- within Technology topic(s)

This Jersey Funds Reference Guide (the "Guide") summarises key legal and regulatory issues related to investment funds in Jersey. The Guide should be read subject to the attached diagram at the end of this document.

There are two key issues to consider in relation to investment funds in Jersey, the first being the legal structure by which the fund will be established, and the second being the level of regulation (if any) to which the fund and/or any service provider to the fund will be subject. The Guide will consider each of these issues respectively.

Legal Structure

The main legal structures used for the formation of an investment fund in Jersey are companies, partnerships and trusts. Although different forms of company, partnership and trust are available, the usual form used in a fund context, and the focus of the Guide, are the limited company, limited partnership and unit trust.

The choice of structure is primarily influenced by the proposed terms of the fund, as well as the non-Jersey legal, tax and regulatory considerations applicable to the fund, the fund service providers and the investors in the fund. For this reason, non-Jersey legal and/or tax counsel situated in or qualified to advise on the legal, regulatory and tax considerations of any jurisdiction outside Jersey, which is relevant to the fund, should be engaged as early as possible to assist in settling these aspects prior to proceeding with the establishment of the fund in Jersey.

However, choice of structure may also be influenced by the regulatory classification of the fund in Jersey (certain regulatory classifications only permit the use of certain types of legal structures). Specific reference to the type of legal structure which may be used for funds of different regulatory classification is contained in the footnotes of the Structure Diagram.

Jersey legal structures may be summarised as follows:

i Companies

A Jersey company is incorporated under the Companies (Jersey) Law 1991 (the "Companies Law"), as amended, and is subject to the Companies Law and to the company's adopted form of memorandum of association and articles of association.

Investors in a company may invest in equity as shareholders and/or debt as creditors. There is no limit on the number of shareholders in a public company, whereas a private company is limited to thirty. There are no minimum authorised or issued share capital requirements imposed. Companies may be authorised to issue par or no par value shares, and shares may be redeemed out of capital provided prescribed conditions are met. Different classes of shares carrying different rights and/or restrictions are permissible. The appointed directors of the company manage the business and affairs of the company. Statutory merger and continuation provisions apply under the Companies Law.

The most frequently used company structure in a funds context is a limited company, which limits the liability of a shareholder arising from the shareholder's holding of a share to the amount unpaid on the share. A number of specialist companies are also available, including unlimited companies, guarantee companies and limited life companies.

A further option which is frequently used in a funds context is a cell company. A cell company is a corporate vehicle that is permitted to segregate its assets and liabilities between different cells, with the result that a creditor's recourse against the cell company is limited to whichever cell it transacted with. Where a cell becomes insolvent, the remaining cells of the structure are not affected and continue to operate as normal.

There are two forms of cell company available in Jersey, namely a protected cell company ("PCC") and an incorporated cell company ("ICC"). The cells of a PCC, although treated as companies for the purposes of the Companies Law, are not bodies corporate and do not, therefore, have separate legal identities from their parent cell company. However, the cell of a PCC is able to transact with its parent cell company or another cell of its parent cell company as if it were a body corporate and had its own separate legal identity and capacity. The cells of an ICC are companies for the purposes of the Companies Law and, as such, have separate corporate status from their parent cell company.

ii Partnerships

A limited partnership may be established under the Limited Partnerships (Jersey) Law 1994, as amended (the "Partnerships Law"), and is subject to the Partnerships Law and its adopted form of limited partnership agreement.

Investors in a limited partnership may invest in interests as limited partners and/or debt as creditors.

There is no maximum imposed on the number of limited partners of a limited partnership. Different classes of partnership interests carrying different rights and/or restrictions are permissible. The appointed general partner manages the business of the limited partnership and has unlimited liability for its debts. For this reason the general partner is usually constituted as a limited company. A limited partnership limits the liability of a limited partner arising from the limited partner's holding of a limited partnership interest to unpaid commitments, provided the limited partner does not participate in the management of the partnership.

