TEN Estate Planning Conference

- INTRODUCTION

-

1.1 Superannuation is increasingly a major asset for more and more Australians.

For retirees and those approaching retirement, superannuation is often the next largest or only other asset after the main residence due to the tax benefits available for investment income. For younger Australians, automatic group insurance cover in retail and industry superannuation funds means that they often have substantial life insurance (far in excess of their contributions) in superannuation.

Superannuation is also a significant asset for all those people in between, due to a combination of insurance, the effects of superannuation guarantee over the course of their careers and reduced contribution caps forcing people to start planning for retirement earlier in life.

Given its significance, it is critical that superannuation is properly dealt with regardless of whether preparing a basic Will or implementing a complex estate planning strategy.

Increasing attacks by estate litigators on the superannuation death benefit payments over the last few years has highlighted the number of potential traps that advisers can be guilty of when implementing a superannuation death benefit plan. Disputes about superannuation, and in particular self-managed superannuation funds, are becoming de facto estate challenges.

1.2 Too often, estate planning strategies do not consider how superannuation integrates into the estate plan or the estate planning and superannuation strategies have not been considered at the same time.

It is essential to consider both estate planning and superannuation when developing any strategy. A strategy that builds wealth in superannuation, but does not consider how it will be passed on is flawed, as is an estate plan that does not specifically consider the issues inherent in superannuation death benefit planning.

We have seen situations where a client had a great superannuation strategy and a great estate planning strategy, but they had been developed independently. As a result, they did not work together and, when combined, failed to achieve the client's ends.

1.3 The aim of this paper is to provide a brief overview of some of these traps and opportunities we have as advisers to assist clients achieve their objectives. It is important to remember that, regardless of the complexity, good estate (and superannuation death benefit) planning is about providing certainty for both the Will-maker and the ultimate beneficiaries. It is our job to ensure that there is no dispute.

- DEATH BENEFIT PLANNING

-

2.1 There are many elements that interact together and must be considered and balanced in light of the various strengths and weaknesses when dealing with superannuation death benefits, including:

- the terms of the trust deed, which are paramount, and the applicable trust law;

- the requirements of the Superannuation Industry (Supervision) Act 1993 and Regulations 1993 (to be referred to as the SIS Act and SIS Regulations);

- the tax implications on superannuation death benefits under the Income Tax Assessment Act 1997 ; and

- where there is a trustee company, the terms of the constitution and the application of the Corporations Act 2001.

Payment of superannuation death benefits

2.2 Superannuation death benefits do not automatically form part of an estate and therefore cannot be primarily dealt with in a Will.

As a result, it is critical to understand how superannuation death benefits are paid so that an appropriate estate planning strategy can be developed.

2.3 Death is a compulsory cashing condition – therefore a benefit must be paid from the superannuation fund in some form after the death of a member.

2.4 The SIS Regulations set out how and to whom the superannuation death benefit can be paid, but within that class provides the trustee with an absolute discretion.

Who can receive a superannuation death benefit?

2.5 Under regulation 6.22, the trustee can pay to any 'dependant' or to the legal personal representative.

If the death benefit is paid to the legal personal representative to be dealt with in accordance with the Will, there is no restriction on who can receive the death benefit. The Will can leave the death benefit to a person even if they are not a 'dependant'.

2.6 'Dependant' is defined in section 10 of the SIS Act to include:

- the deceased's spouse;

- the deceased's children;

- people who are, at the date of death deceased's death:

-

- actually financially dependent on the deceased; and

- in an interdependency relationship with the deceased.

2.7 The definition of 'spouse' in the SIS Act has been amended by the Same-Sex Relationship (Equal Treatment in Commonwealth Laws – Superannuation) Act 2008 to include people:

- in a registered relationship (some states have the ability to formally 'register' relationships); and

- who, although not legally married, live together on a genuine domestic basis in a relationship as a couple.

This expands the scope of 'spouse' and opens it to a wider category of people, particularly same sex couples who were not included in the old definition.

Section 22C of the Acts Interpretation Act 1901 contains a list of factors to consider whether people are in a 'de facto relationship', which are similar to those used in the Family Law Act 1975. Although the phrase 'de facto relationship' is not used in the SIS Act, these factors could be helpful in deciding whether a couple are 'spouses' for the purposes of the SIS Act.

The factors are:

- the duration of the relationship;

- the nature and extent of the couple's common residence;

- whether a sexual relationship exists;

- the degree of financial dependence or interdependence, and any arrangements for financial support between the couple;

- the ownership, use and acquisition of the couple's property;

- the degree of mutual commitment to a shared life;

- the care and support of children; and

- the reputation and public aspects of the relationship.

2.8 The definition of 'child' in the SIS Act has also been amended1 to include:

- an adopted child;

- a step-child;

- an ex-nuptial child;

- a child of the person's spouse; and

- a child under the Family Law Act 1975.

This again expands who can be considered a 'dependant' for superannuation. For example, if you have a 'spouse', then your 'child' includes your spouse's children, which effectively includes your spouse's step-children.

However, it is important to remember that your spouse's children will only remain your 'child' for superannuation death benefit purposes while their parent remains your spouse. If that child's parent dies first, then that child will not be a 'child' for the purposes of the survivor's superannuation death benefit and therefore the client will only be an eligible beneficiary if they have been formally adopted or are in a financial or interdependency relationship with the survivor.2 This is a particular issue for blended families.

The inclusion of a person as your 'child' is not dependent on the relationship you have with them, so it could dramatically impact on the scope of people who are included in the definition of dependant.

2.9 The 'interdependency relationship' is a more recent addition. Two people are in an interdependency relationship if:

- they have a close personal relationship;

- they live together;

- one provides the other with financial support; and

- one provides the other with domestic support and personal care (section 10A of the SIS Act).

