- within Cannabis & Hemp and Environment topic(s)

- with Senior Company Executives, HR and Finance and Tax Executives

- with readers working within the Accounting & Consultancy, Insurance and Healthcare industries

INTRODUCTION

Canada, often referred to as "Hollywood North," continues as a leading innovator in the development and implementation of public sector incentives for film and television production. These incentives have stimulated a billion dollar industry in Canada for the production of both domestic or indigenous programming content and foreign based Canadian location or service productions.

Currently, these public sector initiatives comprise:

- Direct Federal and provincial assistance in the form of grants, loans and equity investments in Canadian content programming;

- Federal and provincial refundable tax credit programs available to domestic producers of Canadian content programming;

- Federal and provincial refundable tax credit programs available to domestic and foreign producers of non-Canadian content programming that employ Canadians and choose Canada as a location or service centre; and

- Canadian content program recognition designation for both qualifying Canadian domestic productions and foreign co-ventures.

In this monograph, we focus on the last two groups of these initiatives and in particular, their application to US-based film and television productions.

FEDERAL REFUNDABLE TAX CREDIT PROGRAM FOR SERVICE PRODUCTIONS

The Federal Tax Credit Program

Under the administration of the Canadian Audio-Visual Certification Office ("CAVCO") and the Canada Revenue Agency ("CRA"), the Canadian Federal government assists domestic and foreign producers by offering two types of refundable tax credits:

- The Canadian Film or Video Production Tax Credit

("CPTC")

A refundable tax credit available to Canadian domestic producers for qualified labour expenditures paid for services rendered in connection with the production of eligible Canadian content film and television productions. The CPTC program is intended to encourage indigenous Canadian programming and to strengthen the domestic production sector. The CPTC is calculated at a rate of 25% of actual qualified labour expenditures capped at 60% of total production costs. To the domestic producer of Canadian content programming, the CPTC represents a budgetary contribution of approximately 15% of the total cost of production (i.e., 25% of 60%), net of assistance. - The Film or Video Production Services Tax Credit

("PSTC")

A refundable tax credit available to both Canadian producers and foreign producers with a permanent establishment (i.e., a production office) in Canada, for qualified Canadian labour expenditures paid for services rendered in connection with the production of qualifying non-Canadian content film and television productions. The PSTC program was designed to strengthen Canada's international reputation as a location of choice for film and video productions employing the services of Canadians. This refundable tax credit is based upon "qualified Canadian labour expenditures" incurred by an "eligible production corporation" for services provided in Canada by Canadian residents or taxable Canadian corporations for the production of an "accredited production." As a fully refundable tax credit, an eligible production corporation is entitled to a refund of the PSTC where the corporation has no federal income tax payable in a particular taxation year or where the credit is more than the amount owed in federal income tax.

How Much Does The PSTC Represent?

The PSTC is calculated at a rate of 16% of qualified Canadian labour expenditures. There is no cap on the amount of credit that can be received and the credit is completely refundable. The PSTC is not available where the production has received a tax credit under the CPTC.

Who Is Eligible To Claim The PSTC?

Canadian domestic corporate producers and foreign-owned corporations having a permanent establishment (a production office) in Canada are eligible to claim the PSTC. The corporation's primary activity must be in relation to a film or video production business or a film or video production services business. The applicant corporation must either own the copyright in the film during the production period or be engaged directly by the copyright holder to provide production services.

Minimum Expenditure Requirements To Qualify For The PSTC

To qualify for the PSTC, a film or television production must meet the following minimum expenditure requirements:

- $1,000,000 Cdn. for a feature film;

- $200,000 Cdn. for a one-hour television episode; or

- $100,000 Cdn. for a 30-minute television episode.

Eligible Genres Of Production

The following genres of production do not qualify for PSTC benefits:

- News, current event or public affairs programming, or a programme that includes weather or market reports

- Talk and game shows

- Sporting and award events

- Reality television

- Productions that solicit funds

- Pornography

- Advertising

- Industrial, institutional or corporate productions

- A gala presentation or an awards show

What Labour Expenditures Qualify For The PSTC?

