Around the world, the urgency of mitigating climate change is growing, with an increasing focus on lowering CO2 emissions and reducing the impact of development on the environment. Nowhere is this more critical than in Africa, which has one of the world's fastest growing populations, high levels of poverty, inequality and will be disproportionately impacted by climate events including cyclones and drought1. The recent tropical cyclone Idai brought winds and flooding which killed thousands of people, impacted millions of people and damaged infrastructure across Mozambique, Zimbabwe and Malawi. The continent is home to 86 of the world's 100 fastest growing cities, 79 (representing 48% of the Africa's GDP) of which are classified as being at "extreme risk" of climate change1.

Given the strong correlation between energy usage and economic growth, this set of circumstances poses a challenge for African governments, businesses and communities. How can energy access and usage be accelerated to support economic growth, without increasing CO2 emissions and increasing the climate change risks already facing the region?

Almost all African countries have now ratified the Paris Agreement in an attempt to limit the global temperature increase to 1.5 degrees Celsius. Under the Agreement every country has submitted a national climate plan that sets out how they will address climate change and what they will do if increased financing is available. It is expected that these plans will be updated every five years, gradually becoming more ambitious. These plans and the overall agreement have been developed so that wealthier countries (who have so far contributed the most to emissions and climate impacts) must make the greatest financial contributions, allocating funds to climate mitigation in developing countries to supplement their own contributions.

Given the disproportionate impact of climate change on Africa over other continents, the Paris Agreement stipulates:

- US$ 100 billion in climate financing by developed countries to support emerging economies;

- That the goal for African countries is to use existing renewable energy and emissions reduction opportunities to achieve sustainable industrial development with minimal to zero emissions.

African countries now have the opportunity to take advantage of increased financial support and forge a new growth path. Given the region's vulnerability to climate change, African countries must consider how they can grow their energy access and economies while combatting climate change.

Improving energy access, consumption and efficiency in Africa

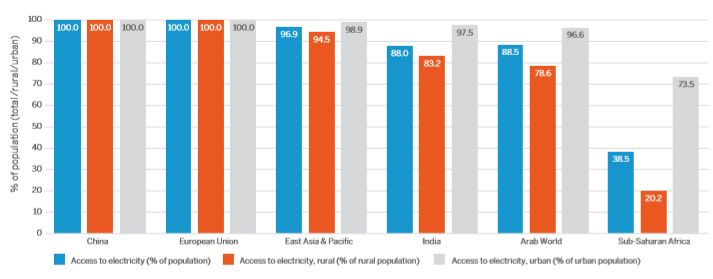

Compared to the rest of the world, Africa has a significantly lower rate of access to electricity, with as many as 600m people without access to electricity across the continent. Based on the latest International Energy Agency (IEA) data available2, Sub-Saharan Africa (the most reliable regional grouping available for the continent for IEA data), has an average electricity access rate of just 38.5%, falling to 20.2% in rural areas. Even in urban areas, more than 1 in 4 people do not have access to electricity.

This compares to electricity access rates of 100% in most developed parts of the world (including the EU and China) and over 85% in emerging economies in India and East Asia. While progress has been made over the last 20 years – the average electricity access across rural and urban areas in Sub-Saharan Africa was just 20.8% in 1995 – it has not been fast enough to close the gap between Africa's electricity access and the rest of the world.

Figure 1: Access to electricity - Selected regions and countries, 20152

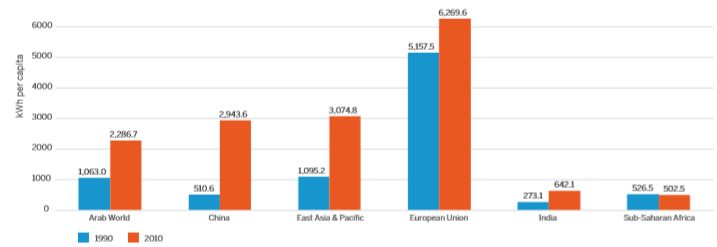

The Sub-Saharan Africa region also lags behind the rest of the world in terms of electricity consumption per capita and electric power distribution and transmission efficiency. Worryingly, it is one of the only regions for which electric power consumption per capita decreased from 1990 to 2010 (the latest year with a consistent global dataset). This is in stark contrast to other emerging economies - China's consumption grew by 476%, the Arab World's by 115%, East Asia & Pacific's by 181% and India's by 135% - indicating economic stagnation and a prolonged period of inadequate investment in electricity generation, transmission and distribution across the Sub-Saharan Africa as its population has grown.