Examples could include:

- same sex couples (although same sex couples will now usually be 'spouses');

- parents and children; and

- siblings.

There is an exception to the requirement to 'live together' where one or both of the parties to the relationship suffer from a physical, intellectual or psychiatric disability.

In what form can a superannuation death benefit be paid?

2.10 Regulation 6.21 permits the trustee of a superannuation fund to pay the death benefit as either a lump sum or a pension. This paper will not explore the issues in relation to the form of the superannuation death benefit payment in detail.

2.11 However, it is important to note that a pension can only be paid where the recipient is a 'dependant' of the deceased at the time of death.

Also, there are additional restrictions where that person is a 'child' of the deceased (see regulation 6.21(2A)).

The importance of the trust deed

2.12 While the SIS Regulations outline the compliance requirements for the payment of death benefits, the trust deed for the superannuation fund is paramount when it comes to paying a superannuation death benefit. It is essential that this is properly considered as part of the estate planning process. In my experience, the trust deed is often less flexible and imposes additional and unnecessary requirements on the payment of a superannuation death benefit.

2.13 That being said, most superannuation trust deeds still afford the trustee a wide discretion to determine how death benefits are paid – although that discretion is subject to the terms of any reversionary pension or binding nomination.

- REMOVING THE TRUSTEE'S DISCRETION

-

3.1 The trustee's discretion in relation to the payment of superannuation death benefits can be a very powerful tool in ensuring that the superannuation death benefit is dealt with appropriately. This is particularly the case in the SMSF environment, where you have control over the distribution and can use the benefits from superannuation payments very effectively with full knowledge of the facts at the time of making the decision.

3.2 However, there are cases where a lack of certainty and wide flexibility created by the trustee's discretion can be a serious problem. This issue has been dealt with in detail in a great number of papers and is a subject entirely of its own. It is not the purpose of this paper to discuss this issue in detail, however it will be particularly important to remove the trustee's discretion where:

- it is not possible to adequately control the decision making process where a death benefit is payable (especially in a retail or industry superannuation fund);

- there is no appropriate person to make the death benefit decision;

- there is a risk of a dispute or a disagreement between the controllers of the >superannuation fund following death;

- there are multiple families and you want your superannuation to be paid to a particular family member (rather than another – for example to children from any of your marriages instead of your current spouse);

- there is a high risk of your wishes not being implemented by the controller of the SMSF; and

- there is likely to be an argument between possible beneficiaries as to what will happen with your superannuation benefits.

This is a non-exhaustive list but provides examples of the more common situations where removing the trustee's discretion should be considered.

3.3 The disadvantage of taking this course of action is the loss of flexibility in being able to have the benefit paid to the appropriate person based on the situation at the time. For this reason, we do not recommend removing the trustee's discretion as a matter of course – locking in a decision can be very useful in the right circumstances but the usefulness needs to be weighed against the loss of flexibility.

3.4 Given these issues, there is no universal answer for death benefit planning – for many people the flexibility inherent in superannuation is very important and useful, and for others the ability to lock in the payment is vital.

3.5 There are a number of ways that the trustee's discretion can be removed:

- binding death benefit nomination;

- reversionary pension;

- specially drafted trust deed provisions; and

- separate SMSFs.

Binding nominations

3.6 This paper discusses binding death benefit nominations in detail in parts 4 and 5.

Reversionary pensions

3.7 A reversionary pension is a pension that continues to another beneficiary on the death of the original pensioner.

3.8 Set up properly, the reversion is automatic – it takes no decision of the trustee for it to occur. This means it can be an effective way to remove the trustee's discretion in choosing the recipient of a death benefit payment.

3.9 A pension can only revert to a 'dependant' (see paragraph 2.6), and there are further limits on a dependant who is a child receiving a death benefit as a pension (broadly the child must be under 18, or under 25 and dependent, or disabled). A death benefit pension cannot be paid, for example, to the estate of the deceased member. Bear in mind particularly, as discussed earlier, that former step-children cease to be a child (and so cease to be a 'dependant' merely because of the step-parent/step-child relationship), so, when choosing who is to be a reversionary beneficiary, it is important to make sure the trustee can pay a pension to the nominated recipient.

3.10 There is some controversy about whether a pension can be changed between reversionary and non-reversionary, or the reversionary beneficiary changed, once the pension has commenced. Current practice has been generally to stop the pension (roll back into accumulation phase) and then start a new pension with the changed reversion. This can have issues with component changes as the pension will mingle with any accumulation balance and other pensions rolled back at the same stage, and may provide Centrelink issues if rolled back and restarted after 1 January 2015.

There is little in the SIS Act and Regulations about reversionary pensions, and the ATO over the years has put out two different views on this question.

3.11 Practitioners generally now accept that if a pension is commenced and the pension terms allow the pensioner to change the reversionary status, the pension can change the reversionary beneficiary. There is no clear legislative authority to support this.

3.12 As with all SMSF issues, it is important to check the trust deed to ensure it allows for reversionary pensions so the trustee must follow the reversion and no longer has discretion about how and to whom the death benefit is paid. Not all trust deeds adequately deal with this and many leave a hole and room to argue.

3.13 The other vital documents are the pension documents themselves. Do they require the trustee to continue the pension after the death of the member to the reversionary beneficiary? It is important this is spelt our clearly in the pension documents, and this also means the pension documents themselves can be produced at the time of death – which maybe years or even decades after the pension commenced.

3.14 Another trust deed issue is what happens if there is both a reversionary pension and an inconsistent binding nomination in place when a member dies – which must the trustee follow? A good trust deed will prescribe which has precedence, but, again, many do not deal with this issue, which again could lead to arguments.

Bespoke deeds

3.15 A third alternative is to put in place a special SMSF trust deed that limits what can happen with benefit payments, control arrangements and the like.

