E-Governance is application of Information and Communication Technology (ICT) for delivering government services, exchange of information communication transactions, integration various stand-one systems and services between Government-to-Citizens (G2C), Government-to-Business(G2B), Government-to-Government( G2G) as well as back office processes and interactions within the entire government frame-work.1 E-Governance is beneficial to provide a corruption free administrative service to citizens and other stakeholders. The essence of E-governance is to serve intended person easily and faster. There should be an auto-response system to support the essence of E-governance, whereby the Government realizes the efficacy of its governance. Best form of E-governance cuts down on unwanted interference of too many layers while delivering governmental services.

There are many electronic governance projects run by government of India. The target users of all these projects come from different segment of public and have different education standards. When these e-governance projects target grassroots level, its success depend not only designers and developers of such electronic governance projects but much upon cooperation and understanding of its end users. Such project always faces critical evaluation by its users and scholars.

The Ministry of Corporate Affairs (MCA), Government of India, has initiated the MCA21 project, which enables easy and secure access to MCA services in an assisted manner for corporate entities, professionals, and general public. The MCA21 project is designed to fully automate all processes related to enforcement and compliance of the legal requirements under the Companies Act, 1956 Government within a day's time.2 Majority of stake holders of this project are professionals and business houses.

In its help MCA claims, "Adopting international best practices, MCA21 application adds immense value to the stakeholders. The following points highlight the project's invaluable importance:

- Enable the business community to register a company and file statutory documents quickly and easily.

- Public will get easy access to relevant records and get their grievances redressed effectively.

- Professionals will be able to offer efficient services to their client companies.

- Financial institutions will find registration and verification of charges easy.

- MCA will ensure proactive and effective compliance with relevant laws and corporate governance.

- Employees will be enabled to deliver best of breed services." 3

MCA21 has more than 31,000 daily users and about 160 lakhs documents were filed last through this system as on 31st December 2011.4 During the year 2009, E-stamping has been introduced in MCA21 portal. This has enabled the stakeholders to make payment of stamp duty on MCA21 portal itself. The revenue collected by way of stamp duty is remitted to RBI at the end of the week and the RBI remits the same to the respective State.5 XBRL filing for select 30,000 (approx.) companies have been mandated for Financial Year ending 31.03.2011.6

MCA21 has successfully replaced paper based registry system to a virtual registrar office. All information filed here are just few click away for public scrutiny and use. This is an example of success of e governance in India and succeeded to reduce direct public interaction and corruption significantly. This is complete transformation of company law administration in India. With introduction of XBRL, we are practically moving towards next generation electronic governance under company law administration. This will also hopefully gain momentum with passing of new Companies Bill which is presently before honourable parliament. Now, Government has announced to initiate second phase of MCA21 project starting from January 2013.7

We have conducted an online survey from 6th August 2012 to 21st August 2012 on 100 company secretaries of which 84 responses were received. The survey targeted Company Secretaries who are regular users of MCA21 portal. A very simple questionnaire was set for their responses. The survey shows that even though 92% respondents say that their login into system is convenient but they are high on complaints regarding blocking of user id after 3 time entry of wrong password or requirement to enter characters from distorted image. Users opine that instead of blocking of user id, some other verification process may be put into place. One user suggests, "Actually speaking it is highly inconvenient to use login facility. This is evident when one wants to upload any e-form and the session gets expired too quickly and one has to login again. The turnaround time can be increased to 10 more minutes and I guess that would help us access MCA 21 quickly and will also save our considerable amount of time." It is common perception once a month respondents feel problem in login and it completely collapses in peak time like last days of Annual filing.

According to the report of The World Bank and the International Finance Corporation, entitled "Doing Business 2012: Doing business in a very Transparent World", India has been ranked at a low of 132 amongst a sample of 183 countries. Although, there is a seven – point improvement over 2010 ranking of 139. However, India continues to lag behind even the BRIC and SAARC countries on most of the parameters.8 The report rank India on 166 for starting a business involving 12 procedure and 29 day times. The India specific report has a detail relating to establishment a business in India.

