In a recently decided case entitled Adiveppa & Ors. Vs. Bhimappa & Anr. being Civil Appeal No. 11220 of 2017, the bench comprising of Hon'ble Mr. Justice R. K. Agrawal and Hon'ble Mr. Justice Abhay Manohar Sapre of the Supreme Court of India, vide its order dated September 06, 2017, has held that all assets pertaining to Hindu Undivided Family (HUF) are to be treated as joint property of the HUF, unless the contrary is proved as self-acquisition of property through valid documents.

FACTS IN BRIEF

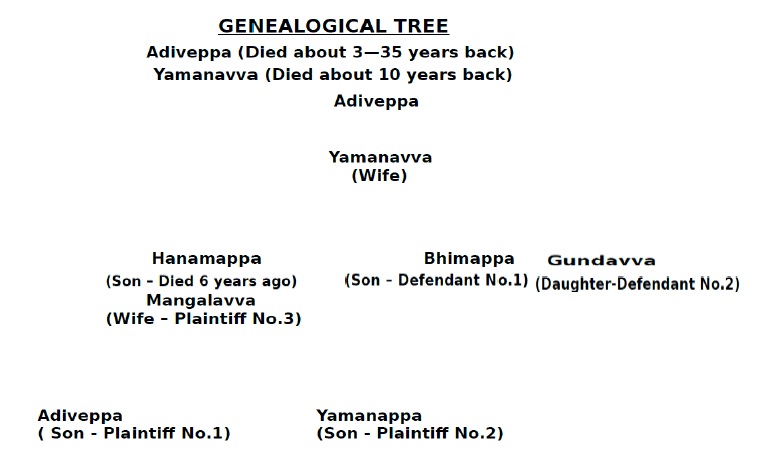

The dispute was between the members of one family, i.e., uncle, aunt and nephews, pertaining to ownership and partition of agricultural lands.

For ease of understanding, the family tree of the parties is as under:

Adiveppa was the head of the family. He married Yamanavva. Out of the wedlock, they had two sons and one daughter, namely, Hanamappa, Bhimappa and Gundavva respectively. Hanamappa had two sons, namely, Adiveppa and Yamanappa. Adiveppa, who was the head of the family, owned several acres of agricultural land. He died intestate.

After the death of Adiveppa and Hanamappa, dispute started between the two sons of Hanamappa i.e. Adiveppa (son – Plaintiff No. 1) and Yamanappa (son – Plaintiff No. 2) and their uncle, Bhimappa and aunt, Gundavva, regarding ownership and extent of the shares held by each of them in the agricultural lands.

Appellants'/ Plaintiffs' contentions

- Adiveppa and Yamanappa (Appellants/ Plaintiffs herein) filed a suit being O. S. No. 85 of 2001 against Bhimappa and Gundavva (Respondents/ Defendants herein) and sought declaration and partition in relation to the suit properties described in Schedules 'B', 'C', and 'D'. The declaration was sought in relation to the suit properties in schedules 'B' and 'C' that these properties be declared as Plaintiffs' self-acquired properties.

- It was alleged that the properties specified in Schedule 'D' were ancestral and hence, the Plaintiffs have 4/9th share in them as members of the family.

- It was alleged that since so far, partition has not taken place by metes and bound amongst the family members, hence the suit also sought for partition.

Respondents'/ Defendants' contentions

- The Respondents/ Defendants denied the Plaintiffs' claim and averred inter alia that the entire suit properties comprising in Schedules 'B', 'C' and 'D' were ancestral properties.

- That during the lifetime of Hanamappa, father of the Plaintiffs, oral partition had taken place amongst the family members on October 28, 1993 in relation to the entire suit properties, pursuant to which all family members were placed in possession of their respective shares. The partition was acted upon by all the family members including the Plaintiffs' father (Hanamappa) without any objection from any member. Hence, the Plaintiffs' claim was misconceived.

Judgement of the Trial Court

After framing the issues and tendering of evidence by the parties, vide judgment/ decree dated July 15, 2006, the Trial Court dismissed the suit on the ground that the Plaintiffs failed to prove the suit properties specified in Schedules 'B' and 'C' to be their self-acquired properties. So far as the properties specified in Schedule 'D' are concerned, though they were ancestral but were

partitioned long back pursuant to which, the Plaintiffs through their father, Hanamappa, got their respective shares along with the other members.

Appeal before the High Court of Karnataka

Aggrieved by the above order, the Plaintiffs filed first appeal before the High Court of Karnataka, whereby the High Court, vide its judgement/ order dated August 22, 2011, dismissed the appeal and affirmed the judgment/ decree of the Trial Court.

Decision of the Hon'ble Supreme Court

- The present appeal is by way of special leave before the Apex Court by the Plaintiffs.

- Upholding the decisions of the courts below, the Hon'ble Supreme Court of India vide its judgement/ order dated September 06, 2017, held that the Plaintiffs in this case could not prove with any documentary evidence that the suit properties described in Schedules 'B' and 'C' were their self-acquired properties and that the partition did not take place in respect of Schedule 'D' properties and it continued to remain ancestral in the hands of family members. On the other hand, the Defendants could prove that the partition took place and was acted upon.

- The Plaintiffs also failed to adduce any other kind of documentary evidence to prove their self-acquisition of the Schedule 'B' and 'C' properties, nor could they prove the source of its acquisition.

- It is a settled principle of Hindu law that there lies a legal presumption that every Hindu family is joint in food, worship and estate and in the absence of any proof of division, such legal presumption continues to operate in the family. The Hon'ble Court opined that a legal presumption that the suit properties comprised in Schedules 'B' and 'C' are part and parcel of the ancestral one (Schedule 'D') could easily be drawn for want of any evidence of such properties being self-acquired properties of the Plaintiffs.

- The counsel for the Appellants/ Plaintiffs had submitted that the Trial Court had recorded some findings against the Respondents/ Defendants in relation to their rights in the suit properties, and the same having been upheld by the High Court, the Appellants are entitled to get the benefit thereof, the Apex Court observed that if the Appellants/ Plaintiffs failed to prove their main case set up in the plaint and thereby failed to discharge the burden, any alternative submission of theirs, which also has no substance, cannot be accepted.

In view of the above, the Supreme Court dismissed the appeal of the Appellants/ Plaintiffs and held that all assets pertaining to a Hindu Undivided Family (HUF) are to be treated as joint property of the HUF, unless the contrary is proved such as self-acquisition of property, through valid documents.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.