- within Food, Drugs, Healthcare and Life Sciences topic(s)

EXECUTIVE SUMMARY

A combination of pending actual and potential tax increases effective in 2013 may have a significant impact on transactional planning in the third and fourth quarters of 2012. These potential tax increases may affect deal terms and also motivate some buyers and sellers to move quickly to close transactions by year-end. Affected parties should evaluate their inventory of pending transactions and identify those transactions for which closing in 2012 may be of critical importance. Please feel free to direct any questions regarding the matters discussed in this client alert to any of the attorneys listed below under the heading Morrison & Foerster Contacts.

POTENTIAL TAX INCREASES

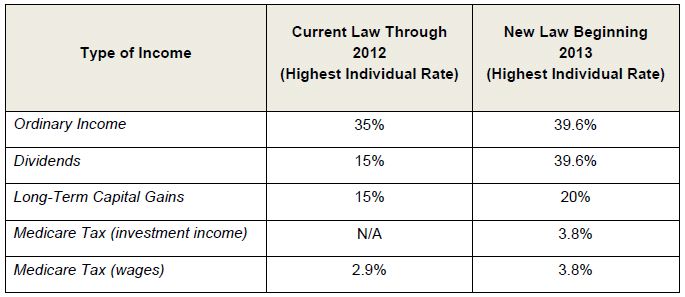

The "Bush tax cuts" are currently set to expire on December 31, 2012. As a result, absent affirmative Congressional action, on January 1, 2013, the highest tax rate applicable to an individual taxpayer will increase from 35% to 39.6% for ordinary income, 15% to 39.6% for dividends, and 15% to 20% for long-term capital gains. At the same time, the already enacted tax increases under the 2010 healthcare reform package will take effect. Of particular significance to transactional activity will be the new 3.8% additional Medicare tax imposed on the investment income of individuals earning more than $200,000 and couples earning more than $250,000. The healthcare reform package also increases the existing Medicare tax on wages and salaries in excess of $200,000 for individuals and $250,000 for couples by 0.9% (from 2.9% to 3.8%). Each of these potential tax increases is summarized in the table below.

POTENTIAL IMPACT ON TRANSACTIONS

- Closing Date. The combined effect of the sunset of the Bush tax cuts and the new Medicare tax on investment income would result in an overall increase in the effective maximum federal tax on long-term capital gains recognized by individuals by 8.8 percentage points to 23.8% (as compared to the current 15% rate). This would be a material incremental tax cost that could motivate affected buyers and sellers to push hard to close transactions before the end of 2012. In addition, the spending cuts (so-called "sequestrations") required by the Budget Control Act of 2011 and the looming prospect of another potential fight over the debt limit in early 2013 could create increasing concerns regarding the general state of the U.S. economy. Any growing concerns regarding the overall U.S. macroeconomic climate may further prompt buyers and sellers to move quickly to close in 2012.

- Tax-Deferred Equity Consideration. In light of the pending 8.8% increase in the federal tax rate on individual long-term capital gains, it may make sense for some sellers who plan to close transactions in 2012 to receive any potentially tax-deferred equity consideration on a taxable basis rather than on a non-taxable basis. This approach may be particularly beneficial if the stock received in 2012 is likely to be sold within a relatively short period of time following the closing date, because the value of the tax deferral to the seller may not offset the cost of the effective tax rate increases. Depending on the facts and circumstances, converting a non-taxable transaction into a taxable one often can be accomplished without changes to the economic terms, and requiring only slight modifications to the legal form. A taxable transactional pattern may also have the potential to deliver incremental tax-basis benefits to the buyer, which in turn can allow the seller to press for payment of an additional premium.

- Escrow / Earn-Out Provisions and Installment Sale Deferrals. Once again, in light of the pending 8.8% increase in the federal tax rate on individual long-term capital gains, it may also make sense for some sellers to structure escrow or earn-out provisions so that payments can be accelerated to some degree in the event that the Bush tax cuts are not extended. For example, a seller might agree to receive a reduced series of one or more earn-out payments beginning on or before December 31, 2012, in the event that the 15% long-term capital gains rate is not extended, in lieu of the buyer making a potentially larger series of one or more earn-out payments that would otherwise begin sometime in 2013. Absent an actual acceleration provision of some kind, sellers can also potentially elect out of installment reporting as late as the extended due date for their 2012 returns and effectively accelerate deferred payments into income for 2012 if there is an adverse rate change (but such a strategy requires careful analysis, especially when there is a high degree of potential variability in the contingent payments that may be made). Electing out of installment sale treatment also requires planning for cash flow needs to pay the 2012 taxes that would be due April 15, 2013.

- Dividend Distributions. As previously noted, if the Bush tax cuts are not extended, the maximum federal tax rate on dividends will jump dramatically from 15% to 39.6% beginning in 2013. This could, in turn, have a significant impact upon certain types of corporate recapitalization or reorganization transactions where the cash received by a shareholder may be characterized as a dividend rather than long-term capital gain. This can occur, for example, in certain minority investment recapitalization transactions where the pre-existing shareholders receive a distribution of some or all of the newly invested cash and do not simultaneously experience a meaningful reduction in their level of ownership or control of the corporation. In such a situation, it may make sense to attempt to restructure the terms of the transaction to avoid dividend characterization. By comparison, through the end of 2012, an individual shareholder may be indifferent as between receiving consideration that is characterized as a dividend rather than long-term capital gain, given the 15% rate that is currently applicable to both types of income.

- Incentive Compensation. Finally, if Congress does not act to preserve the current tax rate structure, the highest individual tax rate on ordinary income will increase from 35% to 39.6% beginning in 2013 (or 40.5% after including the additional 0.9% Medicare tax on wages and salaries in excess of $200,000 for individuals and $250,000 for couples). As a result, a meaningful spread will continue to exist between ordinary income and long-term capital gains rates, and individual incentive compensation planning should continue to take that spread into account, as well as evaluate the benefit of compensation deferrals past 2012 in light of the increasing rates. Another continuing source of uncertainty exists in the area of incentive compensation with respect to the potential for passage of "carried interest" legislation that would tax certain flow-through capital gains at ordinary income rates. This issue may receive renewed attention in Congress in late 2012 or early 2013.

CONCLUDING OBSERVATIONS

- Most commentators have remarked that Congress is unlikely to take any action with respect to tax rates prior to the November elections. After the elections only a very short time period will remain for any potential legislative action, and during that time financial markets may be subjected to an even higher degree of uncertainty and dislocation.

- Given the potential for tax increases and continued macroeconomic instability, affected parties should evaluate their inventory of pending transactions and identify those transactions for which closing in 2012 may be of critical importance. Steps should then be taken to consummate such transactions in an expeditious and tax-efficient manner. Planned transactions should also take into account the increased backlog that may develop toward year-end with respect to transactions that may be subject to regulatory approvals.

Because of the generality of this update, the information provided herein may not be applicable in all situations and should not be acted upon without specific legal advice based on particular situations.

© Morrison & Foerster LLP. All rights reserved

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.