The U.S. Department of Labor ("DOL") has long been concerned about transparency regarding fees and expenses for participants in defined contribution retirement plans (e.g., 401(k) plans, 403(b) plans, profit sharing plans, money purchase plans) as part of its focus on ensuring that workers have access to the information they need to meaningfully compare the investment options under their employer-sponsored retirement plans and make informed decisions about how to manage and invest their retirement plan accounts. The DOL has made this concern one of its priorities over the last few years, culminating in final regulations (the "Final Regulations") requiring plan administrators of participant-directed defined contribution retirement plans that are covered by the Employee Retirement Income Security Act ("ERISA") to disclose certain plan and investment-related information, including fee, expense and investment performance information, to participants and beneficiaries. These new rules will generally apply as early as May 31, 2012.

Plan administrators of the impacted retirement plans and their service providers need to take prompt action to prepare for implementation of these new requirements, as they are tedious and detailed and will potentially require significant changes to current procedures and practices.

General Requirements

The Final Regulations provide that when plan participants and beneficiaries are able to choose their investments (i.e., the plan is "participant-directed") in a defined contribution retirement plan, the plan administrator has a fiduciary duty to ensure that such participants and beneficiaries have sufficient information regarding the plan and the plan's investment options to make informed decisions about their investment choices. To that end, the Final Regulations provide for specific and detailed disclosure requirements that will require plan administrators of impacted defined contribution plans to assess their current disclosure practices and likely make changes to comply with the Final Regulations.

Individuals Who Must Receive the Disclosures. Notably, the indicated disclosures must be provided to each "participant and beneficiary" who, pursuant to the terms of the particular plan, has a right to direct the investment of his or her individual plan account. The DOL has clarified that this includes: (i) current and former participants who maintain plan accounts, (ii) employees who are eligible to participate in the plan but have not actually enrolled, and (iii) beneficiaries who have the right to direct the investment of their plan accounts (e.g., as a result of the death of a participant or pursuant to a qualified domestic relations order).

Timing and Content Rules under the Final Regulations. We provide below an outline of the required disclosures and their timing and content, cautioning that the new rules are long and detailed and this Alert only serves as a summary and not an exhaustive recitation of all the requirements of the Final Regulations. As a general matter, the information required to be provided under the Final Regulations is separated into two categories—plan-related information and investment-related information–which we describe more fully on the following pages.

1. Initial & Annual Notice. On or before the date that an individual can first direct investment of his or her plan account, and annually thereafter (i.e., once every 12 months), a notice must be given (referred to in this Alert as the "Initial Notice" and the "Annual Notice"). The Initial Notice and the Annual Notice must contain the following information:

a. Plan-Related Information. This category of information is further divided into three subcategories as follows:

i. General Plan Information. General plan information consists of information about the operation of the plan and the current investment options offered, such as an explanation of when and how to give investment instructions under the plan (and any plan limitations on such instructions, such as restrictions on transfers to or from an investment alternative), a description of any "brokerage windows" or similar arrangement that enables the selection of investments beyond those designated by the plan, reference to any applicable voting rights, and identification of any designated investment managers.

ii. Administrative Expenses Information. These are expenses related to plan administrative services (such as annual or monthly recordkeeping fees) that may be charged to the plan (and that are not included in the operating expenses of a particular investment options) and then allocated to participants' and beneficiaries' individual accounts. The basis on which such charges will be allocated to each individual account must also be disclosed (e.g., pro-rata or per capita).

iii. Individual Expenses Information. These are expenses that may be charged against a participant's or beneficiary's individual account for services provided on an individual basis (e.g., fees to process loans or qualified domestic relations orders (QDROs), or sales charges).

b. Investment-Related Information. The required investment-related information is detailed and comprehensive and requires that investment alternatives be compared against each other. For each investment option available under the plan, the information required to be disclosed includes: performance data, benchmark information, fee and expense information, Internet website address to obtain more specific or current information, and a glossary of terms. The comparative format requirements for presenting the investment-related information is discussed in more detail below under the subheading "Format and Distribution Methods for Fee Disclosure Notices."

