New Zealand can offer excellent opportunities for property investment and development. What should you be aware of when looking to invest in property in New Zealand?

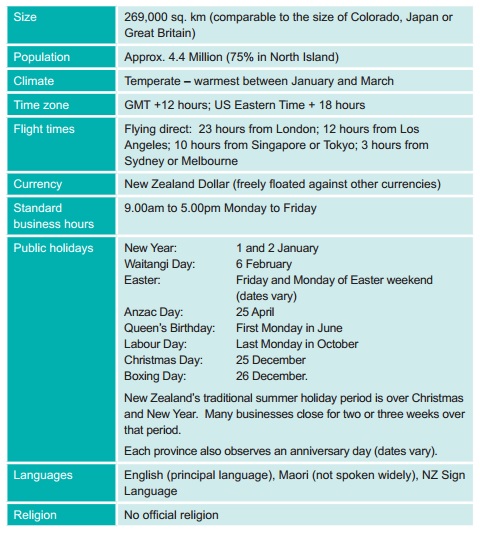

1. A Snapshot of New Zealand

2. General business environment

Legal system

NZ's legal system is based on the common law English system, and much of NZ's legislation is based on English and/or Australian legislation.

The Treaty of Waitangi was signed in 1840, as an agreement between the British Crown and a large number of the Maori of New Zealand. While the status of the Treaty is less than settled, it is widely accepted to be a constitutional document, which establishes and guides relationships between the Crown in New Zealand (as embodied by the New Zealand Government) and Maori.

There is a hierarchy of generalist courts, consisting of the District Court, the High Court, the Court of Appeal and the Supreme Court. Most civil and criminal matters are dealt with by the District Court, with the High Court handling the larger and more serious cases. The Court of Appeal and the Supreme Courts are appellate courts. There are also a number of specialist courts and tribunals, including the Environment Court and the Employment Court. Judges are appointed by the Governor-General on the advice of the Attorney-General and have a strong tradition of judicial independence.

Principal regulators

- The Overseas Investment Office administers foreign investment policy, in accordance with relevant overseas investment legislation (see section 4).

- The Reserve Bank of New Zealand and the Financial Markets Authority are the main regulators of Zealand financial system, investments and financial products. The Financial Markets Authority is also the co-regulator (with NZX Limited) of the New Zealand Stock Exchange.

- The Commerce Commission enforces anti-trust and consumer protection legislation, and the legislation specific to the telecommunications, dairy, and electricity industries.

Registered banks

The principal banks operating in New Zealand are:

- ANZ Bank of New Zealand Limited.

- ASB Bank Limited.

- Bank of New Zealand.

- Westpac New Zealand Limited.

- Kiwibank Limited.

All but Kiwibank are owned by larger Australian banks. Kiwibank is owned and operated through New Zealand's government-owned national postal operator.

Economy and exchange controls

New Zealand is a market economy and operates on a largely deregulated basis. It has been consistently ranked as one of the easiest countries in which to do business.

There are no restrictions on the flow of capital or earnings of a New Zealand business to overseas investors. Profits, dividends, interest, royalties, or management fees can be moved freely either into or out of New Zealand, although payments out of New Zealand may be subject to non-resident withholding tax (see section 8 of this guide).

Money laudering is illegal in New Zealand. A new and enhanced anti-money laundering regime (including customer due diligence, reporting and record-keeping, and enhanced surveillance and enforcement powers) came into force on 30 June 2013.

Accident compensation system

New Zealand has a statutory no-fault accident compensation scheme providing cover for most individuals who suffer a personal injury by accident in New Zealand (ACC scheme). The ACC scheme covers personal injuries suffered by any person in New Zealand, including visitors, and wherever they occur – whether at work or otherwise.

The ACC scheme is funded by the Accident Compensation Corporation, a governmental entity, and is funded largely through levies on employers, employees and taxes on vehicle registration and petrol.

Contract law

Parties are generally free to contract on their own terms with relatively little regulation.

Contract law in New Zealand is largely made up of common law principles, subject to certain statutory requirements regulating matters such as contracting with minors, misrepresentations and contractual mistakes. Certain contracts must be in writing to be enforceable, including those involving interests in land and guarantees.

Contract law applies to overseas-owned persons and entities in the same way as it applies to New Zealand persons and entities. The governing law of a contract between an overseas-owned entity and a New Zealand entity will be determined by the terms of the contract, interpreted in light of "conflict of laws" principles.

Conducting business in New Zealand

Typical options for legal business structures in New Zealand include: limited liability companies, unit trusts, partnerships, limited partnerships, and unincorporated joint ventures, and each structure has its benefits and disadvantages.