3.16 'Off the shelf' trust deeds are designed to be flexible and provide alternatives to suit a vast array of possibilities. They will not be tailored to specific situations or work for every client.

3.17 Some examples to consider include provisions:

- about how new trustees are appointed after death or disablement (discussed elsewhere in this paper);

- that stop the trustee from making a death benefit payment for a certain period after death;

- restricting the payment of a death benefit to a pension with specific rules (for example a maximum yearly draw and no ability to commute); and

- reducing the potential recipients of a death benefit payment.

3.18 There are potential traps in bespoke trust deeds. These include:

- the risk of a later wholesale trust deed update deleting the tailored provisions;

- the client's situation changing and the limitations no longer being appropriate;

- not removing or limiting the trustee's power to amend the trust deed so the trustee can change the special provisions; and

- not limiting the member's ability to roll out to another fund without the provisions.

Separate SMSFs

3.19 Is it simply enough to lock in a death benefit provision, or have special mechanisms to pass control?

Unfortunately, this is not always enough to prevent a dispute, and one often overlooked strategy is to have husband and wife with separate SMSFs.

3.20 Although this option does not remove a trustee's discretion, this can be a very valuable solution in the right circumstances

3.21 Separate SMSFs allow each spouse to implement an SMSF succession strategy that does not require any involvement from the other. If this strategy is implemented properly, it will avoid the issues that arose in Wooster v Morris. This allows a spouse to have more flexibility in distributing death benefits (as we can plan for a decision maker without the inherent conflict of the spouse), and can also be important as there are unfortunately situations where a person may choose to ignore documents by which they are legally bound (as was the case in Wooster v Morris3 ).

Determining the most appropriate beneficiary

3.22 In our view, it is critical that this is not determined in isolation. Every decision in relation to how to pay a superannuation death benefit, whether it is by way of binding nomination, reversionary pension or specially tailored trust deed, is an estate planning decision.

Any adviser who assists a client with removing the trustee's discretion can completely undermine the best estate plan if they do not consider this in the context as a whole.

3.23 Also, if you do recommend removing the trustee's discretion, there is no such thing as a 'default' or 'fall back' beneficiary choice, this includes the estate.

The choice of beneficiary must be the result of in-depth thought and analysis, even more so than any discussion around receipt of superannuation death benefits as the result of desired use of trustee discretion. This is because you are removing the trustee's discretion and lose the ability to deal with the varying range of possibilities that might exist at the time of death.

3.24 It is the job of the adviser who recommends removing the trustee's discretion to carefully consider the probability of all situations and way up the pros and cons of locking in a particular decision in a particular form.

For example, it is almost negligent to recommend a binding nomination in favour of the estate where there is a:

- concern or a likelihood of the estate being insolvent but for the superannuation death benefit; or

- risk of an estate challenge.

It is an applicant's solicitor's dream for the size of the estate (except in NSW where the notional estate concept applies) to be increased by a significant superannuation death benefit payment.

3.25 Further, it is unlikely that the estate will be the default option where the superannuation death benefit is to be paid to a surviving spouse, as it is generally desirable to maintain the death benefit in the superannuation system by paying the death benefit as a pension.

However, this does not mean that a binding nomination or reversionary pension to the surviving spouse is the default option where they are the intended recipient – this is generally for the same reasons as set out above. Despite this, we continue to see a number of advisers who have every person who walks through the front door of their office sign up to a binding nomination or implement a reversionary pension in favour of the surviving spouse without thinking through the consequences. The amount of times we have had to take urgent remedial action continues to astound.

- BINDING DEATH BENEFIT NOMINATIONS

-

4.1 A binding nomination allows a member to pre-make the death benefit payment decision, therefore removing the ability of the trustee to determine who will receive the death benefit.

4.2 In addition to specifying who can receive the death benefit, it is possible for a binding nomination to also specify how the beneficiary is to receive the death benefit (subject to the trust deed).

4.3 A number of commentators are now breaking the discussion on binding nominations up into two separate categories, binding nominations themselves and death benefit agreements.

In our view, this is a distinction without any difference and unnecessarily complicates the discussion on binding nominations. Practically, they are both creatures of the trust deed and therefore operate in the same way. Commentators who refer to death benefit agreements are really only talking about a detailed version of a binding nomination.

4.4 Section 59 of the SIS Act and regulation 6.17A of the SIS Regulations allow the trust deed of a superannuation fund to be structured such that a member can make a nomination that is absolutely binding on the trustee in relation to how their death benefit is to be paid.

However, the provisions in the SIS Act and the SIS Regulations regarding binding nominations only apply to retail and industry superannuation funds and not SMSFs. 4 As a result, there are slightly different considerations for each type of fund.

Binding nominations and retail/industry superannuation funds

4.5 The SIS Act and SIS Regulations only allow a superannuation trust deed to contain the provisions enabling binding nominations – they do not themselves give the beneficiary the power to make a nomination that is binding on the trustee. For a member to be able to make a binding nomination, the trust deed for the superannuation fund must be appropriately worded. Therefore, it is essential before making a binding nomination that the trust deed provisions are carefully considered.

4.6 Also, any process specified in the trust deed must be followed. For example, if the deed contains a form that must be used, that form must be used. If the trustee must acknowledge the nomination, then we must have evidence that the trustee has issued an acknowledgement.

We are starting to see cases5 where the validity of binding nominations are being tested, and we see this continuing to be a battleground for estate litigators given the substantial wealth in superannuation. We have given a number of advices where superannuation trustees can ignore a document that was designed to be a binding nomination because it did not comply with the terms of the trust deed.

4.7 In addition to the trust deed requirements, there are quite a number of technical requirements for a binding nomination to be effective for retail and industry superannuation funds set out in SIS Regulations 6.17A and 6.17B. In summary, these are:

- The trustee must give sufficient information to the member so the member understands the member's rights to make a binding nomination.

