- with readers working within the Business & Consumer Services industries

1. Executive summary

The continued economic instability and a tsunami of banking regulation over recent years has brought much change and challenge to the financial services industry. Against the backdrop of constantly changing local and regional regulations (which are not always harmonised), and ever growing political attention, the pace and scale of these developments has arguably changed the foundation of modern banking institutions. It can be argued that change initiated by the financial crisis has brought to the forefront previously forgotten divisions within financial institutions. None more so than Treasury.

In this paper we briefly examine the current landscape in which Treasury operates and focus on the challenges it needs to overcome to achieve its post-2015 vision. Research for this paper includes results from the Deloitte Treasury Survey1 as well as views from external experts and our own expertise within the field of Treasury management.

The major findings of the paper suggest that the Treasury function will be operating within a backdrop of increasing regulation and market volatility for the foreseeable future. Key challenges will focus on funding planning, infrastructure integration, liquidity and capital management.

This paper raises the question as to whether current funding models are fit for purpose to overcome challenges presented by the lack of liquidity and long term market volatility observed in recent years. Development of a robust governance framework coupled with sophisticated funding models is offered as options to address these challenges.

This paper also highlights that a significant proportion of banks continue to use Funds Transfer Pricing (FTP) models based on standard transfer rates. The ability to accurately evaluate and charge business lines will have a significant impact on the overall profitability of the firm.

Regulation has been the primary driver for challenges faced in capital and liquidity management with an increased focus on data granularity, stress testing and reporting capabilities. This paper assesses how the development of an analytical data management framework can provide an enterprise-wide view of liquidity, stress testing and capital usage.

As financial institutions emerge from tackling immediate regulatory demands; Boards are increasingly turning their attention to what they may encounter over the horizon. The Treasury function has a critical role to play in shaping bank strategy as Treasury linked challenges such as deleveraging balance sheets, maximising capital efficiency and improving risk-return ratios are here to stay for the foreseeable future.

2. Background

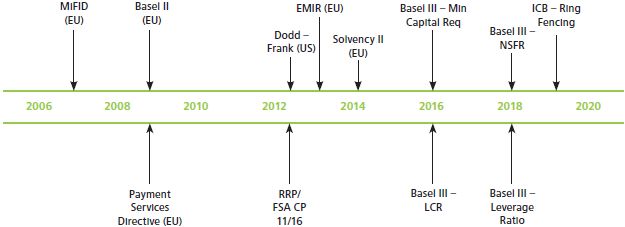

The speed of regulatory change has increased since 2008 and in the coming decade, a raft of new regulation will come into force in an attempt to bring stability and confidence to the industry. This will not only have implications for the wider economy but also for Treasurers as they are forced to react to these challenges.

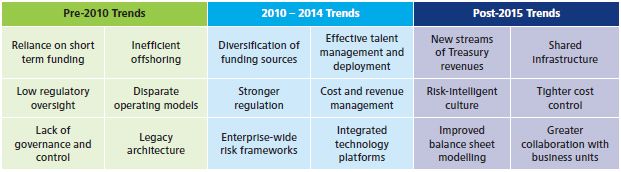

As a result of business, market and regulatory challenges, the following key themes are emerging for the Treasury function:

Note: The above illustration is not intended as a comprehensive list of regulations influencing the global financial services industry. The timeline indicates when a regulation was or is due to be implemented.

Treasury functions have made significant efforts to improve their liquidity management, technology and reporting capabilities, however, this is just the beginning of the journey.

This report examines the case for change and how 2013-2014 is an inflection point for Treasurers to transform and adapt, enabling them to meet the challenges and needs for post-2015.

“ The 2008 crisis was global and financial services were at its heart, revealing inadequacies including regulatory gaps, ineffective supervision, opaque markets and overly-complex products.”

European Commission – Shadow Banking Green Paper [March 2012]

3. Achieving the post-2015 vision

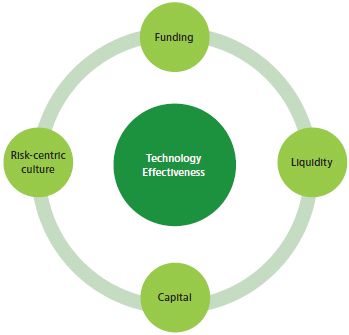

Macro factors such as changing regulation, cost pressures and shifting markets have led to what we see as key themes and trends emerging for the near future and post-2015 for Treasury functions.