Figure 2: Electric power consumption per capita, 1990 vs 20102

While there are many other factors that contribute to economic growth and the living standards of individual citizens, the impact of electricity access cannot be understated. Energy and electricity are used to power industries from agriculture to financial services, enabling them to grow and employee more people. In the home, electricity reduces the amount of time and effort needed for everyday household tasks, enabling more people (particularly women) to take up employment outside the home and increasing the time available for young people to study as electric lights provide light in in dark evenings. In turn, more educated citizens are able to take up more skilled, higher paid jobs, increasing income levels and standards of living as a result of reliable and affordable electricity access. For these reasons and many more, improving electricity access must be a priority across Africa.

The condition and efficiency of grid infrastructure in the region also needs attention if electricity access is to improve. Sub-Saharan Africa's rate of electric power transmission and distribution losses are better than those in India and the Arab World but still more than double those seen in the EU, East Asia & Pacific and China. Losses as a percentage of output in the region have increased by over a third since 1990, demonstrating a lack of grid maintenance and investment, which will continue to hinder electricity access and the associated economic growth.

Compared to other regions around the world (apart from the European Union), Sub-Saharan Africa does have a fairly diverse energy mix. 50.6% of electricity comes from coal and 20.5% is from hydroelectric and other renewable sources. While uptake of renewables other than hydroelectric power has been slow so far, there is a real opportunity for acceleration in this area, particularly as older coal fired power plants come to the end of their life and their generation capacity needs to be replaced.

FTI's Growth-Emissions Matrix: The low CO2 emission growth path

Figure 3: FTI Growth-Emissions matrix3

FTI's Growth-Emissions Matrix provides an analysis of the historic relationship between GDP, CO2 emissions and electricity consumption per capita. This shows a positive correlation between economic growth, carbon emissions and electricity consumption across different countries and regions. The challenge is for Established Emitters, Problematic Polluters and Potential Renewable Revolutionaries to transition into Climate Change Champions, in other words driving high GDP growth with low emissions.

1. Established Emitters: High GDP and high CO2 emissions

These countries have relied on CO2 intensive growth paths to drive economic development and improve electricity access for their citizens. Typically more economically developed, they demonstrate high electricity consumption, however, their high CO2 emissions also indicate that this economic growth was built on fossil fuel energy generation such as coal, oil and gas.

Established Emitters usually have access to these resources in their own country and have historically been the cheapest way to produce electricity on a mass scale. For example, the United States has large coal, oil and gas reserves and produces over two thirds of its electricity from these sources. Using this energy has enabled the country to grow and develop its economy without being constrained by energy access or prices, which has resulted in high consumption of electricity per capita.

2. Climate Change Champions: High GDP and low CO2 emissions

Countries and regions in this quadrant are also more economically developed and typically have high electricity consumption, but lower CO2 emissions. These Climate Change Champions have managed to successfully transition to lower emission economies, without sacrificing economic growth.

This is mainly due to higher use of renewable energy and nuclear power generation. The high electricity consumption per capita in many countries in this category also demonstrates that low carbon emissions do not need to be a barrier to widespread electricity access or supporting highly developed economies.

Sweden, for example, has managed to decouple growth from CO2 emissions by having a consistent regulatory focus on lowering emissions, including introducing a carbon tax as early as 1991 and offering tax relief to power-intensive industries in exchange for them taking steps to reduce energy use. In addition to government initiatives, Sweden also ranks highly on citizen engagement and awareness of climate change, which has been key for successfully implementing sustainable energy reduction policies across the country.

