- within Strategy and Immigration topic(s)

The year 2006 saw a record level of private equity deals in Asia. Up to the end of November 2006, the transaction total in the Asian private equity industry amounted to US $43.7 billion. This represents an increase of 148% from 2005 when the transaction total for the whole year was US $17.6 billion.

Many private equity deals are structured using offshore vehicles, in particular, British Virgin Islands ("BVI") and Cayman Islands vehicles. The BVI was the country with the second largest sum of direct investment in the People’s Republic of China ("PRC") in 2006 with investments totalling US $11.25 billion, representing an increase of 25% from 2005. Cayman ranked eighth largest in terms of direct investment in the PRC in 2006 with investments totalling US $2.1 billion, representing an increase of 8% from 2005. In fact, the aggregate direct investment in the PRC from the BVI and Cayman accounted for more than 25% of the PRC’s total foreign direct investment inflow in 2006.

In recent years, PRC companies have increasingly turned to private equity as a means to finance their businesses and foreign investors usually prefer to invest in businesses in the PRC through various offshore structures, in particular offshore holding companies.

Offshore holding companies are popular with foreign investors for many reasons. There is great flexibility in structuring the company so as to allow for different rights and returns (e.g. by having different classes of shares). The use of these offshore holding companies assists with listings on international stock exchanges. Bermuda and Cayman have been two of the most popular offshore jurisdictions for these offshore holding companies, mainly due to the acceptance of these jurisdictions by various stock exchanges such as NASDAQ, Singapore, Hong Kong and London. Over the past year or so, the London Alternative Investment Market is being increasingly favoured as a stock exchange. Asian sourced clients/ private equity houses seeking an exit option frequently use BVI and Jersey companies.

Many offshore jurisdictions are common law jurisdictions (e.g. Bermuda, Cayman and BVI) and generally offer corporate governance features that are more familiar to international private equity firms. Mauritius is also popular because of its double-taxation treaty network- it is well utilised for PRC, Indian, African and Middle Eastern deals.

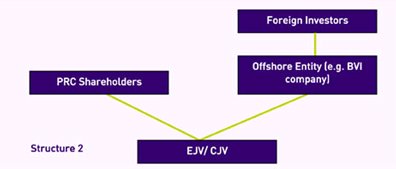

Set out below are two typical structures using offshore holding companies in a private equity transaction in the PRC:

In the first structure, institutional private equity investors and PRC shareholders often subscribe for new shares in a BVI or Cayman offshore holding company that, in turn, holds interests in a PRC wholly foreign-owned enterprise ("WFOE") or other assets/ investments in the PRC. A WFOE is usually established in the form of a limited liability company. A WFOE with limited liability has its own registered capital, is a separate legal identity distinct from its foreign investors and is an independent legal person capable of contracting and bearing liability on its own behalf. Convertible bonds or notes that are convertible into shares of the offshore holding company may also be issued to assist with the financing of the acquisition or set up of this structure.

In the second structure, the investments from foreign investors are streamed into a PRC equity joint venture ("EJV") or co-operative joint venture ("CJV") via a BVI or Cayman offshore holding company that, in turn, holds interests in the EJV or CJV.

An EJV is a limited liability company and it has a legal identity distinct from the investors. CJVs can be formed as either a CJV with a separate legal identity or a CJV with no separate legal identity from its investors.

The main difference between an EJV and a CJV is that the risks, losses and profits of the EJV are shared between the parties in proportion to their respective contributions to the registered capital of the EJV while the risks, losses and profits of the CJV are shared between the parties in accordance with any agreement or arrangement that they may have irrespective of the proportion of the parties’ contributions to the registered capital of the CJV.

A WFOE has certain advantages over an EJV/ CJV. For example, setting up a WFOE is usually easier and faster compared with setting up an EJV/ CJV because the set up of an EJV/CJV usually involves extensive and protracted negotiations between the parties on the joint venture contract.

One of the main disadvantages with WFOE is that investors who are new to PRC often find it extremely difficult to start without the assistance of a PRC partner. This is because knowledge of local markets and conditions is important and, particularly, good local contacts or relationships with local governmental authorities are often essential to the establishment of a foreign investment entity.

We have seen an increasing number of these foreign investment structures set up in the PRC utilising offshore vehicles and expect the private equity trend to continue in 2007.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.