For new participants and beneficiaries, the requirement to provide information on or before the date on which the participant or beneficiary can first direct investment of his or her plan account may be satisfied by furnishing to such individual the most recent Annual Notice furnished to participants and beneficiaries and, with respect to plan-related information, any subsequent Updating Notice (as defined below). The Final Regulations do not require that a plan administrator update materials in "real time" for each newly eligible employee.

2. Updating Notice. Any plan-related information previously disclosed in an Initial Notice or Annual Notice must be updated within at least 30 days but not more than 90 days prior to the effective date of the change (referred to herein as the "Updating Notice"). If a plan administrator is unable to provide such advance notice due to events that are unforeseeable or beyond the plan administrator's control, then the Updating Notice must be provided as soon as reasonably practicable. Notably, the Final Regulations do not contain a "materiality" threshold for changes— as such, any change to the required plan-related information necessitates an Updating Notice. The updating requirements do not apply to investment-related information.

3. Quarterly Notice. At least once every three (3) months, participants and beneficiaries must receive statements showing the dollar amount of the plan-related fees and expenses (i.e., both administrative expenses and individual expenses) actually charged to or deducted from their individual accounts (referred to in this Alert as the "Quarterly Notice"). The statements must include a general description of the services that correspond to the expenses charged. The DOL has confirmed that no Quarterly Notice is required if there were no charges to a participant's or beneficiary's individual account in the preceding quarter (which should also mean that Quarterly Notices would not be required to be furnished to employees who are eligible to participate in the plan but have not actually enrolled). Furthermore, if a charge is otherwise disclosed during a particular quarter (for example, by a confirmation statement after a charge is deducted from an account), then the charge does not have to be disclosed again in a subsequent Quarterly Notice.

4. Disclosures Subsequent to Investment. In addition to the required investment-related information discussed above, the Final Regulations also provide for the disclosure to participants and beneficiaries after they have invested in a particular investment option of any materials that are provided to a plan relating to the exercise of voting, tender and similar rights appurtenant to the investment, to the extent that such rights are passed through to participants and beneficiaries under the terms of the plan.

5. Information Provided Upon Request. Upon the request of a participant or beneficiary, the following investment-related information must be provided: copies of prospectuses (or any short-form summary prospectus approved by the Securities Exchange Commission) or similar documents for non-registered investment alternatives; copies of any financial statements, reports and similar materials provided to the plan; statement of the value of a share or unit of each investment alternative and the valuation date; and a list of assets comprising the portfolio of each investment alternative that constitutes ERISA plan assets, and the value of each such asset (or its proportion of the investment which it comprises).

Format and Distribution Methods for Fee Disclosure Notices. The costs associated with implementing and delivering the Final Regulations' required disclosures can be of concern to plan administrators and employers. Some plan administrators are considering whether they can reduce the costs of complying with the Final Regulations by adding some of the Final Regulations' disclosures to other disclosures and/or notices that they are already providing under other legal rules. The Final Regulations affirmatively permit certain elements of the plan-related information (generally that required to be included in the Initial Notice and Annual Notice) to be provided as part of a summary plan description ("SPD") or periodic benefit statement required under the Pension Protection Act of 2006, provided that the SPD or benefit statement is furnished at a frequency that satisfies the timing rules required by the Final Regulations. The information required to be included in the Quarterly Notice may also be provided as part of a periodic benefit statement to the extent that the timing rules of the Final Regulations are satisfied. The Final Regulations require that investment-related information be provided in a chart or other similar format the permits participants and beneficiaries to compare information. The Final Regulations include, as an appendix, a model comparative chart that may be used by a plan administrator to satisfy the Final Regulations' requirement that a plan's investment-related information be provided in a comparative format. While the model chart is not required to be used and plan administrators have flexibility to create their own formats, a plan administrator that accurately completes and distributes the model chart will be deemed to have satisfied the Final Regulations' disclosure requirements with respect to investment-related information. A copy of the DOL's model chart is attached to this Alert and can also be found at http://www.dol.gov/ebsa/participantfeerulemodelchart.doc. Notably, the DOL has clarified that permitting each individual investment provider to separately distribute its own comparative chart to participants and beneficiaries would not satisfy the comparative format requirement. However, the DOL has indicated that a plan administrator could satisfy the comparative format disclosure requirement by itself combining separate charts in one disclosure—for example, grouped by the type of investment (i.e., stock vs. bond funds) or by investment provider. Although not entirely clear, many in the field interpret the DOL's position as permitting a plan administrator to satisfy the comparative format requirement by combining in one mailing envelope (or other medium of distribution, as applicable), the separate comparative charts that it receives from each individual investment provider.

