "Revisions to the standardised approach for credit risk"(CRSA) 1. The aim of the revised CRSA as proposed by the BCBS is to tackle weaknesses in the current approach, including:

- over-reliance on external credit ratings;

- lack of granularity and risk sensitivity;

- out-of-date calibration;

- lack of comparability across different banks and jurisdictions; and

- misalignment of treatment between the current CRSA and exposures risk weighted under the internal ratings based (IRB) approach.

The CRSA is relevant to all banks, including those using IRB approaches. This is because the proposal for the revised CRSA, once finalised, will be used to calculate a new capital floor for IRB banks. As a result IRB banks need to be able to calculate the CRSA as well. The BCBS is also consulting on revisions to the standardised approaches for market and operational risk as part of its efforts to reduce variability in risk weighted assets (RWAs). Once the new standardised approaches to credit, market and operational risk have been agreed, the new floor will be calibrated. This is expected around the end of 2015.

Overview of the revised CRSA

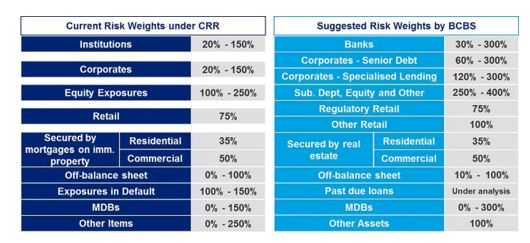

The key feature of the proposed new CRSA is the replacement of the use of external ratings with other risk drivers that vary for each exposure class covered in the consultation 2. Table 1 provides an overview of exposure classes and proposed risk drivers. Risk weights (RWs) for each exposure class are determined based on mapping tables for each risk driver defined in the consultation. It is striking, that RWs may change significantly for some exposures. RWs range between 0% and 400% compared to the current range of 0-250% (see Table 2).

At the same time, the BCBS is introducing more granular exposure classes to the CRSA. In many cases a one-to-one mapping of current exposure classes to the proposed exposure classes is not possible. Additional criteria have been defined by the BCBS to categorize the exposures to the new exposure classes that will require changes to banks' IT systems.

In addition, the BCBS is also proposing changes to credit risk mitigation (CRM) techniques under the CRSA. The range of permitted CRM techniques is reduced and the supervisory haircuts are recalibrated. Increases in net exposures and RWAs will most likely be the result.

Implications of the proposed approach

The revised CRSA, if adopted in its current form, will have a significant impact on the banking sector. Not only could RWAs increase significantly under certain circumstances, but volatility of RWAs could also increase if the proposed risk drivers are more sensitive to the economic cycle than external ratings were. This will have a particular impact on portfolios largely consisting of unrated borrowers.

Even though the proposed risk weights could be higher than under the current approach, the BCBS states that the goal of the revisions is not to increase overall capital requirements. A recalibration of the proposed CRSA is therefore possible. In order to derive a better understanding of the impact of the proposal, a quantitative study (QIS) is planned based on end-2014 data. The QIS could be challenging because many banks currently do not store all the required data on proposed risk drivers systematically, nor will they always be able to source the data easily.

The consultation should be seen from a strategic viewpoint and in the broader context of the changes to the other standardized approaches and proposed the new capital floor. The profitability of certain portfolios may be reduced and banks need to adapt their capital planning and strategy accordingly. The revised CRSA is one more building block banks need to consider when managing their balance sheets in a world of multiple constraints.

Changes to IT systems and processes will also be needed. Early consideration needs to be given to future data capture and maintenance responsibilities to feed into the process design. Timely data availability will be crucial as the BCBS proposes to apply a risk weight of 300% in cases where the required data are not available.

The proposed approach increases complexity relative to the status quo – considerations of "simplicity", so prevalent 18 months ago, seem now to have taken a back seat. However, even so it is not clear if the proposed risk drivers that only contain information on past performance can fully explain the borrower's risk. For example, looking at bank exposures, the RW is determined by the CET1 ratio and the Non-Performing Assets (NPA) ratio. However, neither provides insights into the borrower's liquidity situation. Moreover, using the disclosed "headline" CET1 ratio as the risk driver takes no account of differences in Pillar 2 capital requirements. Two banks with the same reported CET1 ratio may have very different underlying risk profiles. At the same time it is not clear that the new approach will deliver consistent application across the world. As the BCBS itself has noted, the implementation of the Basel framework can vary across jurisdictions: the EU and the US have recently been given "materially non-compliant" and "largely compliant" ratings respectively3.

Next steps

The BCBS recognizes that the proposal is still at an early stage of development. Given the complexity of the topic, and the openness of some aspects of the consultation (itself indicative of possible differences in views among BCBS members), various iterations of the new CRSA could be needed.

The consultation ends on 27 March, 2015. The BCBS has not yet put forward an implementation timeline. However, it is expected that there will be a clearer picture on the broader set of initiatives by the end of 2015.

Risk Drivers

Table 1: Overview of proposed quantitative risk drivers

Exposure classes and risk weights

Table 2: Overview of current and proposed exposure classes and risk weights

Note: The table above does not show a mapping of exposure classes but provides a lit of current and proposed exposure classes and risk weight.

Footnotes

(1) http://www.bis.org/bcbs/publ/d307.pdf

(2) The consultation paper does not cover exposures to sovereigns, central banks and public sector entities. These will be dealt with in a further review.

(3) http://www.bis.org/bcbs/publ/d300.pdf and http://www.bis.org/bcbs/publ/d301.pdf

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.