The recently enacted tax reform act (the Act) significantly altered the U.S. taxation of foreign income. Perhaps most prominently, the Act allows U.S. corporations to fully deduct (and thus not pay tax on) dividends received from their foreign subsidiaries. However, the scope and breadth of the Act's international provisions go well beyond this move toward a partial territorial system. One change that has received considerably less attention is a modification of the attribution rules that apply in determining whether a foreign corporation is a controlled foreign corporation (CFC). The new attribution rule could have significant Section 956 implications in certain debt structures, including existing structures.

A CFC is a foreign corporation with more than 50% of its stock owned by one or more U.S. persons who own at least 10% of its stock (by vote or, post-Act, by value) (10% U.S. shareholders). Section 956 requires a CFC's 10% U.S. shareholders to include in income their pro rata shares of the CFC's earnings and profits that have not yet been subject to U.S. tax to the extent of the CFC's investments in U.S. property (including debt of a related U.S. borrower). A CFC is deemed to hold debt as to which it is a guarantor or in support of which at least two-thirds of its voting stock is pledged. As a result, if a CFC guarantees debt of its U.S. parent, the CFC is deemed to be the creditor on such debt and thus to have an investment in U.S. property.

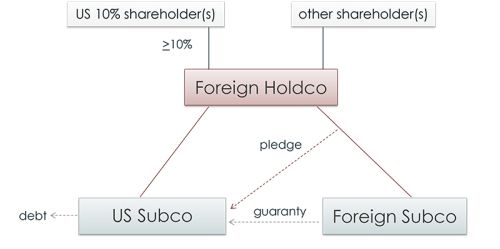

Under pre-Act law, a foreign subsidiary (ForSubco) of a foreign corporation (ForHoldco) was not a CFC merely by virtue of ForHoldco also owning the stock of a U.S. subsidiary (USSubco) (see attached diagram). In that situation, ownership of the ForSubco shares held by ForHoldco was not attributed to USSubco. As a result, provided that ForHoldco itself was not a CFC, ForSubco could guarantee the debt of USSubco (and 100% of the ForSubco stock could be pledged in support of the debt) without causing a deemed repatriation under Section 956 of the earnings and profits of ForSubco to any 10% U.S. shareholders of ForHoldco.

The Act changes that result. Under the Act, ownership of the ForSubco shares held by ForHoldco is attributed to USSubco. ForSubco is thus a CFC, because 100% of its shares are deemed owned by a U.S. shareholder (that is, USSubco). (Even under the Act, ownership of the shares of ForHoldco would not be attributed to USSubco, so ForHoldco would not be a CFC.) As a result, any 10% U.S. shareholders of ForHoldco would be treated as 10% U.S. shareholders of a CFC (i.e., ForSubco). Therefore, if ForSubco were a guarantor of the USSubco debt or if two-thirds or more of the ForSubco voting stock were pledged to support that debt, the 10% U.S. shareholders would be required to include in income their pro rata shares of ForSubco's earnings and profits that have not yet been subject to U.S. tax.

The change is retroactively effective for the last taxable year of a foreign corporation beginning before Jan. 1, 2018 (i.e., for 2017 with respect to a calendar-year foreign corporation). However, the change generally should present the Section 956 issue raised above with respect to only earnings and profits generated in subsequent years (whether pursuant to existing or new debt structures), because under the Act, earnings and profits of a foreign corporation generated in or prior to its last taxable year beginning before Jan. 1, 2018, are proportionately included in income by the corporation's 10% U.S. shareholders (whether or not the foreign corporation is a CFC, so long as it has at least one 10% U.S. shareholder that is a corporation).

The above change to the CFC attribution rules, as well as other changes to the CFC rules in the Act, have other significant implications that should be discussed with your tax advisers.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.