Generally effective Jan. 1, 2018, the most sweeping tax reform in a generation (legislation originally known as The Tax Cuts and Jobs Act (the "Act")) requires many managers to determine if they possess the most tax advantageous form of entity. Choice of entity is an often overlooked but crucial corporate task.

As part of the Act, C corporations are now taxed at a U.S. federal income tax rate of 21%, which was reduced from 35%. The Act also contains a deduction for shareholders, partners, and members of up to 20% of a pass-through entity's "qualified business income" with respect to certain trades and businesses carried on by such shareholders, partners, and members. As a result of the tax rate reduction with respect to C corporations and the 20% deduction with respect to income earned by certain pass-through entities, many business owners are examining whether (i) to structure their businesses as C corporations or pass-through entities or (ii) to convert their existing entities to C corporations or pass-through entities.

Factors to Examine

The benefits of lower C corporation tax rates must be measured against the taxation of distributions by C corporation as dividends (i.e., double taxation). Generally, a shareholder in a C corporation that is in the top bracket pays a tax rate of 23.8% on qualified dividends while (assuming sufficient basis) a shareholder, partner, or member in a pass-through entity generally pays no tax on distributions of previously taxed income.

Another factor for organizations to consider is the possibility of future changes in law that may affect organizations. While the individual and pass-through entity (e.g., partnerships and S corporation) provisions are generally phased out by December 31, 2025, the tax cuts for C corporations are not subject to a similar time-based sunset. However, tax rates have changed dramatically over time since the last major tax reform in 1986, so one cannot rely on rates being stable—especially with the recent changes having passed so narrowly.

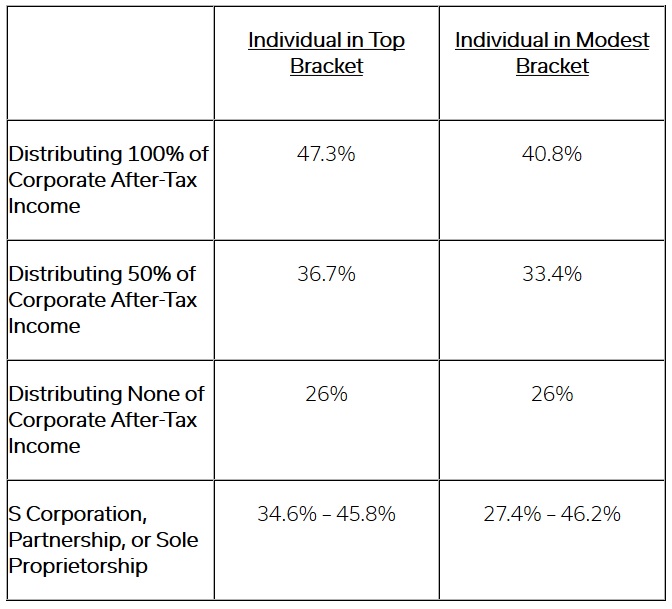

An Example of C Corporation vs. Pass-Through Entity Structures

Assuming one lives in a state imposing a 5% income tax, the table below compares the effective annual tax burdens (taking into account the 15.3% self-employment tax (a portion of which is deductible for U.S. federal income tax purposes) and the 3.8% net investment tax):

Note: Please be aware that the foregoing table is based on certain assumptions and is for illustrative purpose only. Also, please be aware that the chart is on an annual basis, rather than a long-term basis. When a corporation later distributes its earnings or a shareholder sells its corporate stock (at a price that reflects accumulated corporate earnings), the currently reinvested corporate earnings will be taxed at that time. Thus, although by reinvesting corporate earnings the 26% rate applies currently, the future tax on distribution of corporate earnings or the sale of corporate stock will cause the cumulative tax rate to be the 47.3% or 40.8% rate shown above for distributing 100% of corporate after-tax income.

Conversion to C Corporation or Pass-Through Entity Structure

- Conversion to C Corporation Structure: Provided a pass-through entity does not distribute most of its income to its shareholders, partners, or members (i.e., the pass-through entity reinvests its income into its business), the above illustration indicates that such pass-through entity and its shareholders, partners, and members could benefit from a C corporation structure.

- Conversion to Pass-Through Structure: Provided a C corporation does distribute most of its income to its shareholders (i.e., the C corporation does not reinvest its income into its business), the above illustration indicates that a C corporation and its shareholders could benefit from a pass-through structure. While a direct conversion can be costly for U.S. federal income tax purposes (i.e., such a conversion could result in a combined U.S. federal income tax in excess of 40% on the C corporation's built-in gain related to its tangible and intangible assets), other forms of reorganizations/conversions may prove to be beneficial.

Non-Tax Considerations

In addition to the tax considerations, organizations must take into account non-tax factors when deciding between a corporate structure and a pass-through structure. Some of these factors include (i) ease and cost of entity formation and maintenance and (ii) personal liability protection for shareholders, partners or members. In addition, organizations must take into account the flexibility of a corporate structure and a pass-through structure.

- C and S Corporations. Corporations provide shareholders with personal liability protection (i.e., a shareholder's exposure is limited to such shareholder's investment). However, to provide shareholders with the foregoing protection, a corporation must, in general, observe certain corporate formalities (e.g., articles of incorporation, by laws, a board of directors, and hold regular board and shareholder meetings). As a result of such corporate formalities, corporations can be costly to form and maintain. In addition, the Internal Revenue Code places restrictions on the number and type of shareholders that limit the flexibility of S corporations. Also, the Internal Revenue Code limits S corporations to one class of stock and foreigners cannot be shareholders.

- Partnership. There are, in general, three types of state law partnerships (i.e., a general partnership, a limited partnership, and a limited liability partnership). Similar to corporations, limited partnerships and limited liability partnerships provide personal liability protection for limited partners (but not general partners); however, general partnerships offer no personal liability protection for partners. Two primary advantages of partnerships (as compared to corporations) are (i) ease of formation and (ii) flexibility. Unlike corporations, partnerships are not required to comply with certain corporate formalities (e.g., holding annual meetings). In addition, partnerships, similar to LLCs (discussed below), may be less costly to form and maintain.

- LLC. Similar to corporations, LLCs provided members with personal liability protection but, arguably, LLCs provide greater protection than corporations (i.e., it is harder to pierce the corporate veil and attach personal liability to the LLC members with a well-drafted LLC agreement). In addition, similar to partnerships, a chief advantage of LLCs is their flexibility. LLC statutes have very few requirements and allow the LLC members to create an operating agreement to govern the LLC's operations by contract. In addition, some jurisdictions allow the managers of LLCs to waive certain fiduciary duties owed to their members, which further insulates the management team from personal liability. Finally, similar to partnerships, LLCs may be less costly to form and maintain. Generally, an LLC is taxed as a partnership or sole proprietorship, but electively it can be taxed as an S or a C corporation.

An organization's effective tax rate is one of the most important factors it should consider in determining its choice of entity. However, as noted, there are additional business and operational issues to consider. Every situation is different. While the difficulty of this decision has increased after the Act, we at Thompson Coburn LLP have examined these issues for clients and have developed templates, a process and resources to assist business owners and their advisers with a clear and focused approach to this critical inquiry.

Originally published in Law360's Expert Analysis.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.