- The nominees must be dependants of the member or the member's legal personal representative.

- The proportion that is payable to each nominee is certain or readily ascertainable.

- The nomination is in writing, signed by the member in the presence of two witnesses who are over 18 and not mentioned in the nomination.

- The trustee must advise the member each year that the member has made a binding nomination, who are the nominated beneficiaries and when it lapses.

The trustee also has an obligation to clarify a nomination if the nomination is not sufficiently clear to allow the trustee to pay a benefit.

4.8 Further, in a retail/industry superannuation fund the nomination is only binding for a maximum of three years (compare this to SMSFs), at which time the nomination lapses and is no longer binding on the trustee. If a beneficiary wishes to continue with the binding nomination, then they will have to make a new one.

4.9 A binding nomination can be changed at any time, so when you review a Will you should consider whether the client should have one or not, and whether you should change any existing one.

4.10 Even though retail and industry superannuation funds may provide the same opportunity to make binding nominations, practically the attitude of professional superannuation trustees in my experience limits the estate planning opportunities. For example, most retail and industry superannuation funds do not allow you to make cascading or conditional nominations. This effectively removes the majority of the tools out of any estate planner's toolkit.

Binding nominations and SMSFs

4.11 As the legislative provisions have no bearing on the binding nomination process in SMSFs, the provisions of the trust deed are paramount.

4.12 As discussed at paragraph 4.6, the process specified in the trust deed must be followed precisely. Where the process is not followed precisely (or we cannot prove it was followed precisely), the nomination will not be binding on the trustee and it is highly likely, given the prevalence of estate litigation, to find this the subject of a challenge.

4.13 As binding nominations in SMSFs are purely a trust deed concept, they are not subject to the maximum three year validity that applies to binding nominations for retail and industry superannuation funds (see regulation 6.17A(7) of the SIS Regulations, SMSFD 2008/3, Ioppolo v Conti6 and Munro v Munro7 ). Therefore, unless there is a restriction in the SMSF trust deed, it is possible to make a non-lapsing binding nomination in an SMSF.

4.14 Also, when preparing binding nominations for an SMSF it is possible to utilise your drafting skills so that the binding nomination can cover a multitude of situations. Unlike in the majority of retail and industry superannuation funds, the trustee will accept cascading or conditional nominations. Commonly, SMSF binding nominations even specify the form in which the death benefit is paid to the beneficiary.

We have even seen situations where complex restrictions are placed on the payment of a death benefit pension to ensure that a 'spendthrift' surviving spouse does not have access to all the money.

Binding nominations – make sure they have the intended outcome

4.15 Once the decision is made to make a binding nomination, it is essential that careful consideration is given to the terms of the trust deed to ensure that the binding nomination has the intended outcome.

4.16 Part 5 outlines the common issues we see that can affect the validity of a binding nomination and give rise to a challenge.

4.17 However, there are a few other common mistakes that do not result in the binding nomination being invalid, but merely impact on the effectiveness of the binding nomination.

Entire member benefits

4.18 There are a number of trust deeds where the operative provision only allows the binding nomination to deal with benefits in an 'accumulation account'.

Therefore, any amount in a pension account will possibly not be subject to the binding nomination. However, this is not entirely clear and there is an argument that the amounts in pension accounts are commuted and form part of the accumulation account following the death of the member.

Some deeds lock in the decision in the death benefits provisions, but then in the separate provisions dealing with pensions allow the trustee discretion again. This means a binding death benefit nomination will be very difficult to uphold if the client is drawing a pension at death.

Payment priority

4.19 One of the more common debates in the superannuation industry at the moment is whether a binding nomination takes precedence over a reversionary pension. A reversionary pension is a pension that is being received by a member of a superannuation that expressly provides that the pension is to continue to another nominated person on the death of that member.

This issue is once again governed by the terms of the trust deed for the superannuation fund. Any good trust deed should clearly specify the order of priority if there is both a binding nomination and a reversionary pension.

The most common approach taken in superannuation trust deeds that deal with this issue is that a reversionary pension takes precedence over a binding nomination. The reasoning behind this is that, if the pension is taken to automatically continue under the reversionary pension rules, it never forms part of the death benefit to be dealt with by the binding nomination.

However, this is not always the case. There are many trust deeds that provide that a binding nomination overrides any reversionary pension or are silent on which takes priority. The latter situation is particularly problematic as, without clear guidance in the trust deed, there is the risk of having competing beneficiaries.

- CHALLENGING THE VALIDITY OF BINDING DEATH BENEFIT NOMINATIONS

-

5.1 To be honest, we are surprised that we have not seen more cases where binding nominations have been the subject of the estate litigation, particularly given the number of times I have provided advice to SMSF trustees that a particular 'binding' nomination was not in fact 'binding' on the trustee.

However we have recently seen a few cases where the validity of a binding nomination was in question. Given that the large amount of money held in superannuation that can be effectively diverted from an estate challenge (except in New South Wales where the notional estate concept applies), we see this becoming a key battleground for estate litigators.

5.2 As highlighted throughout this paper, it is critical for a binding nomination to be made in accordance with the requirements in the trust deed. This is where the majority, if not all, of the challenges to a binding nomination are going to come from.

Common mistakes when implementing binding nominations

5.3 In our experience, practitioners generally make the same common mistakes when implementing a binding nomination. Although in-depth discussion of the issues is a topic in itself, the following are what we consider to be the common mistakes made by practitioners that could give rise to questions in relation to the validity of a binding nomination.

Approved form

5.4 There are a number of common trust deeds in circulation that require the binding nomination to be made in the 'approved form'.

- (a) Usually, this requires the member to use the specific form set out in the schedule to the particular trust deed. In the grand scheme of things, this is a fairly basic condition to satisfy, but it is surprising how many times it is not.