Equally, banks as a whole will need to adapt their operating models and align to broader macro factors in order to meet the inevitable demands that will be placed on them, and to effectively position themselves to achieve the post-2015 vision:

-

Funding: building a long term funding plan with improved funding models;

-

Liquidity management: development of ‘best in class’ liquidity capabilities such as high quality stress testing and accurate daily reporting of key liquidity metrics;

-

Capital management: developing an optimal capital structure that maximises equity returns whilst meeting the requirements of regulators and markets;

-

Risk-centric culture: development of a holistic view of the risk across the organisation, building a risk-centric culture to ensure that balance sheets are effectively managed and the implementation of an economic capital model to facilitate strategic decision making; and

-

Technology effectiveness: deployment of improved, flexible tools and technology to meet the changing market demands.

2013-2014 is an inflection point for Treasurers to transform and adapt, enabling them to meet the challenges and needs for post-2015.

Deloitte research

4. Funding: Planning

Funding forms the cornerstone of any Treasury division. The lack of liquidity in the wholesale market observed during the ‘credit crisis’ and its resulting impact on funding resources, caught many Treasurers by surprise. Evidence perhaps that funding planning and review lacked focus in preceding years.

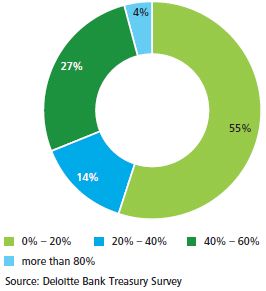

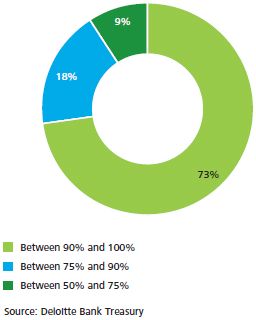

What is the proportion of short-term (defined to be less than a year) wholesale financing?

As Treasury functions look to the post-2015 environment, some of the key challenges being faced in this area and the options which could be considered to address them are outlined below:

1. Banks have made concerted efforts over the past few years to reduce their proportion of short-term wholesale financing however for many, this still represents a large proportion of financing which is susceptible to market volatility and could have a huge impact on organisations who do not have an appropriate strategy in place to deal with this.

Options may include:

-

Development of a clear and robust strategy for the funding sources, mix and uses across the business, detailed to a currency and tenor point level.

-

Development of a regular funding plan governance forum with the business lines. This allows the business lines to challenge the plan and Treasury can provide an update on how the economic environment has changed which may impact the plan.

-

Development of behavioural analytical tools to incorporate into funding models which would lead to be better understanding of key metrics such as attrition rates.

2. Ensuring that management information coming into the Treasury function is timely and accurate is critical to understanding the current and future funding requirements.

Options may include:

-

Development of a governance framework to ensure that inputs to Treasury have the appropriate divisional accountability and controls in place.

-

Establishment of a business line led forum where Treasury can understand the business line performance and the required funding needs for both the current position and any projected future growth.

As institutions consider how to implement these into their broader funding strategy, operational duties towards control and governance will need to be realigned to ensure that there is consistent and granular information coming into the Treasury function on a timely basis.

The impact of the lack of liquidity in the interbank markets during the crisis caught many Treasurers by surprise.

Deloitte research

5. Funding: Funds transfer pricing

As banks integrate their Funds Transfer Pricing (FTP) methodology along the principles of standardisation, granularity, consistency and responsiveness (as outlined in the 2010 Financial Services Authority’s (FSA) ‘Dear Treasurer’ letter), we expect to see the degree of complexity and sophistication employed within FTP models increasing across the industry as banks seek to address the challenges of the post-2015 environment.

A significant proportion of the banks continue to use FTP models based on standard transfer rate charge. As banks continue to assess what business lines they want to be in, the ability to accurately evaluate this will be strongly influenced by the cost of funding (and therefore product profitability) which incorporates the full end to end cost, i.e. the cost for liquidity, risk, term premium, capital and off balance sheet commitments.

Does transfer pricing to the business segments consider different operational characteristics?

Some of the key challenges being faced in this area and the options which could be considered to address them are outlined below:

1. The survey suggested that differing product characteristics are not fully considered within the FTP models for a quarter of banks. An inability to apply a fuller and more reflective cost reallocation can result in incentivising non-strategic behaviours in some business areas at the expense of other businesses.

Options may include:

-

Forge closer working alliances between Treasury, Finance, Risk and the business to ensure that the FTP recharge components includes the full end to end costs based on the characteristic of the trade.

