Introduction

An Exchange Traded Fund ("ETF") is an investment vehicle that, in its typical form, is designed to enable investors to track a particular index through a single liquid instrument that can be purchased or sold on a stock exchange.

An ETF offers characteristics of an investment fund (such as low costs and broad diversification) but also characteristics more commonly associated with equities (such as access to real time pricing and trading).

ETFs have seen dramatic growth in recent years, in terms of assets invested and the number of products available, in contrast with the net outflows being currently experienced by many traditional investment funds. The scope of the products on offer has also widened with ETFs covering a broad range of asset classes as well as specific sectors.

Set out below is a summary of some of the main advantages that ETFs offer to investors, a brief overview of how an ETF is structured as well as how ETFs can be established in Ireland within the UCITS framework.

What is an ETF?

An ETF is a particular type of investment fund structured to facilitate trading of its shares on an exchange. ETFs generally function as index tracking funds, i.e. they provide their investors with an exposure to the securities in an index. The listing on an exchange means the ETF shares can be bought and sold by investors - on an intra-day basis and using realtime pricing - much like an equity security.

Advantages of an ETF

Some of the particular aspects of ETFs that make them an attractive investment for a broad range of investors are outlined below.

Low costs

In almost all circumstances, an ETF will not be required to sell securities within its portfolio, nor will it typically be required to purchase such securities directly on the open market, due to the in kind subscription and redemption arrangements regarding creation units, discussed further under "ETF construction", below.

The decreased level of portfolio transactions means that the ETF is subject to lower transaction costs than a traditional index tracking fund, in addition to the generally lower management costs of pursuing an index tracking strategy when compared with an actively managed fund.

As a result, ETFs offer a lower cost alternative to other investment funds where the average expense ratio of an ETF might be 0.25 per cent for an ETF compared to 1.5 per cent for an actively managed fund. However, transactions in ETF shares by investors in the secondary market may be subject to brokerage commissions and/or transfer taxes associated with the trading and settlement through an exchange.

Diversification and choice

Investment in an index tracking product will automatically provide diversification across the sector covered by the index, the actual level of diversification being determined by the specific index.

Available ETFs cover indices on most major equity markets as well as regional, industry specific and country-specific sectors. ETFs also cover other asset classes such as fixed income securities with the range of available ETFs continuing to increase. This means that with an ETF, an investor can gain a broad exposure to any number of markets/sectors through the purchase of a single security.

Transparency

As the components of the basket for the purchase or sale of creation units are published on each dealing day, an ETF provides greater portfolio transparency than a traditional investment fund which would not publish portfolio holding information on a daily basis and, if published, would generally be made on a lagged periodic basis only.

Real-time pricing and intra-day trading

Intra-day trading enables investors to buy and sell their shares at any time throughout the day, unlike traditional investment funds which would generally deal only once a day (or less frequently). ETFs therefore offer greater liquidity and opportunities to avail of intra-day pricing changes.

In addition, by virtue of being listed on an exchange, investors purchase ETF shares with real-time prices. This differs from traditional investment funds, the shares/units in which are purchased at forward prices. Shorting and margin As an ETF share is an exchange traded security, it can be treated by investors similar to an equity security and so can be sold short or purchased on margin, subject to regulatory restrictions that may apply.

Flexibility and range of investors

As ETFs can be openly purchased on an exchange there is normally no requirement to open a specific account or provide any particular documentation specifically for the ETF, although an account with a broker/clearing system will generally be required to trade listed securities.

ETFs are generally available to both retail and institutional investors. They attract both active traders and long-term investors. Investment managers may utilise ETFs where they find it difficult to achieve out-performance of a market in a certain sector or region.