-

In most of these situations, we cannot be sure of the reasons why this requirement has been overlooked. However, the most compelling reason seems to be that the specified form did not have sufficient flexibility to cater for the practitioner's drafting style (for example, it was not possible to make cascading nominations).

Unfortunately, where the 'approved form' is not used, it is irrelevant how well the alternative form is drafted, as it will not be binding on the trustee.

As mentioned many times in this paper, the provisions of the trust deed are of paramount importance. Where they are not complied with, there is no room for movement. Unlike in the world of drafting a Will, there is no such thing as substantial compliance or testamentary intention.

Therefore, if the trust deed requires a certain form to be used, that is the only form in which a binding nomination can be made and be binding on the trustee.

If you do not like it, amend the trust deed, not the form.

- An even bigger problem is caused by trust deeds that require the binding nomination to be made in the form 'approved' by the trustee.

-

These trust deeds do not usually include a default or pre-approved form and it is therefore up to the trustee to decide at the time what is the 'approved form'. As a result, the trustee must have taken an active step to 'approve' a form before a nomination can be binding on the trustee.

Even where this step is taken by the trustee, such provisions are at high risk of a challenge. This is because, if put to proof, the parties will need to produce evidence that the trustee 'approved' a form and that the form of the binding nomination used was in fact the 'approved form'.

To date, not one client or adviser has been able to produce sufficient documentary evidence to show me that this requirement was satisfied where a client has made a binding nomination under a trust deed with such a provision.

As a result, we do not like to gamble on clients keeping adequate records to prove this issue if challenged. For this reason, we are inclined to vary trust deeds to remove this requirement when making a binding nomination even though it is technically possible to make a valid binding nomination under such provisions.

Eligible beneficiaries

5.5 Another common mistake is that the binding nomination nominates a beneficiary that is either:

- not an eligible recipient for the purposes of the SIS Regulations; or

- they are an eligible recipient for the purposes of the SIS Regulations but the trust deed provisions (in particular the definitions) are inexplicably narrow.

A common example that arises is where a person makes a binding nomination in favour of their de facto spouse but the trust deed defines a 'spouse', for the purposes of the 'dependant' definition and the binding nomination clause, to only include a married spouse. In this case, the binding nomination to the de facto would not be valid as they are not a permitted beneficiary under the trust deed.

In one prominent superannuation trust deed, a binding nomination can only be made to a dependant and not to the estate.

Therefore, it is critical that the terms of the trust deed, including every relevant definition, are carefully considered when making a binding nomination to ensure that it is valid.

Also, it is critical that the binding nomination itself correctly refer to the intended beneficiary. As the power to make binding nominations for SMSFs is solely based on the provisions of the trust deed, the courts have insisted on strict compliance with the requirements of the trust deed when determining the validity of binding nominations.

In the recent Queensland Supreme Court case of Munro v Munro8 the binding nomination was found to be invalid, allowing the trustees of the SMSF to distribute the deceased's death benefit other than as set out in the nomination. The Court held the binding nomination was not valid as it did not comply with the requirements in the trust deed. The Court emphasised that the binding nomination would only be binding if it strictly complied with all the requirements of the trust deed. In this case, the nomination was to the 'Trustee of Deceased Estate' rather than the deceased's 'legal personal representative' as required by the trust deed and the SIS Act. The Court determined that this was not a nomination of the deceased's 'legal personal representative' (as required by the trust deed and the SIS Act) as the roles were different.

Eligibility to make a binding nomination

5.6 This issue is a twist on the situation in the section above.

It is dangerous to assume that every member of a superannuation fund is able to make a binding nomination.

There are SMSF trust deeds that allow a 'member' to make a binding nomination, although, the definition of 'member' did not include a person whose only interest in the SMSF was their pension account. As a result of this drafting oversight, only a person with an accumulation balance in the superannuation fund could make a binding nomination.

Trustee acknowledgement

5.7 Another common binding nomination provision requires the trustee to 'acknowledge' the binding nomination for it to be valid and binding on the trustee.

Although this is not a difficult provision to comply with, such provisions are high risk. If there is a dispute, the parties will need to produce evidence that the trustee 'acknowledged' the binding nomination. In our experience this step is not often completed satisfactorily, or where it has been attended to, the client does not keep adequate records to establish this at the time of payment of the death benefit.

Also, this clause presents a problem where the trustees/members have separated and one of the members wishes to make a new binding nomination. As the nomination has to be acknowledged by the trustee, you have to get the ex-spouse to consent to the new binding nomination for it to be valid. As you can imagine, this can be rather difficult.

Information to members

5.8 A similar issue arises where the trust deed requires the trustee to provide information to the member before they can make, or before the trustee can accept, a binding nomination. The following is an example of such a clause:

Information to Member: Before the Trustee accepts a Binding Death Nomination, the Trustee must give the Member a statement that...Required compliance

5.9 Another critical mistake is that the binding nomination clause and the death benefit provisions in the trust deed do not work together.

Usually, the problem arises because the death benefit provisions do not 'require' the trustee to pay the death benefit in accordance with the binding nomination made by the member. The following is an example from a well-known trust deed:

Where this Deed provides for the payment of a Benefit on the death of a Member, the Trustee may pay or apply the Benefit to or for the benefit of the Nominated Dependants...As you can see, this clause provides the trustee with a choice to follow the binding nomination or pay the death benefit in accordance with the trustee's discretionary power. As a result, for the binding nomination to be 'binding' this clause needs to be amended.

Also, do not be surprised to see trust deeds where the death benefit provisions do not even refer to the binding nomination at all. In this case, depending on the exact wording of the binding nomination clause, it is likely that the binding nomination will not remove the trustee's discretion in relation to the payment of the death benefit.

