On June 29th, the CFTC published a proposed policy statement and interpretive guidance addressing the extraterritorial reach of the swaps provisions of the Commodity Exchange Act ("CEA") that were enacted by Title VII of the Dodd-Frank Act. The foreign banking community and U.S. banks with overseas operations have been waiting for this guidance for quite some time. International banks headquartered outside the United States that engage in swaps activities in the United States have been particularly concerned about U.S. regulation of activities that are more properly supervised and regulated by home country, and not host country, regulators. Further, uncertainty regarding which entities must register as swap dealers or major swap participants, and the extent to which entity level and transaction level requirements would apply to registrants, have hindered the efforts of foreign banks to address their derivatives business and to engage in compliance planning.

The interpretive guidance is open for comment for a 45-day period following Federal Register publication. In large measure, the guidance follows the broad concepts that Chairman Gensler outlined in a June 14th speech before the Institute of International Bankers. While noting that corporate structures and inter-affiliate obligations may cause swaps activity, "regardless of where that activity takes place, to have a direct and significant connection with activities in, or effect on, commerce in the U.S.", Chairman Gensler indicated that the guidance would take into account the comments provided to the CFTC and the SEC on extraterritoriality by the foreign banking community.

Brief Summary

The proposed interpretive guidance and policy statement describes:

- how the CFTC will assess whether a non-U.S. person's swap dealing activities or swap positions may require registration as a swap dealer or major swap participant, respectively;

- the application of the related requirements under the CEA to swaps involving such persons; and

- the application of the clearing, trade execution, and certain reporting and recordkeeping provisions under the CEA, to cross-border swaps involving one or more counterparties that are not swap dealers or major swap participants.

More specifically, the guidance provides:

- A definition of "U.S. person";

- Factors helpful in assessing whether a non-U.S. person's level of dealing with U.S. persons requires registration of that entity as either a swap dealer or a major swap participant;

- Clarification regarding certain entity level and transaction level requirements;

- Substituted compliance, so that a foreign entity may comply as to most entity level and certain transaction level requirements with its home country rules provided those are comparably robust; and

- A means for assessing whether foreign/home country rules would be deemed comparable for these purposes.

Market participants and practitioners may be relieved that some guidance has now been made available for comment; however, the guidance in most cases does not necessarily provide the type of bright lines that are essential to those that hope for legal certainty. Indeed, the guidance is quite nuanced and requires thoughtful reading and analysis. In this alert, we set out the basic principles and will provide additional insights in a forthcoming alert.

Who is a U.S. person?

Section 2(i) states that the provisions added to the CEA by Title VII of the Dodd-Frank Act shall not apply to activities outside the United States unless those activities: (1) have a direct and significant connection with activities in, or effect on, commerce of the United States; or (2) contravene such rules or regulations as the Commission may prescribe or promulgate as are necessary or appropriate to prevent the evasion of any provision of the CEA added by the Dodd-Frank Act. In the guidance, the CFTC proposes to define the term "U.S. person" by taking into account whether that person's swap activities or transactions in fact have a direct and significant connection to the United States, and whether there is substantial U.S. interest in applying the regulatory framework of Title VII to non-U.S. persons. As proposed, the term "U.S. person" includes:

- Any natural person who is a resident of the United States;

- Any corporation, partnership, LLC, business or other trust, association, joint-stock company, fund, or any form of enterprise similar to any of the foregoing, in each case that is either (A) organized or incorporated under the laws of the United States or having its principal business in the United States (legal entity), or (B) in which the direct or indirect owners thereof are responsible for the liabilities of such entity and one or more of such owners is a U.S. person;

- Any individual account (discretionary or not) where the beneficial owner is a U.S. person;

- Any commodity pool, pooled account, or collective investment vehicle (whether or not incorporated in the United States) of which a majority ownership is held, directly or indirectly, by a U.S. person;

- Any commodity pool, pooled account, or collective investment vehicle the operator of which would be required to register as a commodity pool operator under the CEA;

- A pension plan for the employees, officers, or principals of a legal entity with its principal place of business inside the United States; or

- An estate or trust, the income of which is subject to United States income tax, regardless of source.