For international entities that wish to use the company structure to establish their presence in New Zealand, there are further options, being:

- Registering a branch in NZ;

- Incorporating a local subsidiary in NZ; or

- Acquiring an established NZ registered company.

3. Purchasing property in New Zealand

There are relatively few barriers to purchasing land in New Zealand. Non-resident can purchase land in New Zealand, subject to any requirement for Overseas Investment Office consent (see section 4).

Land registration system

New Zealand has a well-developed land registration system (Torrens system). Under this system, parcels of land have their own titles showing dimensions and location, and recording ownership and other interests affecting the land. The same land laws apply for the whole of New Zealand however land transactions are processed and broken down by Land Information New Zealand (LINZ) into land registration districts.

The Torrens system means that dealings involving land can be conducted in reliance on the land information shown on the register, rather than on a succession of title deeds. LINZ maintains the land register, and guarantees the accuracy of titles. Almost all titles, plans and instruments have been converted into an electronic format, enabling real-time searching and electronic registration of land transactions. The land register is easily searchable for a nominal fee. Duncan Cotterill provides a full title searching service.

Contracts for sale and purchase of land

Land contracts are generally entered into on a caveat emptor basis. Contracts for the sale and purchase of land must be in writing and signed by the parties involved or their authorised agents. Once signed, the agreement becomes legally binding on all parties (ie, 'gazumping' cannot occur once the vendor is bound to the agreement).

It is common, however, for a sale and purchase agreement to be subject to conditions. These may include:

- The buyer being satisfied with the title and local authority information relating to the land;

- The buyer obtaining finance sufficient to complete the purchase;

- The buyer being satisfied with engineering reports and building reports in respect of the land; and

- In the case of a buyer seeking to develop the land, the buyer obtaining relevant resource (planning) consents.

In property purchases, it is usual for a purchaser to pay a deposit to the seller's agent which is released to the seller when the agreement becomes unconditional. Where a real estate agent is engaged by a seller to effect a sale, commission is payable by the vendor, typically at a rate of 4% of the purchase price up to NZ$250,000 and 2% thereafter (plus GST).

Effect of Canterbury earthquakes

The recent Canterbury earthquakes of 2010/2011 have resulted in additional considerations to take into account when buying or selling property, and significant changes to insurance in New Zealand. It is important to investigate not only the condition of any buildings but also the land itself, and to be aware that premiums for some older buildings or those deemed to be "earthquake prone" have risen significantly. Investors need to consider earthquake issues, including insurability, as part of due diligence, and it is essential to seek legal advice before entering into any agreements.

4. Overseas investment regime

Certain investments in New Zealand by "overseas persons" or their associates require the consent of the Overseas Investment Office (OIO) under the Overseas Investment Act 2005 (Act) and Overseas Investment Regulations 2005 (Regulations).

The Act applies to acquisitions by overseas persons of 25% or more direct or indirect ownership and/or control of interests in:

- Significant business assets (exceeding NZ$100 million - although higher thresholds apply for Australian non-Government investors);

- Land that is considered 'sensitive' or 'special' under the Act (discussed further below);

- Farm land; and

- Fishing quota.

If OIO consent is required, it must be obtained before the relevant transaction becomes effective. There are statutory exemptions for certain specific transactions. It is also possible to apply for an exemption in limited circumstances.

Overseas person

An overseas person broadly means:

- Any person who is not a New Zealand citizen nor ordinarily resident in New Zealand;

- A company that is incorporated outside New Zealand; and

- A company, partnership or other body corporate that is 25% or more owned or controlled by an overseas person or persons.

There is also a wide definition of 'associate' in the Act, which will capture most trust, agency or joint venture arrangements, whether there is a direct relationship or not, and whether the arrangement is legally enforceable or not.

Sensitive land (both freehold interests and leases of three years or more)

Briefly, land will be 'sensitive' and require consent under the Act if it is, or includes:

- Non-urban land of more than 5 hectares in area (being more than 50,000m2 or approximately 12 acres);

- The foreshore or seabed;

- Land on certain specified islands;

- Land over 0.4 hectares (being more than 4,000m2 or approximately 1 acre) that includes or adjoins:

-

- any land being a 'reserve' under the Reserves Act 1997;

- any land that is a historic place under the Historic Places Act 1993 or the Resource Management Act 1991;

- any regional park;

- a lake; or

- land that is a road or esplanade or recreational reserve, where that adjoining land is over 0.4 hectares and itself adjoins the sea or a lake;

- Land over 0.2 hectares (being more than 2,000m2 or approximately ½ acre) that adjoins the foreshore.

The definition of sensitive land is very detailed and requires careful checking and analysis from qualified advisers.