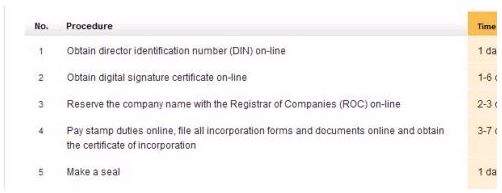

The above screen shoot has been taken from the India profile of the Doing Business for the portion relevant to MCA21 which clearly shows 7 -18 working day time to incorporate a company in India.9 Even though data provided in the report is as on June 1, 2011 but it is not obsolete.

MCA itself guide "To register a company, you need to first apply for a Director Identification Number (DIN) which can be done by filing eForm for acquiring the DIN. You would then need to acquire your Digital Certificate and register the same on the portal. Thereafter, you need to get the company name approved by the Ministry. Once the company name is approved, you can register the company by filing the incorporation form depending on the type of company". 10> There are following steps: Step 1: Application for DIN, Step 2: Acquire/ Register DSC, Step 3: New User Registration, Step 4: Name approval Step 5. Incorporate a Company. It is need less to explain time requirement for incorporation. But one can read, following lines from an unsigned document on the system. "Filing of Incorporation documents in respect of such names shall not be allowed as per below timelines: If name is approved on or before 11.00 AM of any working day then incorporation documents shall not be filed before 7.00 PM of the same working day. If name is approved after 11.00 AM of any working day or at any time on holiday/ non-working day then incorporation documents shall not be filed before 7.00 PM of the next working day. During verification, if the RoC user finds that the approved name ought not to have been allotted, the same shall be liable to be withdrawn by giving an opportunity of being heard to the applicant." 11 All these exercise seems futile when even after name approval through Registrar of Companies; there are instances of registration of companies with undesired name or same name. Practically all name approvals and incorporation are provisional in view of existence of Section 22 of the Companies Act, 1956. Hence there is no need for such a time consuming bureaucratic procedure.

Majority respondents are dissatisfied with the time taken to incorporate a company online. They opine right from filing DIN till the last step should be completed in 24 hours in fully automatic environment. Problem in login, session expire and habit to put sham objections of MCA staff members are frequently quoted problems.

Director Identification Number has been directly linked to Permanent Account Number provided by Income Tax authorities. At the form filing stage itself department verify the PAN details online. Prima –facie there is no need to have a separate DIN when PAN is already there. Further, as per DIN requirement name of applicant should be as per the PAN of applicant. When you go through the PAN Application itself, you can see that there are two entries, namely 'Full name' and 'Name you would like printed on the card'. This create problem for professionals because evident name is display name on the PAN card, this may not be the real name of the applicant. It would be better that in case of Indian Citizens, requirement of DIN numbers should be dispensed with.

In case of annual filing in peak sessions i.e. from September to November every year, dissatisfaction level rises sharply to 48%. Users have long list of complaints including login problems, hanging frequently, showing false errors, frequent server jam, slow uploading, frequent disconnections, break in data transfer, false pre-scrutiny errors etc. One user describes it next to impossible on last date of annual filing. On last days logging into the system itself is not allowed. System throws an error stating that "Too many number of users" or internal system error – contact system administrator". There is nothing to explain if system itself undermine it by claiming "Too many number of users". To add insult to injury, department regularly uploads unsigned letters written in capital letters for the corporate on its website suggesting some preferable dates of filing based on starting alphabet in the name of the company. "To avoid last minute rush and system congestion in mca21due to heavy filing in last 10 days of the months of October and November 2011, it is requested that filing of balance sheet and Annual return may preferably be done in the following order", the letter directed.12 This letter was issued without any legal sanction and its directions prima – facie are against legal mandate given under the Companies Act, 1956. Layman reading of Section 220 read with Section 210 and Section 166, require a company to file annual accounts with in 7 month of end of its financial year and Annual return within 8th month thereof. In majority of cases financial year end on 31st March and relevant last date of filing Annual Accounts comes on 30th October and that of Annual Return on 30th November. It is worthy to note this long period was given in the Act in the manual era. In this information technology era, after computerisation of accounts and online filing, this period may be reduced to 3 and 4 months for all companies so that information may not be obsolete for users. For Listed Companies, SEBI has effectively reduced period to submit to 60 days. Clause 41 (d) of th listing agreement read, "The company shall submit audited financial results for the entire financial year, within sixty days of the end of the financial year."