The definition captures foreign branches of U.S. banks, for example, but would not generally include non-U.S. subsidiaries and affiliates of such U.S. banks. In its questions, the CFTC asks whether "U.S. person" should include a foreign affiliate or subsidiary guaranteed by a U.S. person. Many commenters had noted that Regulation S promulgated under the Securities Act of 1933 already provides a definition of "U.S. person" that would be useful for these purposes. The CFTC, however, does not rely on the Regulation S definition, but does request comment on the utility of the Reg S definition for these purposes.

How do you Calculate Activity for the Swap Dealer De Minimis Threshold?

The guidance notes that the entity definitions in the CEA, and the regulations thereunder, do not "contain any geographic limitations and do not distinguish between U.S. and non-U.S. swap dealers or non-U.S. MSPs". The entity definitions establish a de minimis threshold, and the CFTC clarifies that it believes that non-U.S. persons who engage in more than a de minimis level of dealing with U.S. persons would be required to register as swap dealers. However, in calculating this threshold, a non-U.S. person will not be required to include the notional value of dealing transactions with foreign branches of U.S. registered swap dealers.

In calculating the notional value of swaps, the regulations currently require aggregation of dealing transactions entered into by affiliates that are under common control. This would require that a non-U.S. person aggregate the notional value of (i) swaps between its commonly-controlled non-U.S. affiliates and any U.S. person and (ii) swaps between its commonly-controlled non-U.S. affiliates and any other party but only if the non-U.S. affiliates obligations are guaranteed by U.S. person. Under the CFTC's guidance, the swap dealing transactions of affiliated U.S. persons should not be included by a non-U.S. person in calculating the thresholds for swap dealer registration.

Does Regular Business Include Business That Does Not Face U.S. Persons?

Before applying the de minimis test, an entity should determine whether it is engaged in dealing as part of its regular business. Recognizing that an affiliate of a U.S. person is not automatically a "U.S. person" for purposes of the CEA, the proposed guidance provides that a non-U.S. person whose obligations are not guaranteed by a U.S. person may individually determine, based on relevant facts and circumstances, whether its swaps dealing activities with U.S. persons are part of a "regular business" and whether it is, as a result, subject to registration. A non-U.S. person without a guarantee from a U.S. person should consider whether it is dealing as part of its "regular business" only with respect to U.S. persons.

Consistent with the above, in determining whether it is an MSP, a non-U.S. person would include all of its swap positions where its counterparty is a U.S. person, but would not "count" any swap position where its counterparty is a non-U.S. person.

How do you Calculate Activity Levels for MSPs?

The Commission proposes in the draft guidance to treat swap dealers and MSPs differently with respect to including swaps guaranteed by a U.S. person in making calculations for purposes of the registration requirements. Where a non-U.S. person's aggregate notional value of swaps dealing activities with U.S. persons and with non-U.S. persons whose obligations are guaranteed or are otherwise formally supported by a U.S. person exceed the de minimis levels, the non-U.S. person will be required to register as a dealer with the Commission. Non-U.S. persons would be required to register with the Commission as MSPs when their swaps with U.S. persons, disregarding any positions where their obligations are guaranteed by U.S. persons, exceed the relevant MSP threshold.

To summarize the calculation rules, in determining whether a non-U.S. person is engaged in more than a de minimis level of swap dealing, the person should consider the aggregate notional value of:

- swap dealing transactions between it (or any of its non-U.S. affiliates under common control) and a U.S. person (other than foreign branches of U.S. persons that are registered swap dealers); and

- swap dealing transactions (or any swap dealing transactions of its non-U.S. affiliates under common control) where its obligations or its non-U.S. affiliates' obligations thereunder are guaranteed by U.S. persons.

In determining whether a non-U.S. person holds swap positions above the MSP thresholds, the person should consider the aggregate notional value of:

- any swap position between it and a U.S. person (but its swap positions where its obligations thereunder are guaranteed by a U.S. person generally should be attributed to that U.S. person and not included in the non-U.S. person's determination); and

- any swap between another non-U.S. person and a U.S. person, where it guarantees the obligations of the non-U.S. person thereunder.

How Will Branches, Agencies and Affiliates be Treated for Registration Purposes?

The guidance provides that for U.S. persons, an entity model and central booking model will be applied so that the U.S. person will be considered the registrant with respect to swaps dealing activities conducted by that entity's foreign branches and agencies or its affiliates, but branches and agencies or affiliates that otherwise independently meet the quantitative thresholds would have to register as swap dealers.