Compliance with the SIS Act and SIS Regulations

5.10 By far the most common issue that arises in SMSF trust deeds, including trust deeds from extremely reputable and experienced providers, is where the binding nomination provisions require the binding nomination to comply with the requirements of the SIS Act or SIS Regulations.

In our experience, these provisions usually present in one of two forms:

- The definition of binding nomination in the trust deed refers to a binding nomination 'made in accordance with section 59(1A) of the SIS Act'.

- The operative clause in the trust deed requires the binding nomination to comply with section 59(1A) or regulation 6.17A (or both) for the trustee to be bound.

As mentioned earlier, neither the SIS Act nor the SIS Regulations provisions relating to binding nominations apply to SMSFs. Therefore, in my view, the trustee of the SMSF will not be bound by the binding nomination where the trust deed requires the binding nomination to comply with or be binding under the SIS Act or SIS Regulations.

This is contrasted to a provision that does not require compliance with section 59(1A) or regulation 6.17A but merely imports the technical requirements set out in those provisions into the trust deed.

5.11 This issue was the subject of the dispute in the case of Donovan v Donovan. 9

In this case, the deceased (Mr Donovan) was a member of the SMSF and a director of the trustee company. The operative provision that allowed the member to make a binding nomination was clause 11.4(b) of the trust deed, which provided as follows:

A member may make a binding death benefit nomination in the form required to satisfy the Statutory Requirements;The trust deed provided as follows:

- 'Statutory Requirements' was defined widely to include 'any law...which must be satisfied by a superannuation fund in order to qualify for income tax concessions...'.

- Where a member had made a valid binding nomination, the trustee must pay the death benefit to the nominated legal personal representative or dependant of the member.

The deceased purported to make a nomination by letter to the trustee which specified that he wanted his benefits paid to his legal personal representative for inclusion in his estate assets.

The deceased's second wife and a child of the deceased's first marriage, who were the deceased executors, were disputing whether this was a valid binding nomination that had to be followed by the trustee. The second wife argued that the nomination was binding on the trustee.

However, the deceased's children argued that the nomination was not binding for two reasons:

- First, the language used was not sufficient to convey a binding intention. The nomination merely indicated that the deceased 'wished' for his death benefit to be paid in a particular way, not required or directed.

- Second, the nomination was not sufficient to comply with the requirements of the 'Statutory Requirements'.

In addition to these issues, Fryberg J raised the issue of the 'approved form', but neither party pursued this issue and, in any event, it was irrelevant to the end result.

Fryberg J dealt with the second issue first and held that the reference to 'Statutory Requirements' for the purposes of the binding nomination provision was a reference to the formalities in regulation 6.17A(6) of the SIS Regulations as to read the clause in the trust deed in any other way would render the provision meaningless.

The formalities in the SIS Regulations required the nomination to be in writing, witnessed by two persons and contain a signing declaration from the witnesses in relation to the signing of the nomination.

The letter written by the deceased to the trustee clearly did not comply with the requirement of regulation 6.17A. As a result, the nomination was not binding on the trustee.

Further, the judge ordered that the costs of the dispute be paid from the estate on an indemnity basis.

5.12 This position was affirmed by the Queensland Supreme Court in Munro v Munro10 where they held that a binding nomination in relation to benefits in an SMSF does not have to comply with the requirements in the SIS Act and SIS Regulations (unless the trust deed requires that).

5.13 As you can see, the majority of these issues result from the wording of the trust deed and can be overcome by replacing the binding nomination provisions with a provision with more user-friendly drafting. When we are preparing a binding nomination, more often than not we replace the binding nomination provisions to remove the possibility of having a dispute in relation to the above issues.

5.14 However, the recent case of Wooster v Morris11 demonstrates that practitioners must think beyond the binding nomination when advising on superannuation death benefits.

This case involved a challenge to the validity of the binding nomination. The judgment does not examine this issue as the binding nomination was found to be valid by a special referee before the hearing. However, the case demonstrates that even where there is a binding nomination, it is critical to ensure that the correct person will be running the superannuation fund in the event of the death of a member. This issue is discussed in detail in part 8 below.

5.15 Another concerning issue is the manner in which practitioners initially respond to a dispute where there is challenge to the superannuation death benefit. Quite often, where there is a binding nomination in existence, the practitioners are very quick to write a response to the claimant notifying the claimant of the binding nomination and the fact that the death benefit has been paid in accordance with that nomination.

I understand the reasons for this, as it is usually a very quick way to dismiss the dispute.

However, such a statement must not be made lightly and should only be made after a thorough review of the binding nomination and the trust deed.

If such a statement is made and the binding nomination is not in fact 'binding', the actions of the trustee in paying the death benefit could be subject to the challenge.

Challenging the trustee's actions/discretion

5.16 It is the general trust law position that the discretionary powers of a trustee are not generally subject to review and, therefore, there is very limited scope to challenge the exercise of a discretion.

This issue is extremely complex and is not the subject of this paper. However, when such a discretionary power is exercised, the trustee must inform themselves of all the relevant matters regarding the exercise of a decision.

Where it can be established that the trustee has not considered all relevant issues, it is possible for the original decision to be set aside. It is for this reason that the preferred position is not to provide reasons for the exercise of a discretion.

In the situation discussed in paragraph 5.15, if the binding nomination is not valid, the reasoning supporting the payment of the death benefit to the claimant is flawed and can be the subject of a challenge. That being said, it is often not worth challenging these issues as a court usually refers the decision back to the trustee to be re-determined.

This issue should also be considered when a claimant asks whether they were a considered beneficiary for the purposes of the death benefit payment. Great care needs to be made when responding to such claims to avoid adding fuel to the fire.

5.17 For retail and industry superannuation funds, the common law position has been modified by the Superannuation (Resolution of Complaints) Act 1993, which allows a person to complain to the Superannuation Complaints Tribunal for a review of the exercise of a trustee's discretion.