As another means of curtailing the costs and administrative aspects associated with complying with the Final Regulations, plan administrators and their service providers are considering electronic delivery methods of the required disclosures. Because the rules pertaining to electronic delivery, especially as they apply to disclosures under the Final Regulations, are detailed, somewhat cumbersome and currently in flux, plan administrators will want to proceed with caution if using electronic delivery as a means of satisfying disclosure obligations under the Final Regulations.

Obligation to Comply with Final Regulations is on Plan Administrator

The Final Regulations provide that the compliance obligations rest with the plan administrator of an affected plan. Failure to comply with the Final Regulations' new disclosure requirements could give rise to remedies for breach of fiduciary duty.

Despite this implication of the plan administrator, the Final Regulations give plan administrators protection from liability for the completeness and accuracy of information provided to plan participants and beneficiaries if the plan administrator reasonably and in good faith relies upon information provided by a service provider (e.g., recordkeeper,) or investment provider. In order to meet their fiduciary obligations and the "reasonableness" standard described above, it is suggested that plan administrators periodically review the content and timeliness of information provided by third parties with respect to the Final Regulations.

Effective Date and Disclosures for 2012

The Final Regulations technically apply for plan years beginning after November 1, 2011 (which means the 2012 plan year for calendar year plans). However, the DOL has provided delayed applicability dates to help plan administrators and their service providers transition into the new requirements.

First Initial Notices.

- For calendar year plans and non-calendar year plans with a 2012 plan year beginning on or before April 1, 2012, individuals with existing rights to direct investments of their plan accounts (including those who become eligible between now and the first disclosure date) generally must receive the Initial Notice by May 31, 2012.

- For plans with a 2012 plan year that begins after April 1, 2012, individuals with existing rights to direct investments of their plan accounts generally must receive the Initial Notice within 60 days following the first day of the plan's 2012 plan year (for example, for a plan with a plan year that runs July 1 through June 30, the first Initial Notice under the Final Regulations will be due by August 30, 2012).

First Quarterly Disclosures. The first Quarterly Notices will be due 45 days after the end of the first quarter in which the Initial Notices are required to be made. For calendar year plans and most noncalendar year plans with a 2012 plan year beginning on or before April 1, 2012, because the first Initial Notice generally must be furnished no later than May 31, 2012 (i.e., within the second quarter of calendar year plans), these plans must generally furnish their first quarterly disclosure by August 14, 2012.

Initial Notices After the 2012 Transition Period. After the 2012 transition period, plan administrators will be required to provide an Initial Notice to all newly eligible participants and beneficiaries on or before the date they can first direct their investments.

Relevance for Non-ERISA Plans

While non-ERISA plans (e.g., church plans and governmental plans) are not subject to the Final Regulations, these plans may look to the new disclosure rules as "best practices" and modify their disclosure on a voluntary basis. Also, because service providers are likely altering their disclosures across-the-board to ensure compliance and consistency, they may not distinguish between ERISA and non-ERISA plans in this regard. As such, non-ERISA defined contribution plans may, by default, experience the effects of the Final Regulations.