-

Automate the calculation and distribution of FTP charges at trade level, to enable enterprise-wide analysis through full visibility of the P&L and FTP charge on a regular (daily) basis.

-

Upgrade booking systems to allow for granular allocation of costs and the identification of unallocated costs, for example central costs and premiums on debt issuance.

-

Integrate funding modules within the wider treasury infrastructure i.e. ALM modules, to enable the separation of the effects of interest rate changes from the performance of the product/business.

2. Increased focus on Net Interest Income as a metric for measuring profitability, is driving the focused delivery of a consistent cost of funds charge methodology. Inability to achieve this can result in lost market growth and market share.

Options may include:

-

Create a Front Office funding desk which could act as a utility to the various businesses with a mandate to serve as an intermediary between the businesses and Treasury.

-

Develop innovative funding products that attract and meet the demand of long term sophisticated investors, as a means of smoothing the underlying cost base.

Treasury, as the owners of the FTP process, will need to engage with all business lines to ensure its cost reallocation methodology is documented, fully accepted and understood, and makes sound commercial sense across the bank.

Leading banks are moving their FTP approach towards the FSA Principles based approach, in order to more fully re-charge key funding costs with limited tolerance for regional variations.

Deloitte research

6. Liquidity management: Risk management

Looking ahead, new regulation such as Basel lII, Dodd-Frank and European Market Infrastructure Regulation (EMIR) will influence how banks define and manage liquidity risk. The effect will be far reaching in terms of banking business models, capital, technology and collateral management requirements.

Banks need to understand the capabilities of their existing technology and operational infrastructure, and the risks and benefits of directing resources to tactically upgrading these versus investing in new strategic futureproof solutions to meet any stricter future requirements.

How does your organisation plan to address solution requirement to manage liquidity risk under the new Basel III risk management?

As Treasury functions look to the post-2015 environment, some of the key challenges being faced in this area and the options which could be considered to address them are outlined below:

1. Regulatory demands for new Net Stable Funding Ratio and Liquidity Coverage Ratio place greater requirements for holding larger volumes of high quality contingent assets

As the financial safety net previously provided by government and institutional investors diminishes, there will be a greater need to operate a robust and cost effective risk management programme.

Options may include:

-

Strategic redesign of the legal entity structure, such that subsidiaries rather than branches are self sufficient holders of liquidity and capital.

-

Development of comprehensive global liquidity planning and stress testing models which support the flexible migration of liquidity across the bank.

-

Creation of partnership structures to share costs and collateral inventory within their peer group.

These will naturally have operating challenges, such as negotiating service level agreements.

2. Certain regulatory regimes such as China and India, for example, restrict the movement of funds which may lead to excess liquidity build up in one entity whilst another entity may be short of liquidity. Minimising this trapped liquidity can increase business flexibility and reduce maintenance costs.

Options may include:

-

Inclusion of ceiling tolerance limits for products and known areas of capital restriction in liquidity plans, with greater focus on jurisdiction management of liquidity to exploit local knowledge of markets and depositor behaviour.

-

Development of capital optimisation strategies in areas of trapped liquidity, for example the reinvestment of liquidity within local markets to generate returns or the posting of local currency deposits as collateral for cross border trades and dividend payments.

As regulation progresses and liquidity requirements become clearer, banks will need to develop and demonstrate flexible solutions to ensure there are robust risk management practices in place to administer these.

“ The failure of liquidity risk management practices has been at the heart of the evolving crisis in this period.”

Senior Supervisors Group (SSG) – Risk Management Lessons from the Global Banking Crisis of 2008

7. Liquidity management: Reporting

Regulators have increased their focus on liquidity reporting, including data granularity and frequency of reporting requirements, stressing the need to have robust reporting mechanisms. For example, the FSA has asked banks to provide reports at Business Unit level rather than just Group/Entity level under Section 166 reviews; and the adoption of Common Reporting (COREP) by the FSA, requiring banks to report on capital adequacy, Group solvency, credit, market and operational risk.

What percentage of the liquidity position across the institution are visible daily to the Treasury function?

Some of the key challenges being faced in this area and the options which could be considered to address them are outlined below:

-

Incorporation of granular information into liquidity stress test reports such as sophisticated run off profiles, to give more accuracy in Funds Transfer Pricing (FTP) and areas such as contingent funding plans.