A number of specialist partnerships are also available. Limited liability partnerships are partnerships with separate legal personality distinct from its partners whilst expressly not being regarded as a body corporate. Stringent financial provisions apply to these structures and they are not used very much for fund structures. Jersey is in the advanced stages of introducing two new partnership structures which may be of use for establishing funds in the future.

Incorporated limited partnerships will also provide for separate legal personality, however, will comprise elements which are similar in substance to those typically encountered with corporate structures. Special limited partnerships will not comprise a body corporate, however, will have the ability to contract and sue and be sued in their own name.

iii Trusts

A unit trust may be established under the Trusts (Jersey) Law 1984, as amended (the "Trusts Law"), and is subject to the Trusts Law and its adopted form of trust instrument.

Investors in a unit trust may invest in units as unitholders and/or debt as creditors. There is no maximum imposed on the number of unitholders of a unit trust. A unit trust is not a separate legal entity as such, but a trust arrangement whereby legal ownership of the fund's assets is vested in a trustee who holds the assets of the fund on trust for the benefit of the unitholders. A unit trust is a form of fixed interest trust. Different classes of units carrying different rights and/or restrictions are permissible. A unit trust limits the liability of a unitholder arising from the unitholder's holding of units to unpaid commitments. A number of specialist trust and hybrid type structures are also available, including discretionary trusts and foundations.

Regulation of Funds

The regulation of Jersey funds may be categorised into two regulatory regimes, based on a distinction between funds which constitute "collective investment funds", as defined in the Collective Investment Funds (Jersey) Law 1988 (the "CIF Law"), and those which do not. There are a number of technical requirements comprised within the definition of a collective investment fund, however, it includes any fund which has as an object the collective investment of capital acquired by means of an offer to the public.

The Jersey Financial Services Commission ("JFSC") is primarily charged with the regulation of funds in Jersey.

All fund types are available as stand alone bespoke structures, however, a commoditised platform or umbrella type structure is also available for a more cost and time effective means of formation. The funds are known as Platform Funds and were developed in Jersey by Collas Crill. A separate briefing note is available on Platform Funds.

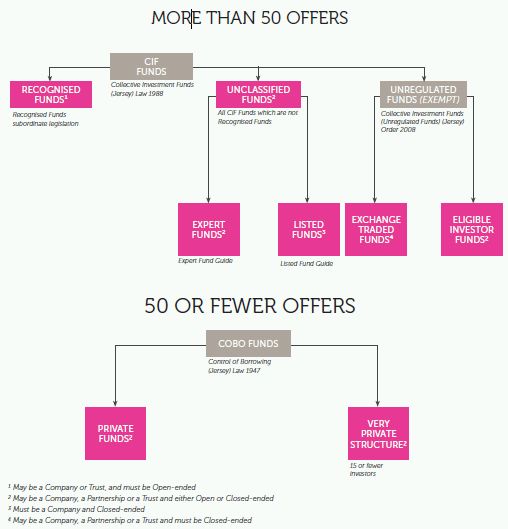

1) More than Fifty Offers

Funds which make a public offer include any fund which makes more than fifty offers or will be listed on any stock exchange within one year of a public offer being made. These funds fall within the definition of a collective investment fund, and are regulated as such, under the CIF Law. Collective investment funds are currently categorised into Recognised Funds and Unclassified Funds, the latter further divided into Expert Funds and Listed Funds. Unregulated Funds are funds which would fall within the definition of a collective investment fund but for the fact that they meet certain requirements which exclude them from the definition of a collective investment fund and, accordingly, the requirements of the CIF Law. The above referred categories of fund may be summarised as follows.

Recognised Funds

Funds intended to be marketed widely to the public in the UK can take advantage of Jersey's designated territory status for the purposes of section 270 of the Financial Services and Markets Act 2000 by complying with the detailed statutory requirements for Recognised Funds. These funds are highly regulated in accordance with Recognised Fund subordinate legislation issued under the CIF Law, including as to investment strategy and restrictions, and investors have access to a statutory compensation scheme.