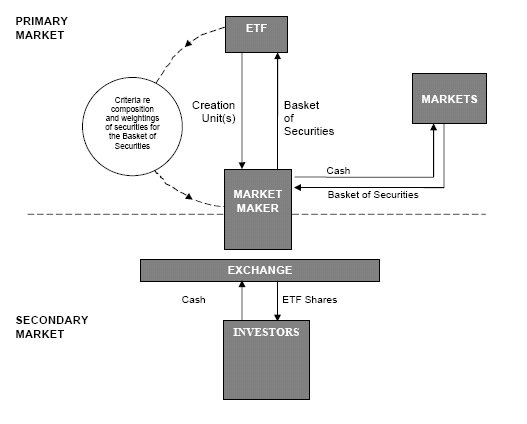

How is an ETF constructed?

ETFs are typically established as index tracking funds where they aim to track an index by holding a portfolio of securities that represents or replicates the index, to the extent possible. As a passive investment vehicle, the only trading activity conducted by the ETF itself would be to reflect changes made to the index at a rebalancing interval by making a corresponding change to its own portfolio.

The ETF will be structured to offer shares to investors on the secondary market, facilitated by the use of banks/brokers who effectively act as market makers between the ETF and the investors subscribing for shares with the market makers being the only direct investors in the ETF.

Primary market

The market maker subscribing directly to the ETF for shares will become an "Authorised Participant" registered with the ETF's administrator.

Typically, subscriptions and redemptions in the ETF will be for one or multiple "creation units" comprising a designated number of shares (50,000 for example) corresponding to the underlying assets within the ETF. These shares will then be sold by the Authorised Participant on the secondary market.

The issue price of a creation unit corresponds to a pre-established fractional value of the underling index that is set at the time of the initial offer of shares by the ETF. Payment for a creation unit will generally be given in kind by the delivery of a basket of securities which closely replicates the composition and weighting of the securities held within the relevant index (although cash subscriptions may also be facilitated and the subscription may also include a cash "balancing amount" to cover any disparity between the value of the creation unit and value of the securities delivered). A list of acceptable securities and their respective weightings (representing the securities and weightings, or components, of the index) comprising the basket for the purchase or sale of such creation unit is published and made available by the ETF on each dealing day.

Secondary market

The ETF shares received by the Authorised Participant will be listed on an exchange (such as NYSE Arca or the London Stock Exchange) where they can be freely purchased and sold, with the settlement of trades in ETF shares on an exchange being facilitated through one or more recognised clearing and settlement systems, for example, CREST, Clearstream or Euroclear.

As a result, investors can buy and sell ETF shares in large or small amounts through the exchange on a real time, intra-day basis without attracting subscription or redemption charges.

The price of ETF shares traded on the secondary market will be determined by the market but should correspond approximately to the net asset value per share of the ETF based on the value of its underlying assets. Generally an indicative net asset value is issued by or on behalf of the ETF at regular periods intra-day. This obliges Authorised Participants to quote bid/offer spreads on the secondary market within a few basis points of the most recent indicative net asset value. The bid/offer spreads allows the Authorised Participant to cover the risk of buying/redeeming shares in the primary market at a price different to the price the shares are sold/bought on the secondary market. The Authorised Participant creates a market by subscribing/redeeming in the primary market in order to settle trades which it has made with investors on the secondary market.

Pricing and arbitrage

As both the underlying securities and the ETF publish closing prices and the ETF portfolio holdings are disclosed, Authorised Participants can take advantage of the disparities between the net asset value of an ETF (which will vary in accordance with the changes in the price of the underlying securities) on the one hand and the price of ETF shares on the secondary market (which will vary in accordance with the supply and demand for such shares) on the other hand by either (a) purchasing ETF shares on the secondary market (trading at a lower price to ETF shares in the primary market) and redeeming them for underlying securities which they can then sell at a profit; or (b) shorting ETF shares in the secondary market (trading at a higher price to ETF shares in the primary market), purchasing the underlying securities and subscribing in kind for ETF shares on the primary market in creation unit size denominations and delivering the ETF shares on the secondary market to settle the short position. This arbitraging activity operates as a market force ensuring that the ETF prices do not vary to a significant extent from the prices of the underlying securities.