Similarly, where a non-U.S. person is the central booking entity, even if the U.S. branch, agency, or affiliate of that non-U.S. person solicits or negotiates in connection with the swap entered into by the non-U.S. person, the CEA's Title VII requirements, including the registration requirement, applicable to swap dealers will apply to the non-U.S. person.

How Will Entity Level and Transaction Level Requirements Be Applied?

In discussing entity level and transaction level requirements, the CFTC recognizes the primary supervisory role of home country supervisors with respect to non-US dealers and MSPs, but does not necessarily defer to those supervisors in all respects. For purposes of providing guidance on substituted compliance, the guidance classifies certain Title VII requirements as Entity-Level and others as Transaction-Level requirements. Within these two broad categories, the CFTC also draws some important distinctions—highlighting certain of the requirements which are more integral to meeting the CFTC's regulatory objectives for the derivatives market.

Entity-level requirements under Title VII of the Dodd-Frank Act and the implementing regulations address: capital adequacy; the role of the chief compliance officer; risk management; swap data recordkeeping; swap data reporting ("SDR Reporting"); and physical commodity swaps reporting ("Large Trader Reporting"). These requirements apply to registered swap dealers and MSPs across all their swaps without distinction as to counterparty or location of the swap.

Registered non-U.S. swap dealers and non-U.S. MSPs must comply with those entity level requirements that address risk mitigation for a firm as a whole, but, in consideration of principles of international comity, the Commission intends to permit substituted compliance with foreign regulations for these requirements in certain circumstances. The CFTC, however, views the data provided by SDR Reporting and Large Trader Reporter as critical to the CFTC's supervisory mandate and therefore will require non U.S. swap dealers and non-U.S. MSPs to comply with those requirements, while also recognizing that substitute compliance may also occur with respect to swaps between such entities and other non-U.S. persons.

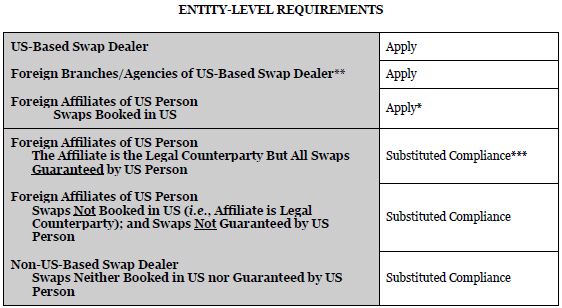

In an Appendix to the proposed guidance, the CFTC provides the following entity-level chart, which we have reprinted here:

* Where swaps are solicited or negotiated by a foreign affiliate of a U.S. person but directly booked in the U. S. person, the U.S. person must comply with all of the swap dealer duties and obligations related to the swaps, including registration, capital and related prudential requirements.

** Both Entity-Level and Transaction-Level Requirements are the ultimate responsibilities of the U.S.-based swap dealer.

*** With respect to the SDR reporting requirement, the Commission may permit substituted compliance only if direct access to swap data is proved to the Commission.

Transaction level requirements include: clearing and swap processing; margining and segregation for uncleared swaps; trade execution; swap trading relationship documentation; portfolio reconciliation and compression; real-time public reporting; trade confirmation; daily trading records; and external business conduct standards. The guidance generally does not extend substituted compliance to transaction level requirements, since it views the purpose of most of these requirements—risk mitigation and transparency—as part of its critical oversight responsibility.

As a general matter, transaction-level requirements will apply to all U.S.-facing transactions. U.S.-facing transactions include transactions with persons or entities operating in or organized in the United States, and also transactions with the foreign branches of these entities. The guidance provides that transaction level requirements will apply to swaps in which: (1) a non-U.S. counterparty is majority-owned, directly or indirectly, by a U.S. person; (2) the non-U.S. counterparty regularly enters into swaps with one or more other U.S. affiliates or subsidiaries of the U.S. person; and (3) the financials of such non-U.S. counterparty are included in the consolidated financial statements of the U.S. person.

Conversely and consistent with principles of comity, the guidance does not require the application of most transaction level requirements to swaps between a non-U.S. swap dealer or non-U.S. MSP and a non-U.S. counterparty that is not guaranteed by a U.S. person, and, in the case of external business rules, it does not require compliance with U.S. rules for transactions between a non-U.S. swap dealer or non-U.S .MSP and a non-U.S. counterparty.

