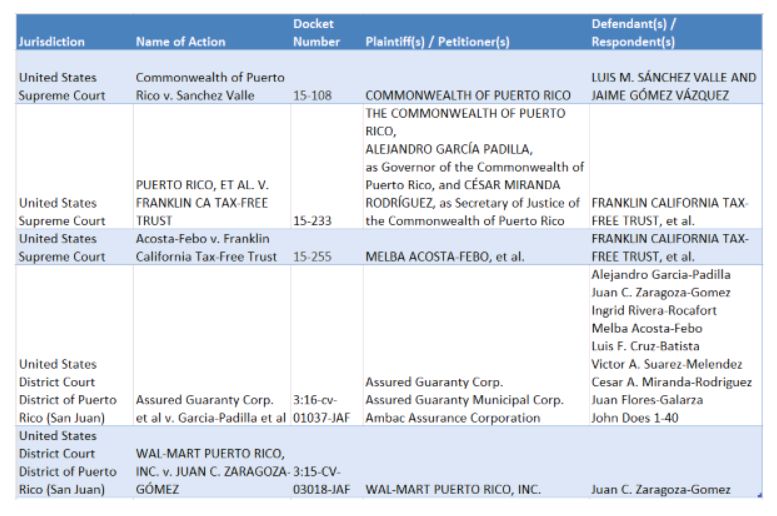

On Wednesday, January 13, 2016, the U.S. Supreme Court will hear arguments in the appeal styled under the caption Commonwealth of Puerto Rico v. Sanchez Valle, No. 15-108. In this case, the Supreme Court is asked to determine whether Puerto Rico and the United States are separate sovereigns for purposes of the Double Jeopardy Clause contained in the Fifth Amendment of the U.S. Constitution. Puerto Rico wants to be able to prosecute crimes in its courts even though the federal government had already prosecuted respondents for those same crimes. In order to do that, Puerto Rico and the United States must be treated as separate "sovereigns."

On December 23, 2015, the United States Solicitor General filed an amicus brief on behalf of the United States taking the position that Puerto Rico and the United States are not separate sovereigns for purposes of the Double Jeopardy Clause. The United States asserts that U.S. territories, such as Puerto Rico, are not sovereigns.1 This position is contrary to the position taken by Puerto Rico. Instead, the United States asserts that territories are under the sovereignty of the United States and subject to the plenary authority of Congress. (Brief for the United States as Amicus Curiae Supporting Respondents ("U.S. Amicus Brief") filed in Commonwealth of Puerto Rico v. Sanchez Valle, No. 15-108, at 7.) The United States argued that "In the Territories of the United States, Congress has the entire dominion and sovereignty, national and local, Federal and state, and has full legislative power over all subjects upon which the legislature of a State might legislate within the State." (Id. at 16.) The United States further argued that "Puerto Rico's transition to self-government did not change its constitutional status as a U.S. territory. The United States did not cede its sovereignty over Puerto Rico, and Puerto Rico did not become a State or an independent nation." (Id. at 21). As stated previously, Puerto Rico takes the position that it is a separate sovereign and, as such, it is able to separately prosecute crimes in its courts even if the federal government has already prosecuted for the same crimes.

Sanchez Valle will be the first of two appeals to be heard by the U.S. Supreme Court this term involving Puerto Rico. As we had previously reported, by order dated December 4, 2015, the Supreme Court also agreed to consider the appeals by the Commonwealth and the Government Development Bank regarding the constitutionality of the Commonwealth's Debt Enforcement & Recovery Act (DERA) in the appeals styled under the caption Puerto Rico v. Franklin California Tax-Free Trust, 15-233, and Acosta-Febo v. Franklin California Tax-Free Trust, 15-255 (the "Franklin Fund Appeals").

The Supreme Court's decision in Sanchez Valle could have an impact on the Supreme Court's decision regarding the constitutionality of the DERA. In filing its amicus brief, the United States asserted that "The Court's decision [in Sanchez Valle] . . . may affect the federal government's defense of federal legislation and policies related to Puerto Rico across a broad range of substantive areas, including congressional representation, federal benefits, federal income taxes, bankruptcy, and defense." (Id. at 1). The hearing on the Franklin Fund Appeals has not yet been scheduled, but briefs by the parties will be filed in the coming weeks.