There is no limit on the number of investors who may invest in a Recognised Fund and also no minimum investment required. Accordingly, these funds are appropriate for retail or public funds. Recognised Funds may take the form of an open-ended company or unit trust only.

Unclassified Funds

All funds which comprise collective investment funds under the CIF Law but are not Recognised Funds comprise Unclassified Funds.

There is no limit on the number of investors who may invest in an Unclassified Fund and also no minimum investment required. There are also no qualifying criteria for investors in Unclassified Funds. Accordingly, although not enjoying the same marketing freedom as Recognised Funds, Unclassified Funds are also appropriate for retail or public funds, and may be used for a wide range of fund types provided they meet the investment strategy and restrictions imposed for the fund type The promoter of an Unclassified Fund must comply with the JFSC's Promoter Policy. A Jersey resident manager and custodian is required where the fund is open-ended, whereas a closed-ended fund does not require a separate custodian. Outsourcing is permitted subject to regulatory policy. Certain investment restrictions and risk diversification strategies are prescribed.

The authorisation process of Unclassified Funds is governed by the JFSC's policy and involves three stages, namely an initial review stage, documentary review stage and formal licensing stage. Unclassified Funds may take the form of an open or closed-ended company, partnership or trust. An Unclassified Fund may list on a stock exchange.

Although Unclassified Funds are in general subject to stringent regulation, certain Unclassified Funds qualify for lighter touch regulation as either Expert Funds or Listed Funds, and unlike Unclassified Funds which do not qualify, may be exempt from some of the requirements referred to above.

Expert Funds

Where the fund fulfils the criteria for an Expert Fund, Jersey applies lighter touch regulation and a more streamlined approval process. These funds are ideal for a wide range of funds which require a minimum initial investment of US$100,000 or currency equivalent, alternatively target sophisticated or high net worth investors. Without limitation, this makes them ideal for alternative investment funds, including private equity, venture capital, property and hedge funds.

The requirements for an Expert Fund are set out in the Jersey Expert Fund Guide issued by the JFSC. The promoter of an Expert Fund will not be subject to regulatory review or approval and an Expert Fund will not be required to adopt any prescribed investment restrictions or risk diversification strategy.

There is no limit on the number of investors who may invest in an Expert Fund. However, an Expert Fund may be offered only to Expert Investors, as defined, who are deemed able to evaluate the risks of investing in an Expert Fund and to bear the economic consequences should the fund fail, and so are deemed to require less regulatory protection. Each Expert Investor must acknowledge in writing a specific investment warning acknowledging their understanding that the fund is suitable only for Expert Investors.

There are ten categories of Expert Investor, however, the most important categories include:

i. an investor who invests a minimum of US$100,000; or

ii. a person or entity (or an employee thereof) whose ordinary business of professional activity includes acquiring, managing or giving advice on investments; or

iii. an individual with a net worth greater than US$1,000,000 (excluding principal residence); or

iv. an entity with assets available for investment of not less than US$1,000,000 or every member, partner or beneficiary of which is an Expert Investor; or

v. a functionary/fund services business or an associate of a functionary/ fund services business to the Expert Fund (or an employee or shareholder thereof).

The offer document for the Expert Fund must contain prescribed basic information. Full details of the fund's investment strategy must be set out in its offering documentation.

An open-ended Expert Fund must appoint a Jersey-resident custodian (save in the case where a prime broker is appointed, where a credit rating of AI/Pl is required).

The Promoter Policy of the JFSC does not apply to an Expert Fund. However, although investment managers regulated in a recognised foreign jurisdiction do not require pre-approval, other investment managers will require preapproval by the JFSC.

An Expert Fund must have an auditor and annual audited accounts must be prepared.