Qualifying Canadian labour expenditures consist of the following for the stages of production from the final script stage to the end of post-production, paid in the year or within 60 days after the year end:

- Salaries and wages:

-

- Paid to persons who were resident in Canada at the time the payments were made

- Paid for services provided in Canada

- Remuneration paid to:

-

- Non-employee(s) of the producer who are Canadian residents

- Taxable Canadian corporations for the services of their employee(s) who are Canadian residents

- Loan-out corporations or personal services corporations for the services of a Canadian resident, subject to certain restrictions

- Partnerships for the services of a partner who is a Canadian resident

- Reimbursements by a wholly-owned production company to its parent company for qualifying labour expenditures that were paid by the parent company on behalf of the production company

A producer's labour expenditure for the purposes of the CPTC must be reasonable in the circumstances and directly attributable to the production.

Can The PSTC Be Combined With Other Tax Credits?

While the PSTC can be claimed in conjunction with complimentary provincial tax credit programs, it cannot be combined with a claim for the federal refundable CPTC available to qualifying domestic Canadian content production.

COMPLEMENTARY PROVINCIAL TAX CREDIT PROGRAMS

In many provinces, provincial tax credits and incentive programs provide an additional source of funding for qualifying film and television productions. In a number of provinces, these provincial incentives are boosted by incentive credits and bonuses for regional production and training initiatives. In most cases, provincial tax credits can be combined with federal tax credits to augment the total benefits available to domestic and foreign productions produced in Canada. As is the case with Federal film tax credit programs, Provincial film tax credits are refundable to the extent the credit exceeds the producer's Canadian income tax payable.

Moreover, recognizing the importance of stimulating the domestic employment market for skilled animation, special effects and digital media workers, provincial governments in Ontario, British Columbia and Québec have legislated refundable tax credits for eligible computer animation and special effects activities, as well as interactive digital media products.

Assistance provided at the provincial level changes from time to time due to industry pressure on government to remain competitive with foreign tax credit programs. As well, competitive pressures between provinces result in some degree of jockeying at a provincial level. As one province enhances its film and television program, the remaining provinces are pressured to boost their support of film and television industries.

