Keywords: real estate, transfer tax, RETT-Blocker, landlord, tenant, written form cure clauses, leases, property management company, land charges,

TIGHTENING OF THE RULES FOR STRUCTURES AIMED AT AVOIDING GERMAN REAL ESTATE TRANSFER TAX – RETT-BLOCKER"

By the Law Implementing the Administrative Cooperation Directive and to Change Tax Provisions (Administrative Cooperation Directive Implementation Act – AmtshilfeRLUmsG") inter alia, the rules regarding real estate transfer tax law have been tightened. This AmtshilfeRLUmsG now finally also includes the long-planned legal change to the real estate transfer tax law in order to prevent so-called RETT-Blocker" structures. In return to this tightening of the law, the possibilities for real estate transfer tax neutral intra-group restructurings pursuant to Section 6a GrEStG were extended. The real estate transfer tax rules apply to all acquisitions realized from June 7, 2013.

Old" RETT-Blocker Structure

Under the old legal situation, only the direct change of the legal owner of domestic real properties (Section 1 paragraph 1 and 2 GrEStG) and the transfer of interest in partnerships and corporations holding real properties (Section 1 paragraph 2a and 3 GrEStG) constituted an event, which is generally subject to real estate transfer tax.

For cases where interests in partnerships and corporations are combined in accordance with Section 1 paragraph 2a and 3 GrEStG, the evaluation under the old rule was exclusively based on civil law, where the joint right of the (direct or indirect) shareholders/ partners to the company's assets was decisive. The evaluation had so far not been based on an economic perspective.

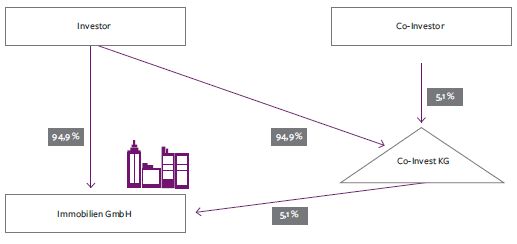

Under these rules, the following structure was regularly implemented in order to avoid real estate transfer tax from accruing in the case of a (partial) change of shareholders/partners (so-called RETT-Blocker" structure). In the case of such a RETT-Blocker structure, an Investor acquired up to 94.9 percent of the shares in a corporation holding the domestic real estate (Immobilien GmbH). The remaining shares were held by a partnership (Co-Invest KG). In the partnership, the Investor again held up to 94.9 percent and a (third-party and independent from the Investor) Co-Investor held the remaining interests of 5.1 percent.

In this (simplified) basic structure, no real estate transfer tax accrued under the old legal situation. Because first of all, no direct change of the legal owner of a domestic real estate exists pursuant to Section 1 paragraph 1 GrEStG, because from a civil law perspective, the acquisition of shares in the company holding the real estate cannot be equated to the acquisition of civil law ownership of the real estate. Also, only the Immobilien GmbH itself is entitled to realize the real estate and accordingly no taxable event pursuant to Section 1 paragraph 2 GrEStG exists either.

Finally, the event is not taxable pursuant to Section 1 paragraph 3 GrEStG, since the Investor does not acquire at least 95 percent of the shares in the Immobilien GmbH. Under the old legal situation, the 5.1 percent participation in the Co-Invest KG (94.9 percent of 5.1 percent) was not attributed to the Investor either. Because the real estate could only be attributed to the member of the interposed partnership, if all shares in a partnership are to be attributed to a member. Any economic perspective beyond this was ruled out.

New Rule of Economic Combination of Shares

In order to combat the described RETT-Blocker structures, a new subsidiary rule for cases of share combinations is inserted under Section 1 paragraph 3a GrEStG. Thereby, an economic participation" was introduced into real estate transfer tax law.

The new rule creates a fictitious combination of shares or interests in the sense of Section 1 paragraph 3 GrEStG, if an economic participation of at least 95 percent is held directly or indirectly in the company holding the domestic real estate.

Taking into account this new rule, the implementation of the previously customary RETT-Blocker structure is subject to real estate transfer tax, since, as described, Section 1 paragraph 3a GrEStG is not based on the civil law perspective, but applies the accrued amount of the indirect and direct participation. Accordingly, the amounts of the interests in the capital or the assets of the respective companies have to be multiplied pursuant to Section 1 paragraph 3a sentence 3 GrEStG in order to determine the indirect participation. The Investor, who holds 94.9 percent in Immobilien GmbH directly and 4.84 percent (94.9 percent of 5.1 percent) indirectly via Co-Invest KG, thus holds 99.74 percent (economically), i.e. at least 95 percent of the shares in Immobilien GmbH.