Other Fee Disclosure Initiatives

The Final Regulations are the third piece of the regulatory initiatives with respect to fee disclosure for employee benefit plans. In 2010, the DOL published interim final regulations requiring new rules for service providers (e.g., investment advisors, recordkeepers, consultants, accountants, etc.) to ERISA pension plans to disclose their compensation and fees to retirement plan fiduciaries of plans from which they expect to receive at least $1,000 in compensation for the indicated services. The purpose of the service provider disclosures is to enable a plan fiduciary to determine if the arrangement with the service provider and the related compensation paid are reasonable and that any possible conflicts of interest are being appropriately addressed. The deadline for the first disclosures under those regulations is April 1, 2012. As a result, plan administrators should expect new disclosures from service providers and possibly changes to current service contracts and arrangements. Plan fiduciaries should be prepared to analyze enhanced disclosures to ensure that fees paid to service providers are reasonable and that potential or actual conflicts of interest are appropriately considered.

In addition, the DOL published new requirements with respect to Schedule C of Form 5500 which were generally effective for the 2009 plan year. These new Schedule C requirements will require administrators of large (i.e., with 100 or more participants as of the beginning of the plan year) ERISA employee benefit plans to provide more detail about fees and expenses from services providers to which they paid $5,000 or more.

Congress has also tinkered in the defined contribution plan fee disclosure area, generally focusing on participant-level disclosures, though no legislative initiatives have yet to become law (notably, some legislative proposals are broader than the DOL's initiatives and contemplate applicability to non-ERISA plans as well).

Action Steps for Plan Administrators

Although the Final Regulations will not technically apply for several months, their potentially onerous and burdensome requirements necessitate that plan administrators and their service providers act quickly to ensure that procedures will be in place to comply with the Final Regulations generally by May 31, 2012. We recommend the following actions for plan administrators and employers:

- Identify all plans for which disclosures to participants under the Final Regulations must be provided. Generally, all ERISA defined contribution retirement plans that permit participants and beneficiaries to direct investments will be impacted.

- Review, contact and coordinate with service providers. It is likely that service providers (especially recordkeepers, investment managers and investment providers) to defined contribution plans have already begun efforts to address the disclosures that will be required by the Final Regulations. It will be important for plan administrators to find out from service providers what types of disclosures are being contemplated and the timeline by which such disclosures will either be provided to plan administrators for them to distribute or directly provided to plan participants and beneficiaries. It will also be important to discuss the method of delivery.

- Consider whether disclosures will be needed independent of those provided by service providers. If the plan has multiple investment providers, it may fall on the plan administrator to compile and distribute relevant investment-related information in a comparative format, as the DOL has indicated that it is not sufficient for each investment provider to separately send the required investment-related information to participants and beneficiaries. Plan administrators will also want to balance the requirements of the Final Regulations with a concern about overloading participants and beneficiaries with too much information.

- Review service provider agreements. While we anticipate that much of the required information will come from service providers, assisting with the new disclosure requirements may not fall within the scope of existing service agreements. If plan administrators expect service providers to share in the responsibility for complying with the necessary disclosures, updates to service contracts and fees may be needed.

- Review and possibly amend current plan documentation. As discussed above, some of the disclosures required by the Final Regulations may be appropriately included in a plan's SPD or benefit statements. Plan administrators should consider whether the distribution timing of such current documents will satisfy the timing requirements of the Final Regulations. Also, plan and trust documents as well as internal delegations may need to be amended to clarify the roles of the plan administrator, staff, directors and service providers with respect to the new disclosure requirements.

- Review the plan's investment line-up and service providers. In the process of dealing with the Final Regulations' onerous requirements, it may become evident that some service providers are better equipped and experienced to assist plan administrators in grappling with the new disclosure requirements. Plan administrators and plan sponsors may also use this as an opportunity to reassess their plans' current investment options and balance the need to provide for diversification with the burdens of disclosing fees, expenses and other investment-related information for a large investment line-up.

