The size of Jersey's financial services industry compared to other sectors of the economy is not exceptional, when comparisons are made elsewhere in the UK, according to the recent study into Jersey's value to Britain.

As part of its detailed analysis of the Jersey economy, Capital Economics, a leading macro-economic research company, compared the Jersey economy with the industrial structure of all local authorities in Great Britain with employment levels similar to Jersey.

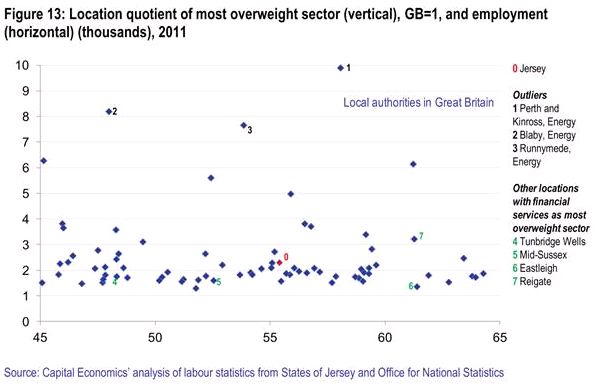

The report author, Mark Pragnell, concluded that 'although the Island has 2 ½ times the United Kingdom's rate of employment in finance, this degree of specialisation is typical of authority areas of a similar size. He added: 'Such concentration on a single sector is unremarkable for an economy squeezed onto a 45 square mile island.'

Using an analysis of labour statistics in Jersey and the UK, the report compilers were able to plot a graph which illustrated that Jersey's finance industry while dominant, was about average in scale when compared to the size of local finance industries in locations in the UK which were also overweight in finance such as in Mid-Sussex, Reigate and Eastleigh. In fact, the statistics showed that locations such as Perth and Kinross in Scotland and Runnymede and Blaby in England were far more reliant on their energy sector in support of their respective economies.

In Jersey, the finance industry accounts for around 25% of jobs compared to 11% in the UK, while 40% of Jersey's gross value added – the contribution to the economy - was accounted for by Finance and related industries, the study concluded.

Geoff Cook, CEO, Jersey Finance Limited, commented:

'While these findings should not in any way detract from the goal of encouraging greater diversity in our economy which the Industry fully supports, it is helpful I believe to have some context when discussing the role of the finance industry within the Jersey economy. It is by far the major provider of tax revenues that pay for public services, but it is not disproportionately over dominant when comparisons are made with similar sized locations in the UK.'

The Capital Economics study concluded that Jersey was an overwhelming benefit to the UK. Among its findings were that Jersey was a conduit for nearly £500 billion of foreign investment into the UK, comprising 5% of the entire stock of foreign owned assets; the island helped the UK generate around £2.3 billion in tax revenues each year and supported an estimated 180,000 British jobs.

Although some UK tax may leak through Jersey – no more than £150 million a year of British taxes could potentially be evaded using Jersey – the amounts were dwarfed by the overall tax contribution by Jersey to the UK exchequer and the report concluded that the recently approved information exchange agreements would substantially reduce or eliminate the potential for tax losses through Jersey.

The findings have been widely disseminated in Government circles in the UK and to finance industry clients of Jersey in London, and there has been considerable coverage of Jersey's value to the UK in leading national media including the Financial Times, the City AM newspaper in London, the BBC and in many trade and professional magazines within the UK. Further coverage of the findings are planned including a feature in a leading magazine with a readership of Westminster MPs, civil servants in Whitehall and parliamentary researchers.

Read more about Jersey's value to Britain here.

Linkedin - www.linkedin.com/company/jersey-finance

Twitter - @jerseyfinance

Youtube - www.youtube.com/jerseyfinance

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.