IN THIS ISSUE:

Muni Market Holds Its Breath While Politicians Play Chicken With Debt Ceiling

Legal Battle Over California Redevelopment Bills

IRS Scrutinizes Conduit Bonds

Homeownership Rates Decline – Is the American Dream Over?

Bond Market Snapshot

Muni Market Holds Its Breath While Politicians Play Chicken With Debt Ceiling

- As Congress continues its standoff regarding the country's debt ceiling, Moody's Investors Service has placed five triple-A states under review for a possible downgrade in light of their dependence on the ability of the United States to pay its bills. Many states -- including Virginia and Maryland, two of the five states under Moody's scrutiny -- receive a significant portion of their revenues directly or indirectly from federally funded programs. For example, if the U.S. government defaults on its obligations to make Medicare and Medicaid payments, states with a significant population who rely on such payments will suffer economically and be ripe for a rating downgrade. Moody's has already placed the federal government on a credit watch in response to the current debt ceiling debate.

Market analysts differ as to just how a U.S. default might impact the municipal bond market. Most agree, however, that the impact could be severe. In addition to its recent announcement regarding the five potential state downgrades, Moody's has warned that any rating downgrade of U.S. credit, which could occur even without a default, would cause an automatic rating downgrade of approximately 7,000 municipal securities that are backed by U.S. Treasury bonds (i.e., state and local government series securities, or "SLGS"). Although SLGS make up only 5% of the municipal bond market, analysts worry that such a massive downgrade could cause a ripple effect in the market.

Additionally, the federal government pays a significant percentage of the interest on Build America Bonds ("BABs"), a program that was initiated as part of the federal stimulus package in 2009. More than $180 billion in BABs were issued between 2009 and 2010. If the U.S. fails to make the interest payments on that outstanding debt, the bond issuers will have to make good on the payments, further straining state and local finances.

But is a default by the United States really inevitable? Some analysts have suggested that the doomsday scenario being threatened by both parties in Congress – failure to raise the debt ceiling followed by a national default and economic disaster – is merely ammunition in their game of chicken. Those observers believe that one of the parties is bound to blink, rather than risk a serious financial debacle.

Nevertheless, whether the current drama is a serious debate or Congress's version of Y2K, the fact remains that the U.S. Treasury will lose its ability to borrow funds on or around August 2, 2011 should Congress and the President not agree on a compromise to raise the debt ceiling.

Legal Battle Over California Redevelopment Bills

The California Redevelopment Association ("CRA") and the League of California Cities recently filed a lawsuit (the "Lawsuit") with the California Supreme Court challenging the constitutionality of Assembly Bill No. 26 ("ABX1 26") and Assembly Bill No. 27 ("ABX1 27") (collectively, the "Redevelopment Bills"). Governor Jerry Brown signed the Redevelopment Bills into law at the end of June 2011 as part of California's budget package.

The Lawsuit alleges, among other things, that the Redevelopment Bills violate Proposition 22, adopted by California voters in November 2010, as well as certain other provisions of the California Constitution. Proposition 22 prohibits the State from redirecting funds allocated to transportation, redevelopment, or local government projects and services. The Lawsuit also requests the Supreme Court to issue a stay, which would stop the Redevelopment Bills from taking effect while the court considers the case.

On July 28, Kamala D. Harris, Attorney General of the State of California, and Manuel M. Medeiros, State Solicitor General, filed an opposition to the Lawsuit (the "Opposition") on behalf of the State. The Opposition argues that the California Legislature has the power to terminate California redevelopment agencies ("RDAs") because the Legislature created RDAs. The Opposition also argues that the Redevelopment Bills do not violate Proposition 22, because the RDAs have a voluntary means of whether to remain in existence by making certain payments under the provisions of ABX1 27. The Opposition further sets forth agreement with the Lawsuit that the California Supreme Court should expedite resolution of the Lawsuit because the issues presented are significant to the continued operation of the State. Last, the Opposition argues that the Court should not issue a stay of the effectiveness of the Redevelopment Bills, because they are critically important pieces of the State's current budget framework and are essential parts of the budget solution crafted by the Legislature and Governor Brown.

The Redevelopment Bills are briefly described below.

ABX1 26: the "Dissolution Bill"

ABX1 26 eliminates all RDAs as of October 1, 2011. As of the effective date of ABX1 26, (i.e., June 29, 2011), most RDA operations are suspended and RDAs are precluded from incurring additional debt or making payments on existing debt, with the exception of fulfilling enforceable obligations entered into prior to such effective date. "Enforceable obligations" are described in ABX1 26 as bonds, loans, payments required by the federal government or imposed by State law, judgments or settlements, and contracts necessary for the continued administration or operation of the RDA.

ABX1 26 provides for the designation of a successor agency to replace each dissolved RDA. Such successor agency – likely the city or county that created the RDA – will assume the RDA's debts and obligations and expedite the winding down of the RDA's affairs.

ABX1 26 also gives the Controller authority to recover certain assets that were transferred by an RDA after January 1, 2011. Many RDAs transferred property to local governments and other authorities in anticipation of the passage of the Redevelopment Bills. Any financing using RDA funds after January 1, 2011, may be reevaluated by the State to ensure that an RDA has not attempted to circumvent the legislation.

ABX1 27: the "Continuation Bill"

ABX1 27 permits an RDA to remain operable after October 1, 2011, notwithstanding ABX1 26, so long as the RDA adopts an ordinance (a "Continuation Ordinance") by no later than November 1, 2011, declaring its intention to continue operations and promising to make certain annual payments to the State and certain other taxing agencies. The Department of Finance will calculate the appropriate amount that each RDA must deposit into an Educational Revenue Augmentation Fund and a Special District Allocation Fund in order to continue operating after October 1, 2011. According to the CRA, estimated payments for the 2011-12 fiscal year are expected to reach an aggregate $1.7 billion, and estimated payments for the 2012-13 fiscal year are expected to total $400 million.

