In the accounting world, the hottest topics at the moment surround three major new International Financial Reporting Standards: IFRS 9 Financial Instruments, IFRS 15 Revenue from Contracts with Customers, and IFRS 16 Leases, all of which have particular relevance to the real estate sector. In this article we'll look at the main changes these standards bring and what regulators have said that they plan to enforce—with real estate players in mind.

See you later, regulator

Both the European Securities and Markets Authority (ESMA) and the Comission de Surveillance du Secteur Financier (CSSF) have stated what their main focus areas will be during their reviews of the 2017 year-end financial statements.

ESMA has particular interest in adequate disclosures and sufficient transparency. For example, real estate companies must disclose the expected impact of the implementation of major new standards (i.e. IFRS 9, IFRS 15, and IFRS 16) in the period of their initial application. More details are discussed on our blog post on ESMA's enforcement priorities for 2017.

The CSSF, as part of its enforcement campaign and as required by IAS 8.30 Accounting Policies, Changes in Accounting Estimates and Errors, requires that, when an entity has not applied a new IFRS that has been issued but is not yet effective, the entity shall disclose:

- this fact;

- known or reasonably estimable information relevant to assessing the possible impact that application of the new IFRS will have on the entity's financial statements in the period of initial application.

Don't forget to consider these on your 2017 financial statements!

The biggest change

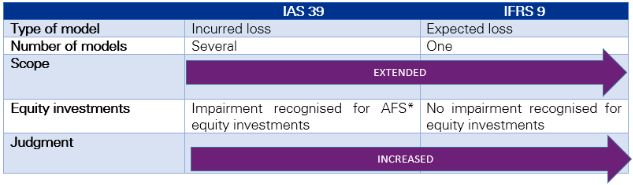

For real estate companies, IFRS 9 Financial Instruments in particular will have an impact. Issuers are now required to make more judgements and estimates than ever before. The principal changes to the new IFRS 9 are as follows:

Common queries

Having advised on many IFRS-related issues, my team and I have come across several common questions:

- In practice, the probability of expected losses cannot be zero. Can we just disclose that there's no significant impact and no analysis to be shown on the notes?

- Can we use the provision matrix structure for the calculation of impairment?

- Can we use historical data to calculate the probability of a lifetime expected credit loss?

- What if there is no credit risk? Do we still need to disclose this?

- If I have no significant credit risk, can I opt for the 12-month approach?

Have you already thought about these? Keep an eye on this blog as we'll continue to explore IFRS—or get in touch with me if you have a specific query.

Takeaway

These standards represent a broad regulatory shift towards more transparent bookkeeping. In line with this, we can expect more IFRS-related change to come to the real estate sector. Real estate companies may find the major new standards particularly challenging in terms of accounting and disclosure requirements, and should therefore concentrate on these aspects as soon as possible.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.