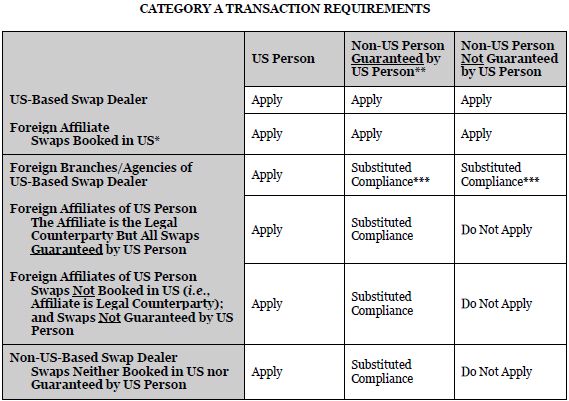

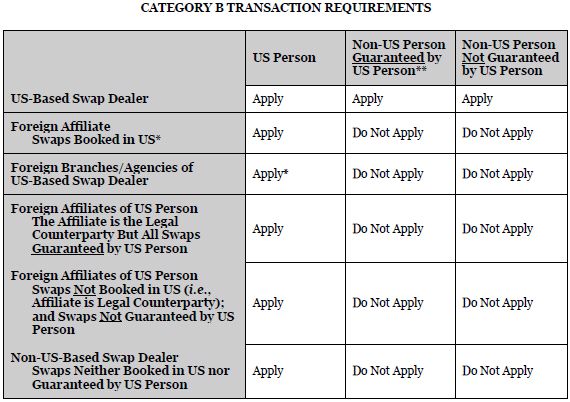

In an appendix to the CFTC's proposed guidance, the CFTC sets out various charts that summarize the application of the various transaction-level requirements. The transaction-level requirements are grouped into two broad categories: category A requirements, which related to risk mitigation and transparency (clearing and swap processing, margin, trading relationship documentation, portfolio reconciliation and compression, real-time reporting, trading confirmation and daily trading records), and category B sales practice requirements (external business conduct standards). These are set out in the following charts:

* Where swaps are solicited or negotiated by a foreign affiliate but directly booked in the U. S. person, the U.S. person must comply with all of the swap dealer duties and obligations, including all Transaction-Level Requirements. The foreign affiliate, if separately required to register as a swap dealer, must comply with those requirements applicable to its swap dealing activities.

** The Transaction-Level Requirements apply to swaps in which: (i) a non-U.S. counterparty is majority-owned, directly or indirectly, by a U.S. person; (ii) the non-U.S. counterparty regularly enters into swaps with one or more U.S. affiliates or subsidiaries of the U.S. person; and (iii) the financials of such non-U.S. counterparty are included in the consolidated financial statements of the U.S. person.

*** Under limited circumstances, where there is not a comparable foreign regulatory regime, foreign branches and agencies of U.S. swap dealers may comply with the local transaction-level requirements rather than the Transaction-Level Requirements, subject to specified conditions.

* Where swaps are solicited or negotiated by an affiliate of a U.S. person but directly booked in the U. S. person, the U.S. person must comply with all of the swap dealer duties and obligations, including all Transaction-Level Requirements. The foreign affiliate, if separately required to register as a swap dealer, must comply with those requirements applicable to its swap dealing activities.

** The Transaction-Level Requirements apply to swaps in which: (i) a non-U.S. counterparty is majority-owned, directly or indirectly, by a U.S. person; (ii) the non-U.S. counterparty regularly enters into swaps with one or more U.S. affiliates or subsidiaries of the U.S. person; and (iii) the financials of such non-U.S. counterparty are included in the consolidated financial statements of the U.S. person.

Which Requirements may be Satisfied through Substituted Compliance? How Will Comparability Be Assessed?

While the CFTC intends to use its experience in making "comparability" findings in exempting foreign brokers from registrations as FCMs for purposes of evaluating comparability for non-U.S. swap dealers and MSPs, it has indicated that its review of regulatory requirements applicable to non-U.S. swap dealers and MSPs will be more focused on whether the applicable foreign regulatory regime meets shared regulatory objectives with those of the Commission. To that end, the CFTC will examine the regulatory requirements applicable to non-U.S. swap dealers and MSPs and also contemplates an on-going process of cooperation and coordination with foreign regulatory authorities. Substituted compliance will be recognized only in those areas that are determined to be comparable and comprehensive to the CEA and its implementing regulations. In that regard, the CFTC may find that certain entity level requirements or transaction level requirements are not covered by foreign regulation and will impose the U.S. standards.