Custody

When ETF shares are bought and sold on the open market, the underlying securities delivered to the ETF by the Authorised Participant(s) as payment for the creation units remain in the ETF's custody account and are not impacted.

Redemptions

Secondary market redemptions are satisfied by selling the ETF shares on the exchange. Primary market redemptions may be effected by the Authorised Participant by redeeming in kind with the ETF directly. Such redemptions must be in portions corresponding in size with one or more creation units with the creation unit(s) being cancelled and the corresponding underlying securities delivered to the Authorised Participant.

Establishing an ETF as a UCITS fund

To date, many ETFs in Ireland have been set up under the UCITS regime, authorised by the Irish Financial Regulator as an undertaking for collective investment in transferable securities (UCITS) pursuant to the European Communities (Undertakings for Collective Investment in Transferable Securities) Regulations, 2003 (S.I. No. 211 of 2003), as amended (the "UCITS Regulations").

UCITS funds benefit from the principle of mutual recognition within the EU and can be marketed in other member states under the UCITS "passport" once authorised in one EU Member State.

While a UCITS fund may be established as a unit trust or common contractual fund, the listing on an exchange generally means that, in a typical case, an ETF would be constituted in Ireland as a variable capital company (VCC) with limited liability.

UCITS Funds – Index Tracking

Importantly, as with any other UCITS, an ETF set up under the UCITS Regulations would have to comply with UCITS rules relating to index replication.

(i) 5/10/40 Rule

Under what is commonly known as the 5/10/40 rule, a UCITS may

invest no more than 10% of its net assets in transferable

securities or money market instruments issued by the same body,

provided that the total value of transferable securities or money

market instruments held in issuing bodies in each of which it can

invest more than 5% is less than 40%. This fundamental UCITS

principle did create problems for UCITS which wished to track an

index where the weighting of a constituent element of the index

exceeded the 5% limit or where the relationship between two or more

constituent elements of the index meant that they were considered

to constitute a single issuer resulting in an aggregation of the

exposure. UCITS III then introduced more flexible provisions,

specifically for index tracking UCITS funds.

(ii) 20% and 35%

Rule Under UCITS III, a UCITS whose policy is to replicate an index

may invest up to 20% of net assets in shares and/or debt securities

issued by the same body, with the 20% limit being raised up to 35%

in the case of a single issuer where justified by exceptional

market conditions. This flexibility is permitted where the relevant

index is recognised by the Financial Regulator on the basis that it

is sufficiently diversified, it represents an adequate benchmark

for the market to which it refers and it is published in an

appropriate manner.

(iii) Index replication

The reference to "replication" of the composition of a

shares or debt securities index is considered by the Financial

Regulator to mean replication of the composition of the underlying

assets of the index including the use of derivatives or other

permitted UCITS efficient portfolio management techniques and

instruments.

(iv) Sufficient diversification

Although somewhat circular, reference to an index's composition

being diversified refers to an index which allows for a maximum

weighting per issuer of 20% with a capacity for a single

constituent to exceed 20% but not exceed 35% of the index.

(v) Adequate benchmark

The reference to the index representing an adequate benchmark for

the market to which it refers is a reference to an index whose

provider uses a recognised methodology which generally does not

result in the exclusion of a major issuer of the market to which it

refers.

(vi) Publication

The requirement that the index be published in an appropriate

manner is taken as a reference to an index which is accessible to

the public and where the index provider is independent from the

index replicating UCITS. Note, however, that this second

requirement does not preclude index providers and the UCITS forming

part of the same economic group provided that effective

arrangements for the management of conflicts of interest are in

place.

(vii) Eligibility of assets comprising the index

If an ETF wishes to track an index by directly holding components

of the index (rather than employing derivatives to gain synthetic

exposure to the components of the index), then, as a UCITS, such an

ETF could only target indices comprising eligible assets for UCITS

investment. This would exclude, for example, commodities indices.