- Anticipate impact of new service provider fee disclosure rules. As briefly discussed above, service providers will also have new fee disclosure rules to comply with by the Spring of 2012. Plan administrators should expect to receive new disclosures from service providers. Plan fiduciaries will want to use the enhanced service provider disclosures to ensure that fees paid to service providers are reasonable and that conflicts of interest are appropriately assessed.

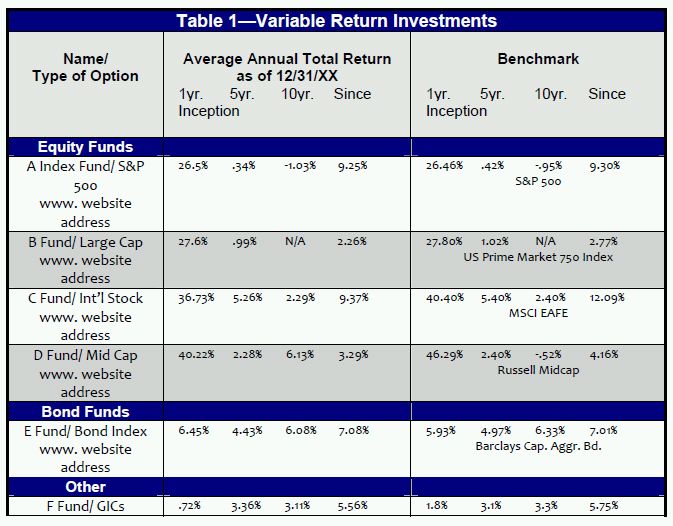

Model Comparative Chart

ABC Corporation 401k Retirement Plan

Investment Options – January 1, 20XX

This document includes important information to help you compare the investment options under your retirement plan. If you want additional information about your investment options, you can go to the specific Internet Web site address shown below or you can contact [insert name of plan administrator or designee] at [insert telephone number and address]. A free paper copy of the information available on the Web site[s] can be obtained by contacting [insert name of plan administrator or designee] at [insert telephone number].

Document Summary

This document has 3 parts. Part I consists of performance information for plan investment options. This part shows you how well the investments have performed in the past. Part II shows you the fees and expenses you will pay if you invest in an option. Part III contains information about the annuity options under your retirement plan.

Part I. Performance Information

Table 1 focuses on the performance of investment options that do not have a fixed or stated rate of return. Table 1 shows how these options have performed over time and allows you to compare them with an appropriate benchmark for the same time periods. Past performance does not guarantee how the investment option will perform in the future. Your investment in these options could lose money. Information about an option's principal risks is available on the Web site[s].

*Generations 2020 composite index is a combination of a total market index and a US aggregate bond index proportional to the equity/bond allocation in the Generations 2020 Fund.

Table 2 focuses on the performance of investment options that have a fixed or stated rate of return. Table 2 shows the annual rate of return of each such option, the term or length of time that you will earn this rate of return, and other information relevant to performance.

Part II. Fee and Expense Information

Table 3 shows fee and expense information for the investment options listed in Table1 and Table 2. Table 3 shows the Total Annual Operating Expenses of the options in Table 1. Total Annual Operating Expenses are expenses that reduce the rate of return of the investment option. Table 3 also shows Shareholder‐type Fees. These fees are in addition to Total Annual Operating Expenses.

The cumulative effect of fees and expenses can substantially reduce the growth of your retirement savings. Visit the Department of Labor's Web site for an example showing the long‐term effect of fees and expenses at http://www.dol.gov/ebsa/publications/401kemployee.html . Fees and expenses are only one of many factors to consider when you decide to invest in an option. You may also want to think about whether an investment in a particular option, along with your other investments, will help you achieve your financial goals.

Part III. Annuity Information

Table 4 focuses on the annuity options under the plan. Annuities are insurance contracts that allow you to receive a guaranteed stream of payments at regular intervals, usually beginning when you retire and lasting for your entire life. Annuities are issued by insurance companies. Guarantees of an insurance company are subject to its long‐term financial strength and claims‐paying ability.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.