-

Development of capabilities to incorporate non financial indicators into MI reports such as market sentiment on potential future impact on liquidity, for example media coverage, internet search hit rates and changes to withdrawal payment types by customer.

-

Standardisation of the definitions of collateral instruments to ensure there is a common understanding across the bank.

-

Ensure that the quality of data is consistent by developing an analytical data management framework which provides an enterprise-wide view of how Treasury will process data. This is particularly important as the Treasury function will need to work closely with each business line to understand how they impact liquidity .

-

Automated firm-wide collection, maintenance and exception management of system data into one central warehouse. This will enable Treasury to provide a firm-wide view in liquidity reporting to the various governance committees (asset liability committees).

Ideally, Treasury functions should have as close to 100% visibility of their liquidity positions as possible. Strong and timely liquidity reporting mechanisms should help to ensure that the data used is reliable and accurate.

“ This drives our proposals for both the granularity and frequency of firms’ reporting to us.”

FSA – CP09/13

8. Capital management: Capital forecasting, planning and reporting

European banks face the equivalent of a EUR 354 bn shortfall in the capital required to comply with the minimum Basel III Core Tier 1 ratio of 7%. Raising capital is one avenue of closing this gap, but it is likely that other paths such as deleveraging balance sheets, capital raising or spinning off risky assets will need to be explored.

Driven by regulation and long term volatility in markets, many banks have been required to upgrade existing capital management business models in order to better align with risk management, meet stress testing requirements and increase granularity of capital reporting. The challenge that remains is determining what the capital structure should look like once these changes are taken into account and what implications it will have for achieving the business plan.

How do you anticipate the new Basel III capital requirements will affect your organisation? (Select all that apply)

As Treasury functions look to the post-2015 environment, some of the key challenges being faced in this area and the options which could be considered to address them are outlined below:

1. Banks operating in multiple jurisdictions are facing substantial challenges adopting to varying regional regulations.

Dodd-Frank and EMIR are examples where seemingly similar regulatory measures require significant

re-investment to achieve compliance. Treasury functions are in turn required to have highly flexible operating models to adapt to this challenge.

Options may include:

-

Development of dynamic data stores and reporting infrastructure to allow for the creation of flexible capital reporting framework.

-

Reduction of financial product complexity to reduce balance sheet complexity. This in turn will reduce capital demands and overheads such as time within the planning, forecasting and reporting process.

-

Development of holistic approaches to capital planning. Targeted relationship management of key capital investors to ring fence access to sustainable and affordable sources of capital which can be used.

2. Increased capital demands on banks calls for greater convergence between the CRO bottom up approach (RWA) and the CFO top down approach (Economic Capital ) for monitoring and appraising capital.

Options may include:

-

Establishing separate Capital Management Committees to supplement forums such as Asset and Liability Committee. This brings together specialist disciplines from across the bank, to drive greater alignment in appraising and awarding the use of capital.

-

Establishing a Front Office based centralised funding desk to gain greater insight into market drivers and achieving greater synergy between capital structure and the firms business plan.

Building an effective capital management framework can help organisations set themselves apart from their peer group in the highly competitive post-2015 environment.

Stronger linkages between Risk appetite setting, credit and market limit setting and capital planning are necessary.

Deloitte research

9. Risk centric culture: Integration with risk management

Given the current climate, focus on risk is perhaps not surprising, however today’s risk management needs far surpass those regarded as the traditional Treasury risks.

Which of the following functions are included in the role of your Treasury department?

As Treasury functions look to the post-2015 environment, some of the key challenges being faced in this area and the options which could be considered to address them are outlined below:

1. As evidenced in the Deloitte Treasury Survey, Treasury functions will need to develop internal risk capabilities to ensure that they meet regulatory demands.

Options may include:

-

Delegation of power to Treasury to develop contagion risk plans so that banks are able to react swiftly to events across industry sectors, sovereigns or individual institutions.

-

Development of a culture with less dependency on quantitative position based models which use historical data (DVAR, VAR, stress tests) and focus on a more balanced skill set that emphasises a holistic approach to risk management, leveraging prior knowledge and market insights.

2. Greater challenges around interest rate risk modelling in the banking books driven, for example, from the treatment of floored variable rate savings products and the resultant margin compression. Understanding of the basis risk position and development of appropriate stress testing is of key importance.

Options may include:

-

Development of better methodologies to measure and manage interest rate risk. For example, net interest income (NII) stress and scenario testing which takes into account the current economic environment.