Monolline Insurers Challenge Puerto Rico's Exercise of ClawBack Rights

On January 7, 2016, Assured Guaranty Corp., Assured Guaranty Municipal Corp. and Ambac Assurance Corporation (collectively, the "Monolines") commenced an action in the United States District Court for the District of Puerto Rico against the Governor of Puerto Rico and certain other officials in an action styled under the caption Assured Guaranty Corp. et. al v. Alejandro Gracia Padilla et. al, No. 16-cv-1037. The Puerto Rico Constitution and applicable statutes allow Puerto Rico to use certain pledged revenues to pay interest and principal on "public debt" due in that year if other available resources (including surplus for any fiscal year) of the Commonwealth are not sufficient to meet appropriations for that year. The Puerto Rican Constitution provides that interest and principal on the public debt due that year shall first be paid, and other disbursements shall thereafter be made in accordance with the order of priorities established by law.

As previously reported, Governor Padilla issued Executive Order OE-2015-046, instructing the retention or transfer of revenues pledged by the Puerto Rico Highways and Transportation Authority (PRHTA), the Puerto Rico Infrastructure Financing Authority (PRIFA), the Metropolitan Bus Authority (AMA), the Integrated Transport Authority (ITA) and the Puerto Rico Convention Center District Authority (PRCCDA) as security for bonds previously issued by those agencies. In this action, the Monolines are challenging the constitutionality of the Governor's executive orders authorizing the clawback of certain revenues pledged by PRHTA, PRCCDA and PRIFA. While acknowledging that the pledged revenues were subject to clawback to pay public debt, the Monolines assert that Puerto Rico was not authorized to "claw back" or divert the pledged revenues where other available resources exist from which public debt could be paid. The Monolines also assert that the executive orders violate the Takings Clause and the Due Process Clauses of the Fifth and Fourteenth Amendments of the U.S. Constitution.

The following is a table of the major litigation involving Puerto Rico's troubled finances.

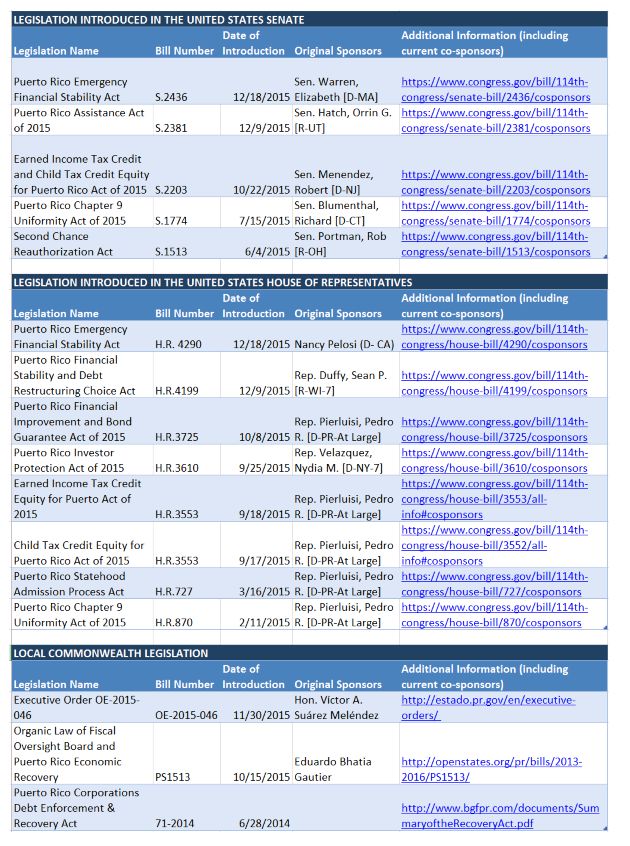

The following is a table of the major legislation that has been introduced to address Puerto Rico's troubled finances.

Footnote

1 Other U.S. territories include American Samoa, Guam, the Northern Mariana Islands, and the U.S Virgin Islands (U.S. Amicus Brief at 15, n.2).

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.