In case of filing related to charge management, respondents list following major concerns:

- In case of multiple signatories, e – form file size goes beyond the prescribed file size with time and communications. It takes time and consume efforts to maintain this file under limit.

- In manual mode and as per Section 131 of the Companies Act, Registrar of Companies were required to keep two registers one date wise and one company wise. Date wise register is now not available.

- If charge id has already been created and showing on the portal then it is very easy to get modification and satisfaction register but if charge id is not created (being a very old charge) ROC officers will hardly create Charge id without bribe.

- Lack of co – operation from banks and financial institutions.

In case of view of public documents, few concerns of respondents relate to non – availability of old manual documents on the system and Sometime, documents does not open giving one or the other reasons, most of the times blaming Adobe Reader. As discussed earlier sessions expire very frequently and turnaround time is very small period of time. On a public service platform it is quite unfortunate to see this limitation of session. This is an evidence of a failure to provide an e –governance service to a common citizen. It seems the project has been designed for professionals and a common investor have to face session expire many time. The system provides only three hours time to view all documents after viewing first document of the company. Imagine a small investor with aim to view some public documents of a company on MCA portal in small city like Aligarh having a slow speed connection with frequent disconnections, he is in fact denied of his right to inspect document given under the Companies Act itself by prescribing the time limit. This de –facto denial of a public service and access public information become very critical after a recent judgement, where court denied Right to Information under the RTI Act in respect of MCA in the matter of public documents of companies. the Delhi High Court ruled in favour of the Registrar of Companies that denied access under the RTI Act on the ground that the Act was unavailable to applicants when the same right could be exercised through inspection under section 610 of the Companies Act.13

As per the government claim, the MCA21project is designed to fully automate all processes. This suggests visit to Registrar of companies office will be minimised however almost 5% respondent visit Registrar of Companies offices daily. However 67% respondent visits only once a while. Generally, practising professionals visit Registrar office frequently then their peer in employments. Main reason quoted for such visits are improper communication and needless queries from the department. One view is that people at registrar still spent their time to find out some way for seeking bribe. To term an e – governance project successful, any physical visit to the office of a public service authority must be a rare event.

Majority of respondents claim that it takes up to one hour and more in normal season and up to two hours or more, from downloading a new form to filing of complete form for annual filing in to the MCA21 System. However, for all other e-forms majority of respondents take up to half an hour (not applicable to e-forms relating to charge filing).

For success of any e – governance project, support and active participation of its users is imperative. MCA21 project is one rare project where a majority of users are professionally qualified or at least educated. It is highly unfortunate to see that many companies do not register their documents as per legal required and a good numbers of them follow letters of law not the spirit of law. Time and Quality of information provided by all users is also matter of concern.

MCA 21 in an attempt to persuade timely compliances has displayed on its portal, list of dormant companies, defaulter companies, defaulting directors and defaulting secretaries. As on 23rd August 2012, there are total 22,226 entries relating to directors and their companies under dormant status. On even date, the list of defaulter companies running into 901 pages evidencing about 63,000 entries. Separate List of Directors and Secretaries of these companies also available on the website of MCA21.