An Irish UCITS fund may, subject to compliance with certain

requirements of the Financial Regulator, gain exposure –

only via derivatives - to a financial index comprised of

non-eligible assets.

Prospectus Disclosure Requirements

The Financial Regulator's Guidance Note 2/07 requires that, where indices are used for investment purposes, the prospectus must provide sufficient disclosure to allow a prospective investor to understand the market the index is representing, why it is being used as part of the UCITS investment strategy, how the investment will be made (i.e. directly through investment in the constituents or indirectly through derivatives) and where additional information on the index may be obtained.

Legal/regulatory features particular to an ETF

Key considerations that must be addressed when establishing an ETF include:

Construction

The structure will normally provide that only Authorised Participants can directly subscribe for and redeem shares in the form of creation units.

The terms and conditions applicable to an application for the issue of shares directly in the ETF by an Authorised Participant, together with subscription and settlement details and procedures and the timeframe for receipt of applications, will be specified in the ETF's prospectus.

Clearing and Settlement Systems

Trading and settlement of ETF shares in the secondary market is facilitated through one or more clearing and settlement systems. Some of these systems provide for the trading and settlement of shares in dematerialised form, i.e. shares which are transferred without requiring the transfer to be evidenced by written transfer of ownership.

The Irish Companies Act 1990 (Uncertificated Securities) Regulations 1996 provides for an electronic share settlement system known as CREST which provides for (i) real time settlement for a range of securities traded on the London Stock Exchange and Irish Stock Exchange; and (ii) the ability to hold securities in dematerialised form.

The merger of CRESTCO (which operates the CREST system) and Euroclear Group plc has created Europe's largest settlement services provider, operating under the Euroclear brand name.

Other clearing and settlement systems (such as Clearstream) facilitate the trading and settlement of shares which although are not dematerialised are immobilised, i.e. one initial share certificate is issued which is then held at a depository within the system with all the details of initial beneficial ownership and subsequent changes recorded in electronic media rather than on share certificates.

Registrar and Transfer Agent/Depository – Clearing System Member

Another requirement if shares are to settle on an electronic clearing system is that the ETF must appoint a registrar and transfer agent or depository which is a member of the electronic clearing system.

The transfer agent/depository will maintain a sub-register for ETF shares purchased on the electronic clearing system and will process the transfers involved. The transfer agent/depository will not be required to conduct anti-money laundering checks in relation to investors purchasing and selling ETF shares through the electronic clearing system.

The transfer agent/depository will be entitled to receive a fee out of the assets of the ETF for its services.

Listing on the London Stock Exchange / Recognised Scheme Status

Many Irish UCITS ETFs are listed on the London Stock Exchange which requires that a set of listing particulars is prepared in accordance with the Listing Rules under Part VI of the UK Financial Services and Markets Act 2000 ("FSMA"). This is generally facilitated by incorporating necessary disclosures required by the UK Listing Authority into the ETF's prospectus.

Certain rules regarding publication of net asset value information will also apply as a result of the listing.

In addition, under chapter 16 of the UK Listing Rules, the ETF will also need to obtain "recognised scheme" status under section 264 of the FSMA. In order to do so, it needs to appoint a UK paying agent for UK resident shareholders in relation to dividend payments and to provide a representation office for the ETF in the United Kingdom.

The UK paying agent will also be entitled to receive a fee out of the assets of the ETF for its services.

The future for ETFs in Europe

While this certainly remains a turbulent time for the investment funds industry, the European market in ETFs seems set to continue its expansion in the short and medium term as ETFs offer retail and institutional investors quick, inexpensive access to top performing indices and sectors. Coupled with the increasing success of UCITS brand worldwide and the continuing development of the UCITS framework, UCITS ETFs promise to offer exciting opportunities for asset managers and investors alike.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.