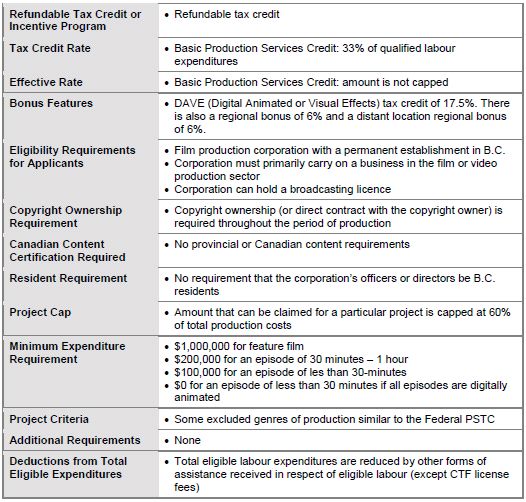

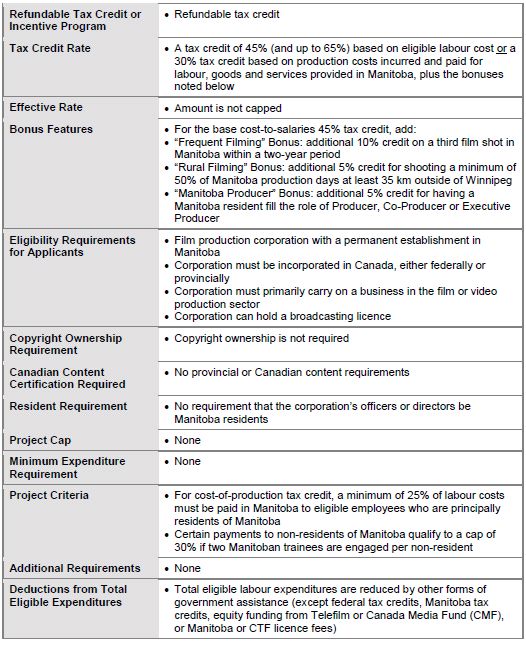

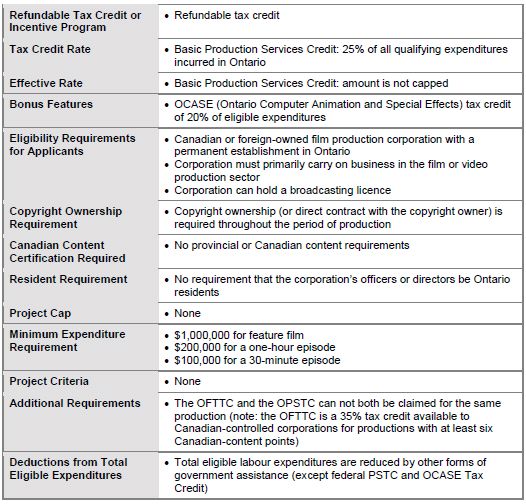

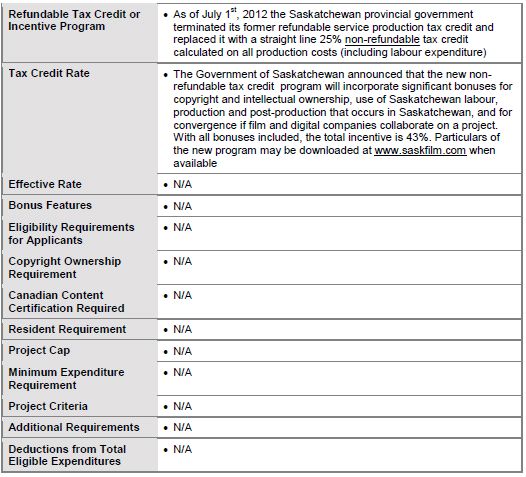

The attached chart provides a brief overview of the various provincial film and television tax credit programs as they exist on August 2012. Please consult the applicable provincial funding agencies at the links provided on pages 9–11 for full particulars, limitations and restrictions applicable to these provincial tax credit programs.

CANADIAN CONTENT PROGRAM RECOGNITION FOR CO-VENTURES

Canada is currently a party to over 50 international treaties setting rules and procedures for Official Co-Productions with other nations qualifying those productions, or the Canadian component of those productions, as domestic productions for the CPTC and other Canadian public sector financing initiatives. However, no co-production treaty exists or is anticipated with the United States of America.

Having said this, both Official Co-Productions and other qualifying co-ventures may still be eligible for Canadian content program recognition, as designated by the Canadian Radio-television and Telecommunications Commission ("CRTC").

The CRTC is the Canadian agency responsible, among other things, for the administration of the Broadcasting Act (Canada), and the licensing of Canadian broadcast undertakings. In the licensing of broadcast undertakings, the CRTC assures a voice for Canadian content programming by mandating defined levels of Canadian programming during various hours of the broadcast day. Moreover, the CRTC mandates minimum expenditure requirements on Canadian programming by Canadian pay and specialty television channels. In many cases then, CRTC "Canadian content" designation is advantageous in negotiating Canadian broadcast licenses and in garnering greater Canadian broadcast license fees.

Clearly, film and television productions that qualify for the CPTC meet the Canadian content criteria administered by both CAVCO and the CRTC. However, programming that does not qualify for the CPTC, like programming seeking to take the benefit of the PSTC, may still achieve designation as "Canadian" for CRTC purposes if it qualifies as produced pursuant to a Co- Venture under the CRTC's guidelines.