Relatively SEBI has much wider reach and popularity amongst large population of small and mid size investors due to its strong teethes and investor protection capabilities. With increasing investor activism and sophistication of market regulator and stock exchanges, more and more information related to listed companies, which may otherwise available on MCA21, is being hosted simultaneously on web portals of company as well as CorpFiling www.corpfiling.co.in is the common filing and dissemination portal for all companies listed on the BSE & the NSE. www.corpfiling.co.in has been developed and is being maintained by IRIS Business Services (India) Pvt. Ltd. Participating Exchanges of www.corpfiling.co.in portal; provide data of all corporate disclosures of companies subjective to their listing in the particular exchange. Here, a stakeholder can find Financial Results, Corporate Announcement, Share holding patterns, Disclosure under SEBI regulations and Insider trading.14> Both major stock exchanges participates for this platform. All information here is free of cost and easy to access then relevant information available on MCA21. Many users are using this information for their daily uses rather than that of original centralised registry of MCA21. This parallel system effectively reduced MCA21 to a corporate information system for mid and small segment.

Even though majority of respondents to survey find MCA21 site user friendly but a good percentage have some concerns. Some of these are:

- To register digital signature of a director or practising professional on MCA21 system is one of the extremely difficult exercise.

- In case of any possibility of disturbance due to updating or maintaining, it should be notified well in advance.

- Checking Name availability required more simplification.

- Users may be educated with videos of practical demo in addition of mere theories. It will be helpful for new users.

- Full automation of MCA21 is need of hour; steps should be taken for minimisation of physical visits.

The survey about the system clearly reveals that on user satisfaction front, MCA21 project could be more efficient and successful if the technological and procedural hurdles are removed. In times of globalisation and dynasism we need transparent and effective e-governance systems. There is immense scope of improvement relating to procedural aspect and the same is an opportunity to look into what still needs to be achieved This e governance project has not been successful to achieve following aims as declared by the government:

- To register a company and file statutory documents quickly and easily.

- To ensure proactive and effective compliance with relevant laws and corporate governance

- To provide easy access to relevant records and get their grievances redressed effectively.

There is no conclusive step from Ministry of Corporate affairs to improve its working in last two years since the introduction of online payment of stamp duty. The Ministry not only failed to replace present obsolete Companies Act, 1956 in last two decade but also providing all possible relief to its users and stakeholders. There is no attempt from the ministry to do any grass root survey of its users with intention to improve its working. Fortunately, after the recent World Banking report the Ministry of Corporate affairs constituted a 20 members Committee for Reforming the Regulatory Environment for doing Business in India. It is better to quote the wording of the circulars to conclude:

"Easing of business environment mandates extensive examination of regulations in different areas of root functioning such as financial reforms, governance reforms, liberalized policy framework, process reforms, etc. Thus there is a need to conduct an in-depth study into the entire gamut of regulatory framework and come out with a detailed roadmap for improving the climate of business in India in a time bound manner. Such an exercise needs to be undertaken for periodical improvement in the ranking, leading to a situation where India gradually moves towards upward position with almost zero hassles."15

Footnotes

1. Saugata,B., and Masud,R,R.(2007. Implementing E-Governance Using OECD Model(Modified) and Gartner Model (Modified) Upon Agriculture of Bangladesh. IEEE. 1-4244-1551-9/07.

2. http://mit.gov.in/content/mca21

3. http://www.mca.gov.in/MCA21/dca/WebHelp/MCA_Help.htm

4. Page 6 of Annual Report 2011 02012 of Government of India ministry of Corporate Affairs

5. Page 69 ibid

6. Page 69 ibid

7. http://pib.nic.in/newsite/PrintRelease.aspx?relid=87946

8. http://www.mca.gov.in/Ministry/pdf/General_Circular_26_2012.pdf

9. http://www.doingbusiness.org/data/exploreeconomies/india

10. http://www.mca.gov.in/MCA21/RegisterNewComp.html

11. http://www.mca.gov.in/Ministry/pdf/Name_availability.pdf

12. http://www.mca.gov.in/Ministry/pdf/Pro_Statutory_Returns_2011.pdf

13. Registrar of Companies v. Dharmendra Kumar. http://lobis.nic.in/dhc/VS/judgement/06-06-2012/VS01062012CW112712009.pdf

15. http://www.mca.gov.in/Ministry/pdf/General_Circular_26_2012.pdf

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.