Special land

Special land is defined as the foreshore, seabed, riverbed or lakebed. If an investor wishes to acquire sensitive land under the Act and that sensitive land includes any special land, the special land must first be offered to the Government by the owner.

Farm land

Where a proposed purchase involves farm land (being land used exclusively or principally for agricultural, horticultural or pastoral purposes or the keeping of bees, poultry or livestock), that farm land must first have been offered on the open market to persons who are not overseas persons.

Consent process

To obtain consent, the overseas person will need to demonstrate that the purchase will bring benefits to New Zealand which are greater than those which would result from the current ownership. There is detailed and prescribed investment criteria set out in the Act and its Regulations. All applications for consent must be made in the prescribed form, and will be assessed against such criteria. This includes whether the investment will:

- Create jobs.

- Create new technology or introduce new business skills.

- Develop new export markets or increase market access.

- Add to competition.

- Introduce additional investment for development purposes to New Zealand.

- Increase processing of primary products.

In addition, an applicant (or if the applicant is not an individual, the persons with control of the applicant) must:

- Be of good character;

- Have relevant business experience or acumen, and

- Be able to demonstrate a financial commitment to the investment.

There are other factors also regularly considered by the OIO. Consent applications need to cover all these matters and may take significant time to put together. It is important to seek advice early if you think OIO consent might be required in the context of a proposed purchase or transaction.

Consent is usually granted subject to various conditions with which the applicant must comply. Compliance will be monitored by the OIO and will continue until the benefits of the investment have been realised or the conditions have been revoked. Penalties apply in case of a breach of these provisions. In addition, the High Court has the power, on application from the OIO, to order disposal of any property.

Duncan Cotterill has extensive knowledge of the OIO application process and has helped clients to obtain consents for a diverse range of acquisitions, including significant business investment and land acquisitions for forestry, farming, and tourism purposes, as well as for private use.

5. Resource management (planning)

The Resource Management Act 1991 (RMA) governs the use of physical resources in New Zealand, including land, water, minerals and air. The RMA has major implications for property developments. A new development may require a number of consents under the Act before it can go ahead.

Plans and resource consents

Development controls are administered by local government authorities (councils) and are expressed through a range of publicly notified plans. These plans set out rules for activities in various locations or 'zones'. Parties seeking consent to proceed with a development must follow the procedures set out in the relevant plan, and this may involve public participation through the public notification of the consent application.

Types of consents under the RMA include land use consents, subdivision consents, water permits, coastal permits, and discharge permits. These consents are granted by the relevant local authority, which also has wide powers to impose conditions on any resource consent it grants.

Penalties for breach

Non-compliance with the RMA is a strict liability offence (ie, intention or knowledge is not necessary for there to be a breach). Breaches can result in significant penalties, of up to a maximum fine of NZ$600,000 plus NZ$10,000 per day for continuing offences by corporates.

Liability is not limited to the party that actually commits the offence. Directors, trustees or any person concerned in the management of the relevant party can also be held liable for the breach under the RMA.

6. Building

Building consents

The Building Act 2004 regulates and controls building work and the use of buildings in New Zealand.

Every new building and most substantial alterations or additions to existing buildings will require a building consent. On completion of works, a code compliance certificate will be issued, provided compliance with the building consent has been satisfied.

The Building Code sets criteria to ensure buildings are safe, sanitary, have adequate means of escape and, in the case of certain commercial buildings, have access and facilities for disabled persons. Existing buildings, which are being altered, may require upgrading in the course of the alterations in order to comply with these criteria as nearly as is reasonably practicable.

Earthquake-prone buildings

The New Zealand Government has recently announced a revised policy requiring the strengthening or demolition of buildings considered earthquake-prone. New legislation to amend the Building Act 2004 is intended to be introduced later in 2013, and will require building owners to strengthen or demolish earthquake-prone buildings within a set timeframe.

This will have implications for the value of buildings assessed as earthquake-prone, and on commercial leasing and other arrangements affecting those buildings. Prudent building owners and purchasers should undertake a full investigation of all land and buildings before entering into any agreements and leases and advice should be taken to ensure that relevant documentation deals with any issues.

7. Other property issues

Personal property

The Personal Property Securities Act 1999 (PPSA) established a regime whereby priority is determined not by whom holds title to personal property, but by the timing of creation and "perfection" of "security interests". It is based on Canadian legislation, and, under the PPSA, "personal property" is broadly defined and most assets owned or used by a business can become subject to a security interest (excluding interests in land).

The general scheme of the PPSA is that a person looking to acquire personal property is able to search on the Personal Property Securities Register (PPSR) under the name of the vendors to check whether or not the property being sold is encumbered by a security interest. The PPSR is maintained and searchable online at www.ppsr.govt. nz. Duncan Cotterill is able to assist with searches of the PPSR.