- DEALING WITH SUPERANNUATION DEATH BENEFITS IN A WILL

-

6.1 The superannuation death benefit is not an asset that forms part of the estate and cannot be dealt with under a Will unless the trustee's discretion is exercised in favour of the estate or the estate is the pre-determined recipient under a binding nomination or by operation of the trust deed.

6.2 Where the superannuation death benefit does become an estate asset, the Will can deal with the superannuation death benefit in any manner the testator determines.

6.2 Where the superannuation death benefit does become an estate asset, the Will can deal with the superannuation death benefit in any manner the testator determines.

6.3 It is essential that any well drafted Will deal with superannuation death benefits regardless of whether or not they are intended to form part of the estate for a number of reasons:

- The superannuation death benefit may form part of the estate even where this was not the desired outcome. As a result, it is critical that the consequences of the superannuation death benefit being received by the estate are properly thought through and dealt with in the Will.

- The superannuation death benefit may be paid to an unintended recipient. Since the trustee of the superannuation fund has a wide discretion, it is possible for it to be used in favour of a person who was not the desired recipient. This can result in a very different outcome to that intended by the testator particularly where the provision left under the Will was made on the assumption of the intended outcome.

For example, it is not unheard of for a trustee to decide, considering your assets, your Will and the needs of your dependants, to pay all of your benefits to a child from a previous marriage, rather than the current spouse.

In both the above situations there are some drafting considerations that should be taken into account to deal with these possibilities (see paragraph 6.11).

6.4 Also, there can be varying tax consequences depending on who receives the death benefit. Although this should not be the sole focus when formulating an estate plan, having an understanding of these is critical for any estate planner as it can be used to maximise the estate for the beneficiaries.

6.5 Additionally, where the testator has an SMSF, the control of the SMSF needs to be considered so that the death benefit decision is made by the correct person.

To adequately address the control of an SMSF on the death of the member, the Will, the SMSF trust deed and the trustee company constitution (where applicable) need to work together.

This issue is discussed further in part 8.

Superannuation death benefit testamentary trusts

6.6 There are many situations where it is desirable for estate assets and superannuation death benefits to form part of a testamentary trust. It is not the job of this paper to talk about when it is appropriate to use a testamentary trust or the ins and outs of testamentary trusts generally.

6.7 Quite often as indicated above, where superannuation is to form part of the estate, the primary reason is so that it forms part of a testamentary trust.

6.8 Where this is the case, it is important that the terms of the testamentary trust properly deal with the implications of receiving superannuation death benefits.

6.9 Even though it is possible to have a testamentary trust with a very limited range of beneficiaries, most testamentary trusts these days have a wide range of beneficiaries so that the trust is more tax effective.

However, testamentary trusts with wide classes of beneficiaries can inadvertently result in tax being payable where the assets of the testamentary trust include a superannuation death benefit. This is because the tax treatment of the superannuation death benefit depends on the extent that tax law dependants are likely to benefit from the superannuation death benefit.

Where there is a mix of tax law dependant and non-dependant beneficiaries and the trustee has a wide discretion, it is unlikely that the tax benefit in section 302-10 of the Income Tax Assessment Act 1997 will apply and the estate will be taxed as if the death benefit is paid to a non-dependant.

It is possible to draft the testamentary trust deed so that the concessional tax treatment is maintained where the testamentary trusts includes dependant beneficiaries – see paragraph 6.15. Where you have a mix of dependant and non-dependant beneficiaries, this is an important consideration as the tax treatment is substantially different.

Will clauses and superannuation death benefits

6.10 Any well drafted Will should deal with the possibility of a superannuation death benefit being received even where active steps have been taken as part of the planning process to divert the superannuation away from the estate. This means that appropriate clauses need to be inserted to deal with the possibility and the vast range of potential consequences that could apply should a superannuation death benefit form part of an estate.

In the absence of such clauses, opportunities to maximise the estate assets will be lost, which could potentially result in disgruntled beneficiaries and possibilities of allegations of negligence against the practitioner who assisted with the estate planning.

6.11 In our opinion, you should consider the inclusion of the following clauses in any Will you prepare.

Equalisation clause

6.12 Where the superannuation death benefit is intended to be split between multiple beneficiaries either directly or through the estate – for example, to the surviving children – it is essential that the Will include an 'equalisation clause'.

An 'equalisation clause' is designed to increase the portion of the estate assets left to the beneficiary who does not receive the superannuation death benefit and decrease the portion of the estate received by the beneficiary who does. This ensures that the total share of the deceased's assets (including the estate assets and the superannuation death benefit) left to each beneficiary is equal. The clause is designed to prevent one beneficiary receiving a windfall by taking the superannuation death benefit directly from the fund and then still sharing equally in the estate assets under the Will.

It is critical that this clause be included where equality between beneficiaries is important and the superannuation trustee will have a discretion as to what is to happen to the superannuation death benefit. However, it should also be included where there is a binding nomination, reversionary pension or specifically drafted death benefit clause in the trust deed. This is because, like all well-made plans, something may change.

A perfect example of where this clause may have been useful was in the case of Katz v Grossman. 12 In that case, the daughter of the deceased was the co-trustee of the SMSF and decided to pay the superannuation death benefit to herself rather than equally between her and her brother or to the estate. As a result, the daughter received a significantly larger share of the assets than her brother.

However, it is important to note that 'equalisation clauses' have some limitations. In particular, for the equalisation clause to work perfectly and equalise the total benefits left to each beneficiary, there have to be sufficient assets in the estate. For example, where there are two beneficiaries to benefit equally, the estate assets have to be worth at least the same amount as the superannuation death benefit. Where there are three beneficiaries, the estate assets have to be worth at least twice as much as the superannuation death benefit.