Criticism and Outlook

The new rule has a very wide scope of application. Constellations and structures might also be included now, which were not meant to serve the avoidance of real estate transfer tax and were specifically excluded from the scope of the real estate transfer tax law before.

In addition, the terminology of the provision itself is partially unclear. It is accordingly particularly questionable, whether the term of economic participation also includes rights that are similar to participations or other obligatory elements. Generally, it should be possible to assume that Section 1 paragraph 3a sentence 2 and 3 GrEStG define the term of economic participation with participation in the capital or assets of the company" conclusively and that the aforementioned similar rights are not included.

It would at least be desirable, if a statement or clarification from the tax authorities concerning the unclear issues would be published soon. This applies in particular in respect to the fact that the individual federal states currently pursue an increase of the respective real estate transfer tax rates. Thus, inves-tors have an increased interest in legal clarity in order to either choose structuring alternatives or take corresponding expenses for real estate transfer tax into account in their investments.

WRITTEN FORM WITH NO END IN SIGHT

OLG Hamm, decision of April 26, 2013 – I-30 U 82/12

Head Note

- Written form cure clauses in lease agreements will be effective, even if they are agreed as General Terms and Conditions.

- The acquirer of a leased object is not obligated under such a written form clause to subsequently contract in the proper form because of written form defects originating from the period between prior owner and tenant.

- The rights under a written form cure clause pass to the acquirer based on an implicit assignment of these rights.

Facts

The defendant tenant entered into a lease agreement with the former owner of a real property for a hotel building under construction. Subsequently, these parties concluded two supplements to the lease agreement. The object was sold to the plaintiff later on. The tenant then terminated the lease by invoking a defect of the written form whereupon the acquirer filed an action for a declaratory judgment with the goal of determining that the lease continued to exist and had not been terminated prematurely. The Higher State Court (OLG) decided in favor of the plaintiff.

Content and Subject of the Decision

One of the most disputed subject matters in commercial tenancy law is the so-called written form requirement for lease agreements. This particularity of German tenancy law, which particularly causes incomprehension among foreign investors again and again, has important economic effects at the same time. In our spring 2013 Newsletter, we reported about a different high-court decision and explained the problem in detail. Essentially, the issue is that lease agreements with a term of more than one year require the written form (Section 550 sentence 1 BGB). If the essential understandings between the parties are not recorded within a written instrument, the contract will be deemed concluded for an unspecified period of time and may be terminated upon the statutory notice period (Section 550 sentence 2 BGB). So-called written form cure clauses", also referred to as remedial clauses", are aimed at avoiding this risk. Accordingly, the parties are supposedly no longer able to invoke any violations of the written form, but are rather required to establish the written form subsequently. So far, there is no high-court decision by the German Federal Court of Justice (BGH) on the validity of such written form cure clauses. The decision by the OLG Hamm sets a clear signal here. It states that such clauses are effective even in case – as usual – they were agreed as general terms and conditions of contract. According to the view of the court, the clause was neither surprising nor unreasonably discriminating against the participants, which could lead to an ineffectiveness of the clause because of a violation of Section 305c or, as the case may be, Section 307 para-graph 2 no. 1 BGB. Such clauses were not unusual in the commercial field, which is why they were to be expected. They were not unreasonable either because of a circumvention of the mandatory character of the written form rules. The Senate refers to the established case law of the German Federal Court of Justice, according to which the parties to an orally concluded lease agreement can agree to conclude it in writing later on. Therefore, it is also supposed to be possible to agree on a claim for the conclusion of a formally-effective lease agreement. The fact that the right to terminate pursuant to Section 550 BGB is ruled out by such clauses is considered unproblematic by the Senate, since this constitutes a consequence of the general objection of bad faith pursuant to Section 242 BGB. Finally, the clause was not unreasonable in relation to the acquirer either, since the latter could not be obligated based on it to conclude an agreement, which was not initiated by him, in a formally effective way.

Another part of the deliberations is centered around the question of whether or not an acquirer may assert the claims based on the valid remediation clause. Even though an acquirer enters into an existing lease agreement pursuant to Section 566 BGB by action of law, this does not apply to duties existing prior to the acquisition and is at least doubtful regarding the corresponding rights based on the written form clause. The court states in this regard that at least in the present case, an implicit assignment of the claims resulting from the written form clause to the acquirer had to be assumed. Therefore, the acquirer was able to assert the claims based on the remediation clause against the tenant.