-

The understanding and communication of the reinvestment risk arising from the investment of non-interest bearing balances, for example in capital & reserves and current accounts in a low interest rate environment.

In the coming years, Treasury will increasingly become an important business partner as tighter regulation is enforced. Understanding the risks that lie within a business and the wider organisation will give both management and regulators comfort that banks are able to cope with shocks in the market.

“ A number of firms also experienced difficulties integrating credit and market risks at the enterprise level.”

SSG – Risk Management Lessons from the Global Banking Crisis of 2008 [Oct 2009]

10. Technology effectiveness: Treasury systems

The use of common data sources within Treasury continues to remain a key area of focus and with the various proposed regulatory changes, this will likely be significant and broad ranging for the Treasury function.

Are common data sources used by the application supporting the following functions?

Some of the key challenges being faced in this area, and the options which could be considered to address them, are outlined below:

1. Historically Treasury systems have grown organically with bespoke development for specific management information requirements. There has always been a case for centralisation, however costs generally outweighed any benefits for investment. Centralisation and streamlining will be critical going forward to ensure that banks are able to meet new regulation reporting, data and granularity requirements.

Options may include:

-

Development of shared capabilities across Treasury, Middle and Back Offices to process trades reducing cost per trade for Treasury Front Office (i.e. executing Treasury decisions such as hedges etc.) and therefore increasing margins.

-

Development of golden sources of data for the main asset classes across Treasury and Markets, in a shared infrastructure ensuring accuracy and consistency of data.

-

Development of tools and systems that facilitate Straight Through Processing and reduce reliance on manual spreadsheets/End-User computing.

2. The recent credit crisis and the on-going Eurozone market fluctuations have shown that organisations need to have an accurate projection of exposures and risk to help them more successfully navigate through these uncertain times.

Options may include:

-

Development of tools to facilitate on-demand risk data (i.e. intraday risk runs) allowing management to take action more swiftly.

Demands on technology are increasingly likely to move towards lower process latency, more-granular data and the flexibility to integrate with other applications used across the bank to meet the needs of the post 2015 era.

Given the dynamic nature of Funding, Liquidity and Capital, managing, data should be consistent across business lines, products, legal entities, and functions.

Deloitte research

11. Conclusion

The pressures that are now facing Treasury functions within banks are unprecedented. With the turbulent economic climate and constantly changing regulatory landscape, modern Treasury strategy must now show that it can match the needs of the organisation, fundamentally supporting the business, and meet the expectations of an increasingly wider set of external stakeholders, particularly regulators.

To address these challenges in a strategic and sustainable way, bank Treasury functions must look not only at their current situation, but also at the challenges that will face them post-2015. They will need to demonstrate:

-

Their efficiency and effectiveness in achieving results in terms of minimising the cost of funding, maximising capital efficiency and deleveraging the balance sheet.

-

Their adherence to new regulatory requirements.

-

Robust governance and risk management.

-

Increased confidence in capital, funding and liquidity management.

-

Enhanced, appropriate and flexible contingency planning for stress scenarios.

-

Underlying technology & data supporting Treasury activities in an efficient and cost-effective way.

Underpinned by operating model enhancements and renewal, bank Treasury functions are becoming better positioned in dealing with the challenges of market driven and regulatory change.

In summary, the global financial crisis has brought the role of the bank Treasury functions increasingly into the limelight. Scarce resources, increased liquidity risk, high complexity, and the need for integrated management of banking assets and liabilities are shaping the decision-making processes in today’s banking institutions.

Evolving regulatory standards will drive complexity for years to come and as a result, banks must review their Treasury function thoroughly in the context of the post-2015 environment: revisiting strategic-planning methods, re-evaluating collaboration mechanisms, and re-tooling the organisation and operating models. Adjustments must be made to risk and performance management metrics, stress-testing techniques, transfer-pricing systems and decision-making processes. As a result, technology and operational hurdles will also have to be overcome.

Decisive action today will ensure an optimised Treasury model for the post-2015 era.

“ The crisis you have to worry about most is the one you don’t see coming.”

Mike Mansfield, American statesman (1903-2001)

Footnotes

1 A Treasury survey was conducted by Deloitte in Summer 2011 which included responses from 25 global banks to understand the role of Treasury in changing marketplace. The survey included study of business practices employed by Treasuries around capital management, ALM, funds transfer pricing, liquidity and risk management. It also included a study in current areas of strategic focus, investment, changing Treasury systems and technology infrastructure landscape.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.