A non-U.S. person, a group of non-U.S. persons from the same jurisdiction or a foreign regulator may initiate the comparability process by requesting, in connection with the swap dealer or MSP registration process, the CFTC's permission to use the relevant home country's comparable requirements rather than the applicable Dodd-Frank Act requirements. An application must state the grounds for a comparability determination with specificity and include supporting legislation and rules. To facilitate its market supervisory role, the CFTC expects to enter into a memorandum of understanding ("MOU") or similar arrangement with the home country supervisor for purposes of on-going information sharing (including, for example, access to supervisory and possibly enforcement information and on-site visits) and cooperation for the supervision of swap dealers and MSPs. Once a determination of comparability has been made for a particular jurisdiction, the CFTC likely will use that that determination as guidance for subsequent applications from that jurisdiction. However, if material changes (to be defined by the CFTC) occur with respect to information that was submitted to support a comparability determination, a prior comparability determination may no longer be valid.

The guidance specifically addresses comparability with respect to clearing. For swaps subject to mandatory clearing, the CFTC expects to find comparability with foreign regulatory regimes when the swap is subject to a comparable mandate issued by appropriate government authorities in the home country of the counterparties to the swap; and the swap is cleared through a Derivatives Clearing Organization that is exempt from CEA registration.

Even where comparability is found, the CFTC will retain broad enforcement authority, including anti-fraud and anti-manipulation authority with respect to cross-border swaps activity.

Provisions Applicable to Persons Other Than Swap Dealers and MSPs

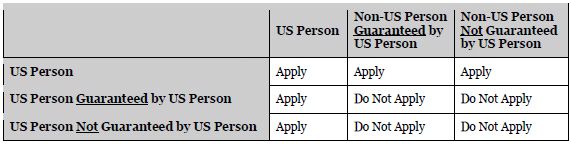

Important provisions of Title VII -- clearing, trade execution, public reporting, large trader reporting, SDR Reporting and Swap Data Recordkeeping -- apply to persons other than Swap Dealers and MSPs. Where neither party to a cross-border swap transaction is a swap dealer or MSP, but at least one party is a U.S. person, such requirements will apply. Where neither party to a cross-border swap transaction is a swap dealer or MSP and neither party is a U.S. person, such requirements will not apply.

The CFTC's determination of the applicability of the rules rests on its belief that "U.S. persons' swap activities outside the United States have a direct and significant connection with activities in, or effect on, U.S. commerce". The CFTC has expressed particular concern about non-U.S. persons being used as conduits by U.S. persons, and has stated that, while non-U.S. persons that are affiliates of U.S. persons will be exempt from the above-discussed requirements if engaged in swap transactions with other non-U.S. persons, it is considering "appropriate measures" to address its concerns relating to conduits.

The CFTC will permit substituted compliance for swap transactions involving at least one U.S. person that is not a swap dealer or MSP with respect to SDR Reporting and swap data recordkeeping requirements but not for the clearing, trade execution, public reporting and large trader reporting requirements. While it acknowledges that its determination not to allow substituted compliance for key requirements may lead to two or more jurisdictions asserting authority over these swaps with possible duplicative or inconsistent regulatory requirements, the CFTC states that it intends to address these issues through regulatory coordination (as opposed to exemptive relief, for example).

The CFTC provides the following summary table relating to non-swap dealer/non-MSP compliance with certain Dodd-Frank requirements*.

* The relevant Dodd-Frank requirements are those relating to: clearing, trade execution, real-time public reporting, Large Trader Reporting, SDR reporting and swap data recordkeeping.

Phased Compliance

The CFTC also proposed on Friday a phased compliance program for certain entity level and transaction level requirements, permitting dealers and major swap participants to prepare for DFA compliance. The proposed phased compliance would become effective on the compliance date for registration of swap dealers and major swap participants and expire: (i) for non-U.S. swap dealers, non-U.S. major swap participants, foreign branches of U.S. swap dealers, and foreign branches of U.S. major swap participants, 12 months following the publication of the proposal; and (ii) for U.S. swap dealers and U.S. major swap participants, January 1, 2013.

Because of the generality of this update, the information provided herein may not be applicable in all situations and should not be acted upon without specific legal advice based on particular situations.

© Morrison & Foerster LLP. All rights reserved