There are no requirements as to investment or borrowing restrictions applicable to Expert Funds, provided that the approach to borrowing or gearing is clearly disclosed in the offering documentation. However, if the Expert Fund is permitted to borrow money in excess of 200% of the net asset value of the fund, full details of the manner in which the risk posed by such borrowing will be managed must be disclosed to the JFSC and in the offering documentation.

The authorisation process itself is quick and straightforward and, provided the JFSC are satisfied that the fund meets the JFSC's criteria for an Expert Fund, the relevant consents, licences and/or permits for a new Expert Fund should be issued within a matter of days. The JFSC will review the application form to confirm that it has been completed properly, but it will not carry out a regulatory review of the Expert Fund, nor will it review the fund documentation, save in exceptional circumstances.

If the fund satisfies the JFSC's criteria for an Expert Fund, the JFSC will authorise the expert fund on the basis of the application form, and will then issue the relevant consents, licences and/or permits.

Expert Funds may take the form of an open or closed-ended company, partnership or trust. An Expert Fund may only list on a stock exchange which permits restrictions upon transfers of interests within the fund.

This is in order to ensure that only Expert Investors are allowed to invest in the fund. An Expert Fund may be established as a Platform Fund, commonly known as a Standard Form Expert Fund ("SFEF").

Listed Funds

A Listed Fund is subject to a similar level of regulation as an Expert Fund, the key difference being that there is no requirement for investors to be Expert Investors and the securities of a Listed Fund must be listed on a recognised stock exchange or market.

The requirements for an Expert Fund are set out in the Listed Fund Guide issued by the JFSC. The key advantage of a Listed Fund over an Expert Fund is that it is possible to establish a Listed Fund with no minimum investment level or other eligibility criteria applicable to the Fund.

There is no limit on the number of investors who may invest in a Listed Fund. Listed Funds may take the form of a closed-ended company only.

Unregulated Funds

Unregulated Funds fall outside the scope of the CIF Law, on the basis that they comply with the criteria set out in the Collective Investment Funds (Unregulated Funds) (Jersey) Order 2008 (the "Unregulated Funds Order").

The Unregulated Funds Order provides for two categories of unregulated funds, namely Unregulated Eligible Investor Funds and Unregulated Exchange Traded Funds.

Both of the Unregulated Funds may be established as a company, trust or partnership. However, the Unregulated Exchange Traded Fund must take the form of a closed-ended fund.

Another common feature of the Unregulated Funds is that there is no requirement to appoint a manager, administrator, Jersey resident directors or auditors to the fund. The JFSC states that an Unregulated Fund must provide written notice, confirming that the fund has been established and that the necessary conditions set out in the Unregulated Funds Order are satisfied.

Unregulated Eligible Investor Fund

An Unregulated Eligible Investor Fund is a scheme or arrangement which is available to Eligible Investors. These funds are ideal for a wide range of funds which require a minimum initial investment of US$1 million or currency equivalent, alternatively target sophisticated or high net worth investors. Without limitation, this makes them ideal for alternative investment funds which meet their requirements, including private equity, venture capital, property and hedge funds.

There are ten categories of Eligible Investor, however, the main categories include:

i. a person who has agreed to pay consideration of not less than US$1 million, or the equivalent of that amount in another currency, for the subscription, purchase, exchange or acquisition;

ii. a person whose ordinary business or professional activity as principal or agent includes or could be reasonably expected to include: (1) the acquisition, underwriting, management, holding or disposal of investments, whether as principal or agent, or (2) the giving of advice on investment;

iii. a functionary in relation to the fund or an associate of such a functionary (or an employee, director or shareholder of, or consultant to, such a functionary or associate who is acquiring the investment as remuneration or reward); or

iv. an individual whose property has a total market value of not less than US$10 million or the equivalent of that amount in another currency.

The investors will be required to acknowledge in writing their acceptance of the risks involved in a prescribed form. In addition, the fund must take steps to ensure that its investors meet the legal requirements to invest in the fund.

