In recent years, the relevance and growth of environmental, social and governance (ESG) principles in investments has captured the attention of the global business community. With Shari'ah-compliant investing also continuing to grow, there are significant synergies between principles of Shari'ah and ESG principles. The markets have witnessed the development of innovative Shari'ah-compliant financing structures that align with ESG principles. In 2018, Indonesia became the first country in the world to issue a sovereign green Sukuk and, more recently, in March 2021, the Islamic Development Bank issued its $2.5 billion sustainability Sukuk.

These issuances have demonstrated that by adding a sustainability component to a Sukuk offering, the potential investor base is broadened such that socially responsible investors outside the traditional Sukuk fixed-income investor space may seek to diversify their holdings and participate in such offerings. We outline below the significant potential for overlap between ESG and Islamic debt capital markets and the opportunities available when aligning the two investment approaches, including a case study of a recent sustainability Sukuk issuance, on which Akin Gump advised, which exemplifies the successful coalescence of Islamic debt capital markets and sustainability.

I. Potential Growing Appetite for ESG-Focused Sukuk

Whilst Sukuk are broadly certificates of equal value representing an interest in underlying assets, groups of assets or business activity that comply with Shari'ah principles, sustainable Sukuk specifically are Shari'ah-compliant financial instruments whose proceeds are used for the funding of eligible sustainability projects. Likewise, a green Sukuk is a Shari'ah-compliant financial instrument in which issuers exclusively use the proceeds of the issuance to finance investments in renewable energy or other environmental assets (such as energy and infrastructure projects).

Shari'ah-minded investors are increasingly alive to the ESG impact of their investments. Although, to date, there have been comparatively fewer sustainable Sukuk issuances, ESG sensitivities are certainly rising globally, with investors being driven by sustainability now more than ever before. As sovereign entities, corporates and financial institutions seek to address the economic disruption caused by the global pandemic - and bearing in mind the ambitious energy targets announced by various Middle East governments such as UAE Energy Strategy 2050 and Saudi Vision 2030, all of which will require significant investment and capital - green and sustainable Sukuk, which will appeal to both the core Islamic investors in the region and the wider pool of international ESG investors, may offer a unique source of diversified capital for issuers.

With respect to the use of proceeds of an issuance, ESG-compliant assets have significant potential to also be Shari'ah-compliant; in particular, both Shari'ah-compliant and ESG investing typically prohibit investing in certain products and services, such as gambling, weapons and human trafficking. Indeed, Islamic banks have a long history of seeking to invest responsibly and promoting asset classes that align with such values. Numerous banks in the region have already advised upon and issued sustainable and green Sukuk.

Demand and pricing considerations will undoubtedly be the key drivers for the development of ESG in the Sukuk sphere. Whilst certain of the incentives that appeal to ESG investors in other jurisdictions may not necessarily extend to regional Middle Eastern investors (notably taxation deductions and beneficial regulatory treatment), there is growing awareness and understanding of ESG in the region and heightened interest in the role it can play in the Islamic debt capital markets and Islamic finance transactions more generally. Whilst structuring Sukuk within an ESG-compliant framework may result in an additional layer of complexity to any transaction, we demonstrate below how the smooth interrelation between the two may be uniquely rewarding.

II. Case Study: Kuveyt Türk Katilim Bankasi A.S. Issues World's First Regulatory Capital Tier 2 ESG and Islamic Compliant Trust Certificates

In September 2021, we advised Kuveyt Türk Katilim Bankasi A.S. ("Kuveyt Türk"), one of the leading Turkish participation banks that is majority-owned by Kuwait Finance House, on the landmark issuance of $350 million fixed-rate resettable sustainability Tier 2 certificates due 2031, listed on the Irish Stock Exchange plc (Euronext Dublin). These trust certificates are the world's first regulatory capital Tier 2 ESG and Islamic compliant trust certificates. An amount equal to the net proceeds of the issuance was applied to finance and/or refinance eligible green and/or social projects in accordance with Kuveyt Türk's Sustainable Finance Framework.

The appetite for ESG and Islamic compliant trust certificates is clearly demonstrated by the fact that the issuance was oversubscribed by 12 times with an order book of $4 billion. With the issuance achieving the tightest pricing for any Tier 2 issuance out of Turkey since 2017 at 6.125 percent, the strong fundamentals and positive market sentiments were clear.

The issuance of sustainable Tier 2 certificates worked especially well for Kuveyt Türk for a number of reasons:

First, being a member of the Kuwait Finance House family, Kuveyt Türk already conducted its operations by taking into consideration the environmental impact of its actions, undertaking various sustainability efforts and supporting sustainable project financings in Turkey including renewable energy and social housing projects. The issuance of sustainability Tier 2 certificates therefore neatly aligned with its existing values and considerations.

Second, the ability to allocate the proceeds of a given green, social or sustainable Sukuk issuance to eligible green and/or social projects that were originated no more than three years prior to the issuance permitted Kuveyt Türk to retrospectively rely on certain of its existing projects in the sustainability sphere, rather than having to earmark future new projects in which the entirety of the Sukuk proceeds needed to be invested. This principle was a critical component of the success of the transaction, in the absence of which some issuers might struggle to source new projects / allocate new purposes for the entirety of the proceeds of an issuance.

Third, in the absence of a clear, uniform definition (legal, regulatory or otherwise) of, or any market consensus as to what constitutes green, social, or sustainable projects, issuers have a broad scope and a range of international frameworks to use; Kuveyt Türk's Sustainable Finance Framework, for example, was in accordance with various international principles, including the International Capital Market Association (ICMA) Green Bond Principles 2021, ICMA Sustainability Bond Guidelines 2021 and the Loan Market Association (LMA) Social Loan Principles. In the context of Kuveyt Türk's landmark issuance, the eligible sustainable projects included those falling within the categories of renewable energy, pollution prevention and control, energy efficiency, employment generation, affordable housing and access to essential services.

Fourth, there is a global shift towards corporate reporting on sustainability as entities increasingly recognise the importance of acknowledging the impact of their operations on the environment and wider society. In addition to the publication of Kuveyt Türk's Sustainable Finance Framework, an allocation report and an impact report is due to be published by Kuveyt Türk within 12 months of the issuance. Such reporting provides investors with confidence in the sustainable value of their investments, and it was deemed not to be unduly burdensome from the perspective of Kuveyt Türk.

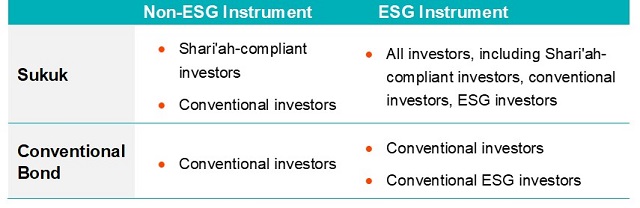

Finally, through ensuring the Tier 2 certificates were sustainability trust certificates, Kuveyt Türk was able to appeal to a broad range of investors (thereby achieving further diversification in its investor base), as demonstrated below:

The process of issuing a green or sustainable Sukuk requires a convergence of the process for issuing traditional Sukuk and the incorporation of ESG-specific elements (such as with regard to the management of the use of proceeds, independent third-party reviewers and ongoing sustainability reporting). This requires, among other things, innovative structuring, and transaction parties should seek the advice of experienced legal counsel to help them navigate such issues.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.