Dependants clause

6.13 It is our view that a Will should be drafted to minimise the tax payable on the superannuation death benefit if it is an estate asset.

To achieve this, the Will should include a 'dependants clause', which allows the executors to allocate specific assets to specific beneficiaries (or their testamentary trusts). The clause should be worded widely enough to allow the executors to allocate the superannuation death benefit, to the extent possible, to the dependant (for tax law purposes) beneficiaries to minimise any tax payable, with other estate assets going to the non-dependant beneficiaries.

This clause can result in substantial tax savings and therefore an increase in the total estate assets for the beneficiaries. We have seen this clause work extremely well where the estate is left to the deceased's children but only one of them is a 'dependant' for tax law purposes.

In the absence of a specific clause empowering the executors to do this, the estate assets may have to be proportionately split between the beneficiaries and this could result in a beneficiary having to pay tax on the portion of the superannuation death benefit they receive where they are a non-dependant.

Streaming clause

6.14 A further extension of the 'dependants clause' is a clause that allows the different components of a superannuation death benefit to be streamed to different beneficiaries. By different components, we mean the taxable, tax-free and untaxed components that usually make up a superannuation death benefit payment.

It is well known that where a superannuation death benefit is paid by a superannuation fund, each payment includes a proportionate amount of each component and it is not possible to pay different components separately to different beneficiaries. This is desirable where there are both dependant and non-dependant beneficiaries, as different tax consequences apply to each of the components.

However, where the superannuation death benefit is paid to the estate, it is arguable that the different components can be streamed to different beneficiaries. Under general trust law, it is possible for different income and capital amounts to be streamed where the trust deed provides that the different amounts retain their character and there is a clause that permits the different amounts to be streamed.

For this reason, we include a clause that allows the different components of the superannuation death benefit to be streamed to different beneficiaries. This allows the executors to allocate the tax-free component to the non-dependant beneficiaries so that no additional tax is payable and the taxable component to the dependant beneficiaries so that no tax is payable on that amount.

Sub-trust clause

6.15 As discussed in paragraph 6.9, it is common for superannuation death benefits to form part of a testamentary trust with a wide class of beneficiaries that includes dependants and non-dependants (for tax law purposes).

Without the inclusion of a specific clause in the terms of such a testamentary trust, tax will be payable on the superannuation death benefit by the estate as if it was paid to a non-dependant beneficiary – this is the case even if practically the trustee of the testamentary trust will only distribute to the dependant beneficiary. This is because the superannuation death benefit is only concessionally taxed to the extent the dependant beneficiary is likely to benefit (section 302-10 of the Income Tax Assessment Act 1997).

Therefore, the terms of the testamentary trust should include a 'sub-trust clause' that holds the superannuation death benefit on trust solely for the benefit of the dependant beneficiaries and only where there are no dependant beneficiaries, can the superannuation death benefit be paid to the non-dependant beneficiaries.

If one of the beneficiaries of the testamentary trust is a 'dependant' for tax law purposes at the time the estate is distributed, then it is our opinion that the superannuation death benefit will be taxed as if it were paid to a dependant under section 302-10 Income Tax Assessment Act 1997 where such a clause is included.

Conflict clause

6.16 In light of the recent decision in the Queensland case of McIntosh v McIntosh, 13 we believe additional caution needs to be taken where the desired recipient of the superannuation death benefit is also the executor (or potentially the administrator) of the estate.

One possible step that can be taken to address the issue in McIntosh is to include a conflict clause in the Will that expressly authorises the executor to also pay, or apply to receive, the superannuation benefits personally.

This paper addresses the McIntosh case and its importance to the way we approach estate planning in detail in part 10.

- TAXATION OF DEATH BENEFITS

-

7.1 Although there is no restriction on who can receive the superannuation death benefit under a Will, there can be varying tax consequences depending on who receives the death benefit.

The tax treatment of superannuation death benefits is a complex area that is dependent on a number of issues. The following is a brief summary of some of the key taxation issues.

7.2 There are a couple of fundamental taxation concepts that need to be understood:

- First, you need to be mindful of whether the beneficiary is a dependant for the purposes of the Income Tax Assessment Act 1997. This is a different definition to the definition of 'dependant' for the purposes of the SIS Act.

- Second, the tax rate that applies will depend on the components that make up the superannuation death benefit. Each superannuation death benefit payment will be made up proportionately of a range of components, including taxable, tax-free and untaxed, depending on how the amount came to be in the superannuation system. Each of these components has a different tax treatment.

- Third, where a death benefit is paid to multiple recipients, the proportionate rule applies. This means that each beneficiary will receive a proportion of each of the different components (and its varying tax consequences) that makes up the death benefit. See paragraph 6.11 for a discussion on the ability to stream different components where the death benefit is paid to the estate.

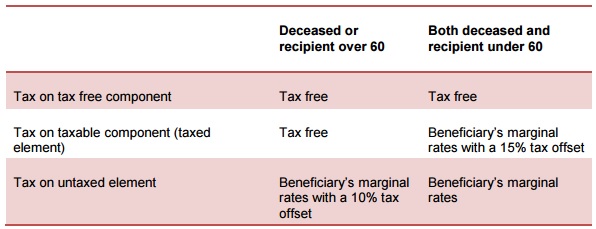

Lump sum to a tax law dependant

Lump sum to a non-tax law dependant

Pensions

Winner – EOWA Employer of Choice for Women Citation 2009,

2010, 2011 and 2012

Winner – ALB Gold Employer of Choice 2011 and 2012

Finalist – ALB Australasian Law Awards 2008, 2010, 2011 and

2012 (Best Brisbane Firm)

Winner – BRW Client Choice Awards 2009 and 2010 - Best

Australian Law Firm (revenue less than $50m)

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.