There is no limit on the number of investors who may invest in an Eligible Investor Fund. The fund may only list on a stock exchange which permits restrictions upon transfers of interests within the fund. This is in order to ensure that only Eligible Investors are allowed to invest in the fund. An Eligible Investor Fund may be established as a Platform Fund, commonly known as a Standard Form Unregulated Fund ("SFUF").

Unregulated Exchange Traded Fund

An Unregulated Exchange Traded Fund is a form of unregulated listed fund which need not be regulated by the JFSC on the basis that it is already regulated by a stock exchange. In order to qualify under this category the units in the fund must be listed on one or more of the exchanges listed in the Unregulated Funds Order.

There are no specific criteria for investors to be eligible for an Unregulated Exchange Traded Fund. There is no limit on the number of investors who may invest in an Unregulated Exchange Traded Fund.

2) Fifty or Fewer Offers

Where the fund is not offered to more than 50 investors and is not to be listed within one year, registration under the CIF Law is not required. The fund is instead authorised by the issue of a consent under the Control of Borrowing (Jersey) Law 1947, and the subordinate legislation made thereunder in the form of the Control of Borrowing (Jersey) Order 1958 (collectively, "COBO"), by the JFSC.

Regulatory requirements in relation to COBO-only funds are governed by policy rather than statute and are flexible. The promoter of a COBO-only fund would need to comply with the Promoter Policy.

Although there is no prescribed minimum initial investment for a COBO-only fund, the JFSC is particularly flexible in its approach to COBO-only funds which qualify as a "professional investor regulated scheme", where each investor is either qualified by the nature of its business or by making a minimum investment of £250,000 and signs an investment warning confirming that they are a "professional investor".

The offer document is to be reviewed by the JFSC. The requirements are generally less onerous than those for funds regulated under the CIF Law.

A Private Fund and Very Private Structure may take the form of a open-ended or closed-ended fund. Neither a Private Fund nor a Very Private Structure may be listed.

The JFSC's published time frame for its response to an application for the establishment of a COBO only fund is as for public funds (see above). However, the JFSC has indicated that the time taken will often be well within that published time frame.

Private Funds

An investment vehicle which may be made available to a restricted circle of persons, the meaning of which is negatively inferred from the definition of a collective investment fund under the CIF Law, but basically means not more than fifty investors.

Very Private Structure

An investment vehicle established for a small number of pre-selected investors (up to a maximum of fifteen) is treated in the same way as a joint venture company. Offers as well as investors may not exceed fifteen. A Very Private Structure can be established on an expedited basis, at modest cost and with minimal regulation. A Very Private Structure may be established as a Platform Fund, commonly known as a Standard Form Very Private Structure ("SFPF").

Fund Services Business

The Financial Services (Jersey) Law 1998 (the "FSJ Law") provides that a person carries on fund services business if by way of business the person is:

i. a manager, manager of a managed entity, administrator, registrar, investment manager or investment adviser;

ii. a distributor, subscription agent, redemption agent, premium receiving agent, policy proceeds paying agent, purchase agent or repurchase agent;

iii. a trustee, custodian, depository;

iv. a member (except a limited partner) of a partnership, including a partnership constituted under the law of a country or territory outside Jersey;

In relation to an Unclassified Fund or an Unregulated Fund. Registration requirements apply to persons carrying on fund services business, unless a relevant exemption applies under the FSJ Law or otherwise.

The conduct of fund services business is subject to the Codes of Practice for Fund Services Business issued by the JFSC.

The CIF Law provides for the regulation of functionaries of Recognised Funds.

Although service providers to COBO-only funds do not fall within the definition of fund services business under the FSJ Law and are also not functionaries under the CIF Law, regulatory requirements may apply under COBO or the FSJ Law, subject to certain exemptions where applicable. However, the provision of services to COBOonly funds does not constitute fund services business and is not subject to the Codes of Practice for Fund Services Business issued by the JFSC.

Platform Funds

Further information on the SFEF, SFUF and SFPF are available in the briefing note issued by Crill Canavan and entitled Platform Funds.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.