Impact on RDA Bond Financings

Upon the passage by an RDA of a Continuation Ordinance, the RDA may legally continue its operations, including the issuance of bonds to finance redevelopment activities or refinance outstanding debt. Until the Supreme Court decides the Lawsuit, however, it is unlikely that any bond counsel will be willing to provide a "clean" opinion to support such debt issuance. Consequently, RDAs are effectively precluded from utilizing traditional tax-exempt financing vehicles until the court issues its ruling.

IRS Scrutinizes Conduit Bonds

Conduit bonds provide private developers and nonprofit entities with low-cost, tax-exempt financing for projects that satisfy a public purpose or promote economic development, such as housing, hospitals, and industrial facilities. In a conduit bond financing, a governmental entity issues tax-exempt bonds on behalf of a private entity or nonprofit corporation, usually for a fee. Unlike general obligation bonds, which are secured by the governmental entity's general fund, conduit bonds are generally payable solely from revenues generated by the project being financed.

According to Thomson Reuters, the conduit bond market grew four times faster than the overall municipal bond market during the past five years. According to the research firm Income Securities Advisors, however, while conduit bonds represent only one-fifth of the municipal bond market, they have accounted for two-thirds of all municipal bond defaults in recent years.

In light of the growth and turmoil in this market, the Internal Revenue Service ("IRS") recently appointed an advisory panel to explore possible safeguards. The panel released a report last month, which concluded that local governments frequently misunderstand the tax rules applicable to conduit bond financings and are given insufficient instruction by the IRS. Consequently, the standards for approval and costs vary widely throughout the conduit bond market.

For example, conduit bonds were recently used to finance a casino resort and a private airport. Some local agencies have even begun issuing these bonds for projects in other cities or states, which raises issues of federal regulation under the Commerce Clause of the U.S. Constitution. The report recommended greater oversight of the conduit bond market by the IRS, as well as clearer rules and more guidance for conduit bond issuers.

Homeownership Rates Decline – Is the American Dream Over?

The Research Institute for Housing America recently released a special report that warns of a possible further drop in the rate of homeownership in the United States due to a variety of factors, including the continued tightening of credit.

According to the report, entitled "Homeownership Boom and Bust 2000 to 2009: Where Will the Homeownership Rate Go From Here?," the homeownership rate of 69.2% in 2004 was unsustainable, and the drop to 66.4% in the first quarter of 2011 more closely reflects historical averages. The report concluded that the majority of new homeowners during the last decade were people under 30, and that the increase in the homeownership rate to historic levels was likely attributable to unprecedented access to mortgage credit.

The UCLA Ziman Center for Real Estate recently released a summary of the key findings of the report, which include the following:

- A combination of changes in mortgage credit standards and attitudes towards investment in homeownership likely contributed to much of the boom and bust in homeownership over the decade. As credit conditions loosened in the first part of the decade, many people of all ages who would have remained renters instead became homeowners. With the financial crash, the recession, and tighter credit conditions, homeownership rates have fallen back to levels close to those of 2000 for most age groups.

- Changes in the population's socio-demographic composition and economic attributes also served to lower homeownership rates between 2000 and 2009. For all household heads age 20 to 80, demographic-socioeconomic shifts pushed homeownership rates down by roughly two additional percentage points over the period. These effects were notably different across demographic groups, however. For example, among individuals 25 to 35 years old, shifts in their demographic-socioeconomic attributes pushed homeownership rates down by nearly five percentage points over the 2000-2009 period. For African Americans, the analogous value was roughly one percentage point.

- Individuals appear to have been more risk-seeking in their approach to home buying in the first half of the last decade. This changed to a more risk-averse posture following the real estate meltdown.

- Between 2000 and 2009, there was a one percentage point increase in the homeownership rate. But, were it not for the shifts in access to homeownership through easier credit and the changes in socioeconomic conditions, the homeownership rate would have actually fallen between 2000 and 2005, rather than increasing.

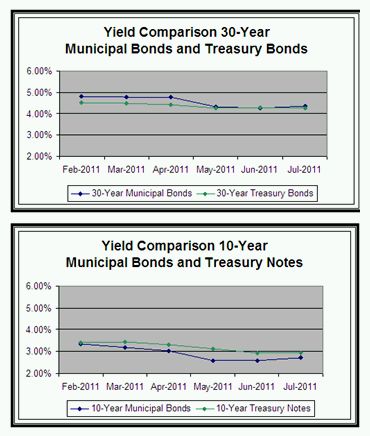

Bond Market Snapshot

In July, yields moved only slightly, increasing from 4.25% to 4.37% for 30-year municipal bonds and dropping from 4.28% to 4.26% on 30-year Treasuries. Yields on 10-year municipal bonds increased from 2.61% to 2.74%, and remained slightly below the 2.95% yield for 10-year Treasury notes.

Source: Bloomberg (www.bloomberg.com)

Goodwin Procter LLP is one of the nation's leading law firms, with a team of 700 attorneys and offices in Boston, Los Angeles, New York, San Diego, San Francisco and Washington, D.C. The firm combines in-depth legal knowledge with practical business experience to deliver innovative solutions to complex legal problems. We provide litigation, corporate law and real estate services to clients ranging from start-up companies to Fortune 500 multinationals, with a focus on matters involving private equity, technology companies, real estate capital markets, financial services, intellectual property and products liability.

This article, which may be considered advertising under the ethical rules of certain jurisdictions, is provided with the understanding that it does not constitute the rendering of legal advice or other professional advice by Goodwin Procter LLP or its attorneys. © 2011 Goodwin Procter LLP. All rights reserved.