3. Potential Renewables Revolutionaries - Low GDP and low CO2 emissions

These countries are typically less economically developed and have lower energy consumption and access rates, which for many is the main reason for their low emissions levels. As these countries, many of which are in Africa, strive to grow their economies and improve standards of living for their citizens, the challenge will be how to support economic growth with the lowest possible increases in CO2 emissions.

Some of these countries are starting to move along the right path. Costa Rica, for example, produced over 40% of its electricity from renewables in 2010 and has launched an ambitious economy-wide plan to reach zero-emissions by 2050, while also allowing the country's economy to continue growing. Costa Rica contributes only a tiny part of global CO2 emissions, but its example could be emulated by other developing nations. On the other hand, some countries - such as South Africa - have grown their economies on based on readily available domestic fossil fuels (coal in South Africa's case) and have high CO2 emissions compared to their GDP. The governments of these countries must work hard to correct this relationship and incentivise the economy to move to lower emissions energy generation.

4. Problematic Polluters - Low GDP and high CO2 Emissions

Globally there are very few countries in this category, as the electricity generation that causes CO2 emissions is typically correlated with economic development, but it is important to make sure that countries do not fall into this trap in the future by prioritizing low emissions electricity and power generation.

Taking a sector view, the biggest contributors to emissions production are electricity and heat production, responsible for almost half of all CO2 emissions globally. Sub-Saharan Africa attributes a relatively low proportion of its emissions to manufacturing industries and combustion, which reflects the low level of industrialisation across the economy. However, many African countries are aiming to increase their industrial activity in the coming years to support economic growth. If this is done using energy sources with high emissions, then it could result in worrying growth in CO2 emissions across the continent, growing the economy at the cost of sustainability and future climate change impacts.

Figure 4: CO2 emissions by sector across global regions, 20101

Cost-effective renewable energy technology provides a route to low CO2 emission growth for Africa

Historically, the high costs of utility scale electricity generation from renewable and other low-emissions meant that high government subsidies, industrial incentive programs and high levels of citizen engagement were needed to lower a country's emissions without constraining economic growth. For the governments of many economies in Africa, these were luxuries that were unaffordable at a time when they needed to prioritise basic public services, infrastructure development and servicing high levels of debt. However, over the last 5-10 years the cost of installing and operating renewable energy generation facilities at scale (particularly photovoltaic solar and on-shore wind) has reduced dramatically and now offers a competitive, or in some cases cheaper alternative to traditional fossil fuel power plants. As a result, African economies and governments now have the opportunity to use these technologies to support economic growth with low emission energy sources that also improve energy access and consumption levels across the continent.

Due to its high levels of InSolAtion (Incoming Solar Radiation) and available land space for both solar and wind power generation, Africa is a prime location for renewable energy developments. In addition, the modular, scalable and easily replicable nature of solar and wind power generation technologies means that where sufficient grid connections and storage infrastructure exist, these facilities can be rapidly planned, built and connected over much shorter timeframes than their fossil fuel and nuclear counterparts. For example, large nuclear or coal fired power plants can take over a decade to plan and build, whereas solar farms could be completed in less than 2 years once financing and permits are in place. Of course, larger numbers of these installations would be required, but this could also be used as an advantage, spreading generation facilities across a country instead of concentrating activity in a small number of strategic locations.