Impact on Day-to-Day Business

The decision of the OLG Hamm is to be welcomed, because it deals extensively with the question of effectiveness of remediation clauses and affirms these with substantial arguments. The decision addresses new aspects in this context, to which hardly any attention had been paid in the discussion so far. The clear recognition that such clauses are customary on the market and of the economic reason for the wide adaptation cannot be valued highly enough. It remains to be hoped that the German Federal Court of Justice (BGH) will support this position. The decision appears contestable primarily in respect to the statements regarding the implicit assignment of the claims from remediation clauses to an acquirer. Doubts as to whether this legal assessment will stand up to a high-court review are certainly appropriate here. In practice, an explicit assignment of claims based on such remediation clauses should therefore be included in the purchase agreement in the interest of the acquirer for now. This avoids the risk that a different court does not follow the argument of an implicit assignment of the claims.

TRANSFER OF THE EMPLOYMENT RELATIONSHIP OF THE PROPERTY MANAGER WHEN A REAL PROPERTY IS ACQUIRED

BAG, decision of November 15, 2012 – 8AZR 683/11

Head Note

Real property managed by a property management company is not an operating resource of that company. Rather, it is the object of management activity. The employment relationships of the employees of the property management company managing the real property therefore do not pass to the acquirer of the managed real property by way of transfer of operations.

Facts

The parties are in dispute as to whether the employment relationship of the plaintiff has passed to the defendant city by way of a transfer of operations. The plaintiff worked at A GmbH & Co. KG as a technical-commercial employee in the building management and was as such exclusively responsible for the management of an office and commercial building in M. The duties of the plaintiff included the lease administration, supervising the maintenance of the object, as well as representing the interests vis-à-vis the construction management, public authorities, and third parties.

The defendant was the principal lessee of the building leasing 82 percent of the existing area.

After the sale of the office and commercial building, being the only asset of the KG, to the city, the KG was liquidated. The defendant continued the existing lease agreements and utility contracts concerning the building. The management of the property was taken over by the defendant's municipal building management. The plaintiff now seeks the determination that his employment relationship continues to exist and has passed to the defendant. So far, he was successful in all prior instances.

Content and Subject of the Decision

Upon the defendant's appeal, the Federal Labor Court (BAG) annulled the decision of the state labor court (LAG) and dismissed the lawsuit. The employment relationship of the plaintiff did not pass from A GmbH & Co. KG to the defendant by way of a transfer of operations pursuant to Section 613 a paragraph 1 sentence 1 BGB.

For purposes of defining a transfer of operations, the BAG applies its established case law and assumes such a transfer, if a new legal entity continues the economic unit while preserving its identity. Even though an independent economic unit existed in the present case in the form of the property management originally carried out by the KG, which was capable of being transferred, the working purpose of that unit was aimed at maintaining a leased building used by third parties in an appropriate condition, preserving its substance, and ensuring income from leasing it. This operation was, however, not transferred to the defendant. The management of the office and commercial building constitutes an operation with only few operating resources, the added-value of which focuses not on the sold real property, but rather on the operating resources required for the commercial activity. These resources are, e.g.: office, IT equipment, and the tools required for the technical management. The sold real property is merely the object of the property management so that its disposal has no relevant influence on the transfer of the economic unit.

It is insofar also harmless that the property management of the KG was limited to a single real property, because the activity of the property management constitutes a service that focuses on the manpower, where an employee can also perform that activity for other real properties. With the acquisition of the real property, however, the defendant did not take over any employees.

The fact that specifically speaks against the existence of a transfer of operations is that the operating purpose of the commercial property management was not maintained by the defendant. While A GmbH & Co. KG focused on generating profits through the property management, this aspect is absent entirely in the case of the management of real property used by the owner itself.

Insofar, it is also interesting to see how the BAG deals with the Klarenberg" decision of the ECJ dated February 12, 2009 – C-466/07. In this decision, the ECJ made it clear that a transfer of operations may also be assumed in accordance with Council Directive 2001/23/EC dated March 12, 2001, if the organization of the economic unit is not maintained, but if only the functional relationship of the transferred production factors permit the acquirer to continue using them for an equivalent activity after integrating them into a new structure. The BAG interpreted this decision as meaning that the actual continuation of the business activity and not only a possibility to do so constitutes the decisive criterion for the transfer of operations and thereby followed its own established case law as well as the ECJ decision dated November 20, 2003 – C-340/01.