In order to qualify as a CRTC recognized Canadian co-venture, the following thresholds must be met:

- A Canadian producer must have an equal measure of decision making responsibility over the creative elements of production;

- The Canadian producer must have both entrepreneurial and financial risk by retaining the obligation to provide 50% of the financing and 50% of the profits;

- The Canadian producer does not have to own the copyright;

- An expenditure test must be met:

- In the case of a co-venture with a US-based partner, 75% of the production costs must be spent to or for Canadians, and 75% of processing and final preparation must be paid to or for Canadians; or

- In the case of a co-venture with a co-producer from a

Commonwealth or French-speaking country, or from a country with

which Canada has a co-production treaty, 50% of the production

costs must be spent to or for Canadians, and 50% of processing and

final preparation must be paid to or for Canadians;

and

- A Canadian content points test must be met:

- In the case of a co-venture with a US-based partner, at least six CRTC points must be achieved; or

- In the case of a co-venture with a co-producer from a Commonwealth or French-speaking country, or from a country with which Canada has a co-production treaty, at least five CRTC points must be achieved.

Slightly varied criteria apply to co-venture production packages (i.e., co-ventures for more than one production undertaken by a Canadian and a foreign producer).

Canadian content points are as follows:

|

Live Action (including continuous action animation) |

|

|

Production Element |

Points |

|

Director Screenwriter Lead Performer or First Voice Second Lead Performer or Second Voice Production Designer Director of Photography Music Composer Picture Editor |

2 2 1 1 1 1 1 1 |

|

Animation (other than continuous action animation) |

|

|

Production Element |

Points |

|

Director Scriptwriter and Storyboard Supervisor First or Second Voice or First or Second Lead Performer Design Supervisor Layout and Background (location) Key Animation (location) Assistant Animation/In-Betweening (location) Camera Operator (person) and Operation (location) Music Composer Picture Editor |

1 1 1 1 1 1 1 1 1 1 |

At least one of the director or the screenwriter must be Canadian, and at least one of the two lead performers must be Canadian.

USEFUL LINKS

Canadian Film or Video Production Tax Credit (CPTC)

www.pch.gc.ca/cavco

Alberta Film Commission

www.albertafilm.ca

BC Film + Media

www.bcfilm.bc.ca

Film or Video Production Services Tax Credit (PSTC)

www.pch.gc.ca/cavco

Manitoba Film and Video Production Tax Credit

www.mbfilmmusic.ca

New Brunswick's Labour Incentive Film Tax Credit

www.nbfilm.ca

Newfoundland and Labrador Film and Video Industry Tax

Credit

www.nlfdc.ca

Nova Scotia Film Industry Tax Credit

www.film.ns.ca

Nunavut Film Deveopment Corporation

www.nunavutfilm.ca

Ontario Film and Television Tax Credit (OFTTC)

www.omdc.on.ca

Ontario Interactive Digital Media Tax Credit (OIDMTC)

www.omdc.on.ca

Ontario Production Services Tax Credit (OPSTC)

www.omdc.on.ca

Prince Edward Island Film & Television Office

http://www.innovationpei.com

Québec Film and Television Production Tax Credit

www.sodec.gouv.qc.ca

Québec Production Services Tax Credit

www.sodec.gouv.qc.ca

Saskatchewan Film Employment Tax Credit (SFETC)

www.saskfilm.com

Yukon Film Incentive Program

www.reelyukon.com

Cultural Agencies

Telefilm Canada

www.telefilm.gc.ca/accueil.asp

National Film Board

www.onf.ca

Funding Agencies

Ontario Media Development Corporation

www.omdc.on.ca/site11.aspx

Canadian Film Centre

www.cfccreates.com

Canadian Media Fund

www.cmf-fmc.ca

Société de développement des entreprises

culturelles (SODEC)

www.sodec.gouv.qc.ca

Professional Associations

Canadian Media Production Association (CMPA)

www.cmpa.ca

OVERVIEW OF PROVINCIAL TAX INCENTIVE PROGRAMS

Alberta

British Columbia

Manitoba

New Brunswick

Newfoundland

Nova Scotia

Nunavut

Ontario

Prince Edward Island

Québec

Saskatchewan

Yukon

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.