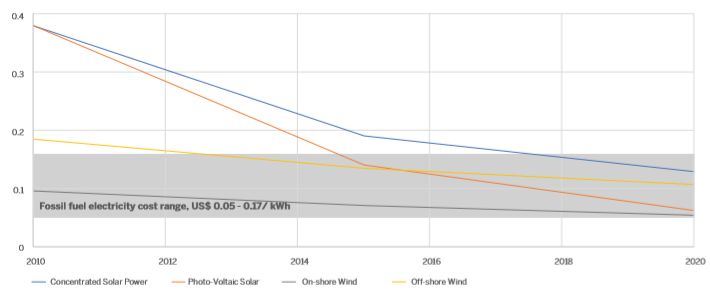

Historically, renewables needed to be heavily subsidised by governments to be commercially competitive, but in recent years the Levelised Cost Of Electricity (LCOE) of utility scale renewable solar and wind energy has fallen significantly4, to the extent that both are now cheaper than almost all new build fossil fuel power plants. In some cases, new build renewables can even be cheaper than continuing to run older fossil fuel power plants that have significant operating and maintenance costs.

Figure 5: Trends in global weighted average levelised costs of electricity, 2010-20204

To continue this downward cost trend in Africa, a number of drivers are important, including:

- Continued technology improvements

- Favourable regulatory and institutional frameworks

- A strong local skill base, including planners, engineers and technicians

- Low offtake and country risks to encourage investment

- Low project development barriers and costs

Bearing these drivers in mind, the latest auction and project-level data indicate that global average costs could fall to as low as US$ 0.05/kWh for onshore wind and US$ 0.06/kWh for solar PV in the near future.

As well as being able to provide low cost electricity without increasing CO2 emissions, renewable energy also plays an increasingly important role in creating direct and value chain jobs across the region, critical considering the high levels of unemployment in many African countries. While the number of jobs created in renewable energy in Africa is still low (322,000 in 2018 according to the IRENA jobs database), globally the industry employed 11 million people in 2018, growing from 10.3 million in 2017.

In South Africa, there are 66,000 people currently employed in the renewables sector, compared to 102,000 in the coal sector and 28,000 in the petroleum sector. This demonstrates the size of the opportunity for job creation if renewable energy was developed at scale across the continent, in manufacturing across the value chain as well as solely in the build and operation of facilities. In addition, IRENA research shows that jobs in the renewables sector tend to be more skilled and have substantially higher wages than the average in the countries these jobs are created in, further adding to the value that renewable energy can add to the African economy.

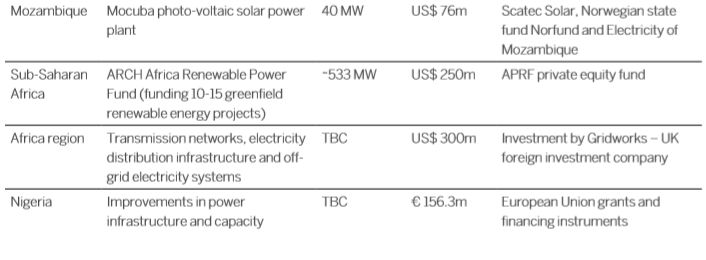

Table 1: A selection of recent renewable energy and electricity access projects and investments in Africa

The use of micro- and off-grid solutions

Another area attracting interest in the African market are off-grid energy solutions such as mini grids (<10MW) and solar home systems (10-100MW). A number of large energy companies such as Shell, EDF and Japanese industrial conglomerate Marubeni have recently invested in off-grid solutions driven by digital technology, including pay-as-yougo energy products for off-grid urban and rural communities. These systems take advantage of the recent reductions in renewable costs and avoid reliance on under-invested grid systems with the aim of relatively quickly (compared to the build of traditional grid infrastructure) bringing affordable, reliable and sustainable energy to those that still cannot access power from national grids.

Global off-grid capacity has more than doubled since 2008 to 8.8 GW, with off-grid solar PV now making up almost a third of all global off-grid capacity. A corresponding increase in global private sector investment in the sector from US$10 million in 2010 to US$ 512 million in 2018 has also been seen, with almost all of investment being in emerging economies such as Sub-Saharan Africa, South Asia and Latin America. Of these regions, almost 80% of investment was in SubSaharan Africa5, although increases in investment of as much as 685% (according to Invest Africa research) would be required to solve Africa's lack of energy access by off-grid solutions alone.