Impact on Day-to-Day Business

The decision finally provides some degree of legal certainty that labor law consequences will no longer have to be expected in the case of a sale of a previously self-managed real property for self-use. A financial aspect also plays a significant role here due as the acquirer of such real property is not faced with any further costs resulting from the employment relationship of the property manager.

In this decision, the BAG follows its own previous case law regarding transfers of operations in the case of managed objects". A similar substantiation approach could already be found in the decisions about the technical plant management by a facility management company and the supervision of military training grounds by third-party providers. In the former case, the BAG rejected the transfer of operating facilities to the acquirer, since the technical facilities (heating, sanitary, and air conditioning systems) were merely the objects through which the business purpose of technical facility management and administration was performed. In the second case, the operating resources (inter alia, the guard building, the telephone and alarm system) had only a subordinated and thus not an identity-characterizing role in connection with guarding the military training ground.

As a consequence, these objects do not constitute the actual core of the functional relationship required for the added value in terms of an evaluation so that as in the present case, no transfer of the economic unit to the acquirer occurred through their sale.

ON THE LIABILITY OF THE FIRST-RANKING LAND CHARGE CREDITOR FOR DAMAGES IN THE CASE OF A TRANSFER OF THE LAND CHARGE TO THIRD PARTIES

BGH, decision of 19 April 2013 – V ZR 47/12

Where loans are secured using land charges, the latter are often passed on to third-party banks, e.g. in a debt restructuring. It is also customary practice where subordinate land charges are established to regularly assign the retransfer claims of the owner against the senior real property lien creditor. If the latter is disclosed to the senior creditor, the senior creditor may become liable for damages by transferring the first-ranking land charge to a third party.

Head Note

A secured party is liable for damages according to the general law of obligations, if it culpably fails to fulfill the claim for retransfer, which is subject to the condition precedent of definite lapse of the security purpose.

Facts

The defendant bank held first-ranking land charges. The suing savings bank holds lower-ranking land charges encumbering the same real properties. Under the security purpose agreement, the owner had assigned future and contingent claims for retransfer, inter alia, of all higher-ranking land charges to the plaintiff. The plaintiff disclosed this assignment to the defending bank. Subsequently, the defendant transferred the land charges to a third bank for an amount of EUR 150,000 that was equivalent to the outstanding loan amount. The latter extended a new loan under the land charges and issued the deletion consent at the time of the sale of the real properties against payment of a redemption amount of EUR 450,000. The plaintiff demands damages in an amount of EUR 300,000, since the defendant would insofar have had to retransfer the land charges, but culpably failed to do so.

Content and Subject of the Decision

The decision focuses on the security purpose agreement between the owner and the first-ranking land charge creditor as cardinal point. The court first addresses the question of when the claim for retransfer arises. The claim for retransfer embodies the right of the security grantor to request the retransfer of a collateral once the cause for granting the security is no more. The claim is always subject to the condition precedent to definite lapse of the security purpose, i.e. the agreed legal link between the collateral (e.g. the land charge) and the obligations to be secured (e.g. claim for repayment of a loan). The security purpose lapses upon complete and definite performance of the secured obligations. A difference needs to be made whether the security purpose is narrow, i.e. whether the security is provided only for a very specific obligation, or whether it is wide, e.g. all – including future – obligations from a business relationship are secured. When the condition precedent is fulfilled is not as clear in the case of an agreed wide security purpose as it is in the case of an agreed narrow security purpose. In most cases, an agreed wide security purpose also provides for a new extension of the loan under the land charge, whereby the fulfillment of the condition may be postponed repeatedly each time a new loan is granted or the existing one is extended. In particular, newly arising payment obligations prevent the fulfillment of the condition precedent in spite of the repayment of the previous payment obligations. Therefore, the condition is fulfilled according to the German Federal Court of Justice (BGH) in any case once the business relationship ends. This is at the latest the point in time when it is certain that no new extension of a loan may occur between the parties of the security purpose agreement. In the present case, the business relationship between the owner and the defending bank had ended when the latter assigned the land charge for debt restructuring purposes against payment of the remaining outstanding amount secured by the land charge. Therefore, the BGH found that the security purpose lapsed at the time of the assignment.