Public works and compulsory acquisitions

The Government has the ability to acquire privately-owned land (compulsorily if necessary) if it is required for a public work. Compensation (based on current market value) must be paid if compulsory acquisition occurs.

Maori land claims

Land claims by Maori, the indigenous people of New Zealand, are heard by the Waitangi Tribunal which can then make recommendations to the Government regarding the resolution of the claim. Privately owned land is not subject to return to Maori ownership unless the title to the land has been specifically endorsed to that effect. If it was exercised, the current market value would be paid.

Minerals

All petroleum, gold, silver and uranium existing in land (including under the sea) in New Zealand is the property of the Government. The Government may grant access to and rights to prospect, explore and mine New Zealand's petroleum and mineral estate under the Crown Minerals Act 1991. No person may prospect or explore for, or mine, minerals without an appropriate permit.

8. Taxation

New Zealand has a broad-based tax system consisting principally of:

- Income tax;

- Fringe benefit tax;

- Resident and non-resident withholding tax (RWT and NRWT); and

- Goods and services tax (GST).

Gift duty and death duties are not payable in New Zealand.

Land taxes

No national land tax is payable in New Zealand. Local government authorities can levy taxes (called rates) on all property within their boundaries, and these are the main source of local government revenue. Rates are generally assessed as a percentage of the value of land and/or capital improvements on the land.

Stamp duty

There is no stamp duty payable in New Zealand, whether on the acquisition or transfer of property interests or otherwise.

Goods and services tax (GST)

GST is a consumption tax charged at 15% on the supply of most goods and services in New Zealand.

Personas carrying on a taxable activity (wich is similar in concept to a business, but wider in scope) in New Zealand through wich they will supply goods or services of more than NZ$60, 000 per year must obtain GST-registration, and must change GST on the goods and services they supply. The supplier in the course of their business, and, in this way, the burden of the GST is passed along until reaches the final consumer.

GST is not normally payable in respect of residential property between non-GST registered persons.

Recent changes to GST legislation now require the compulsory zero-rating (CZR) of land transactions between GST-registered persons. The purpose of the CZR rules is to prevent abusive GST arrangements, under which the vendor does not pay GST to the Inland Revenue but the purchaser claims a GST refund. Where the CZR rules apply, GST is calculated on the transaction at the rate of 0%.

There are certain exceptions to these rules, including where the property is intended to be used as a principal place of residence by either the purchaser or an associate. The rules apply to any transaction involving land or where land is a component (even if a minor component). Accordingly, advice should be sought on any acquisition (such as the purchase of a business) involving any interest in land.

Depreciation

Depreciation can be claimed on building fit-outs, but not on most buildings or land.

Capital gains tax

New Zealand does not generally levy tax on capital gains. In certain circumstances, however, the proceeds from the sale of real or personal property (including shares) may be subject to income tax (for example, where the dominant purpose of the initial purchase was to resell the property at a profit).

Income tax

For individuals and companies defined as "resident" in New Zealand, income tax is imposed on worldwide income. Non-resident individuals and companies, on the other hand, are taxed only on income derived from New Zealand, and their tax liability may be reduced by the provisions of an applicable double tax agreement.

Companies (both resident and non-resident) are taxed at 28%. Individuals (both resident and non-resident) are taxed incrementally at between 10.5% and 33%. As noted above, non-residents are taxed only on their New Zealand-sourced income.

Specific tax advice should be taken on residency status in each case as the rules are complex.

Double tax agreements

New Zealand has entered into double tax agreements (or tax treaties) with more than 30 countries to reduce the incidence of double taxation and to provide more certainty for taxpayers operating in foreign jurisdictions.

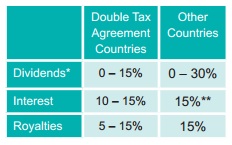

Taxation of payments to non-residents

Payments of dividends, interest and royalties to individuals or companies not resident in New Zealand are generally subject to non-resident withholding tax (NRWT). The rate of NRWT imposed depends upon the type of payment and whether a double tax agreement (DTA) is in place:

*A 0% rate of NRWT applies to fully imputed dividends paid to a non-resident shareholder holding a 10% or more direct voting interest in a New Zealand company or holding less than 10% but whose post-treaty rate is less than 15%. To the extent the dividend is not fully imputed, NRWT will be required to be withheld at 30% (reduced to 15% for countries New Zealand has a DTA with).

** Where interest is paid to a non-resident and a resident (jointly) the applicable rate of NRWT will be higher than 15%.

In the case of dividends, certain royalty payments, and interest paid to non-associated persons, NRWT is generally a final tax for New Zealand tax purposes.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.