While the advantages of micro-grid and at home solar systems are clear, developers must also consider how they could be connected back into the main grid as access improves over time. This requires a clear regulatory framework to manage the potential feedback of electricity into the grid and the role of 'prosumers' (consumers who also produce electricity) in future distribution networks.

Accelerating low emissions energy access

Recognising the need for African governments, businesses and communities to work together to increase energy generation capacity and access without increasing CO2 emissions is important, but almost equally important is understanding how to accelerate action needed. For the wide-scale implementation of low-emissions power generation and reliable distribution to the 600 million people still without access to power in Africa, appropriate policy frameworks and investment programmes will be critical.

Firstly, government commitments to climate change and emissions targets must be supported by stable, or at least predictable, regulatory frameworks which incentivise and lower the barriers to renewable energy project development. This is particularly important where energy poverty exists, as market forces may not be strong enough to prioritise renewables development where existing 'quick and dirty' power generation such as diesel-powered generators has long been the go-to option.

It must also be understood that there is reduced potential for African countries with fiscal constraints or high levels of debt to channel public money towards renewables and energy efficiency R&D as has been done in wealthier parts of the world such as Germany (where renewable energy subsidies have long been in place) or Japan (which made early investments in hydrogen and fuel cell R&D). Therefore, Public-Private partnerships, FDI or 'mission programme' funding needs to be attracted to develop these projects without adversely impacting public finances.

The IEA World Energy Investment Report 2019 shows that investment allocation to low carbon power and energy efficiencies initiatives across the globe is still insufficient to deliver sustainable development scenarios. Power investment as a whole in Sub-Saharan Africa is lagging behind targets, but progress has been made in some areas. For example, although investment in the sector slowed to just 8% in 2018, it has grown by 80% since 2010 and 65% of this growth came from renewables. On the other hand, spending on grid infrastructure – critical for connecting citizens to electricity – has stagnated over the same period.

Power investment in the region has been hindered by persistent financing risks (often relating to political risk and the financial strain on national utilities operators), challenging project development and insufficient or unstable regulatory frameworks. These factors emphasise the need for governments to work to centrally coordinate energy planning and investment requirements, putting in place the required incentives and fiscal safeguards to encourage private sector investment and international involvement in renewable energy power generation and distribution to consumers.

Moving forward

Nowhere in the world is balancing the energy triangle of security and access, environmental sustainability and economic development more pressing than in Africa, which continues to face an uphill battle to develop its vast natural resources in a way that will benefit its citizens and the environment for the long term. As the vulnerability of the region's fragile economy and fast-growing cities to climate change becomes better understood and more widely publicised, there can be no doubt that encouraging economic growth while minimising the growth of CO2 emissions is a dilemma that the continent must solve.

With the increasing affordability of electricity from renewable energy sources and improvements in technological understanding of how these can be the basis of a reliable energy system, it is possible to build a grid system which provides sustainable electricity to Africa's growing population. Given the limited ability for citizens to absorb tax increases to fund grid infrastructure and renewable energy generation projects, the onus has to be on governments to:

1. Create an attractive environment for investment in the power sector by foreign businesses and governments, including creating policy certainty and economic stability.

2. Work with international finance agencies to help guarantee critical investments in the power sector to further encourage foreign and private sector investment

3. Where required, update energy generation, transmission and distribution policies to support Independent Power Producers (for renewables), micro-grids and prosumers to increase electricity access across the country

4. Reduce and eventually eliminate fossil fuel subsidies in support of lower cost new build renewable power generation facilities

The scale and scope of these actions begins to show the vast commitment required from African governments and their cooperation with international investors, foreign governments, NGOs, research institutes, businesses and communities to successfully solve this dilemma and transition Africa towards a low emission, well developed economy that is supported by an inclusive, sustainable, affordable and secure energy system.

2 https://www.iea.org/statistics/

3 https://www.iea.org/statistics/ , FTI Consulting analysis

4 International Renewable Energy Association (IRENA), Renewable Power Generation Costs in 2017

5 IRENA, 2019

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.