In the following, the BGH affirmatively answers the question of whether the retransfer claim may also arise only partially. In the absence of specific rules under the security purpose agreement, the land charge is also to be retransferred in parts. This is substantiated using the existing BGH case law regarding excess collateralization, which, when it occurs definitively, results in the lapse of the security purpose insofar. This had affected the part of the land charges, which no longer served to secure any loan, at the time of the assignment to the third-party bank.

Finally, the BGH details the statutory rule according to which a new creditor of the retransfer claim (in the present case, the bank with the lower-ranking land charge) has to accept all legal acts of the debtor (in the present case, the bank with the first-ranking land charge), which – although made without his involvement - postpone or frustrate the fulfillment of the condition, for as long as the debtor did not have any knowledge of the change of creditors. In the present case, however, the assignment had been disclosed to the defending bank. In this case, the security purpose agreement could only be changed with the consent of the new creditor. The BGH affirms that this consent requirement does not apply to new extensions of loans under the land charge that are already permitted under the security purpose. Likewise, the lapse of the retransfer claim cannot be prevented in the case of a direct sale of the land charge by the new creditor after the secured event has occurred. These disadvantages were part of the retransfer claim. Even in case the retransfer claim was formally assigned in its entirety, this would not prevent the new creditor from asserting the retransfer claim that had arisen only partially.

Impact on Day-to-Day Business

This court decision is not surprising, as it consistently implements the general principles of the law of obligation in the German Civil Code (BGB). In practice, this decision affects primarily the assignment of security in connection with debt restructurings with third parties. In the case of definite sales of loans with collateral, i.e. the replacement of the debtor of the retransfer claim, the case law should play hardly any role at all. This is because the debt as such remains unchanged and the retransfer claim itself remains unaffected. The BGH had already decided accordingly in 1991 for the replacement of the original creditor, i.e. of the real property owner as provider of collateral, and confirmed this again in this decision. Also, the case law expressly does not apply in the case of realizations after occurrence of the secured event by direct sale of the land charge.

Even though the BGH considers the contractual agreement in the security purpose agreement relevant in respect to the duty of also partial retransfer; in practice, however, a partial retransfer will regularly also be owed. The reason for this is the duty to release collateral in the case of a subsequent excess collateralization, i.e. the value of the collateral substantially exceeding the secured obligations. If this excess collateralization is final (i.e. no new liabilities by the security grantor can be incurred which would be secured by the land charge), it would be unreasonable for the provider of collateral to allow the full land charge to continue to exist for a significantly lower amount still owed. According to the prevailing opinion, the definite excess collateralization therefore leads to a partial retransfer claim. The BGH apparently did not intend to change this with its decision.

If junior-ranking land charges exist and if the first-ranking real property lien creditor has knowledge of the assignment of the retransfer claim to the subordinated creditor, the security purpose agreement will have to be reviewed. In cases of doubt, the sub-ordinated creditor has to be asked for approval during the transfer of the first-ranking land charge. If that approval is withheld, the land charge will have to be partially deleted. The remainder can only be transferred in the amount of the remaining outstanding loan.

For junior-ranking land charge creditors, who receive assignments of retransfer claims, it is advisable at any rate to have the owner disclose the assignment to the first-ranking creditor or, as the case may be, obtain an original deed of the assignment agreement in order to be able to effect the disclosure themselves.

Originally published July 18, 2013

To learn more about our Real Estate practice.

Mayer Brown is a global legal services provider comprising legal practices that are separate entities (the "Mayer Brown Practices"). The Mayer Brown Practices are: Mayer Brown LLP and Mayer Brown Europe – Brussels LLP, both limited liability partnerships established in Illinois USA; Mayer Brown International LLP, a limited liability partnership incorporated in England and Wales (authorized and regulated by the Solicitors Regulation Authority and registered in England and Wales number OC 303359); Mayer Brown, a SELAS established in France; Mayer Brown JSM, a Hong Kong partnership and its associated entities in Asia; and Tauil & Chequer Advogados, a Brazilian law partnership with which Mayer Brown is associated. "Mayer Brown" and the Mayer Brown logo are the trademarks of the Mayer Brown Practices in their respective jurisdictions.

© Copyright 2013. The Mayer Brown Practices. All rights reserved.

This Mayer Brown article provides information and comments on legal issues and developments of interest. The foregoing is not a comprehensive treatment of the subject matter covered and is not intended to provide legal advice. Readers should seek specific legal advice before taking any action with respect to the matters discussed herein.