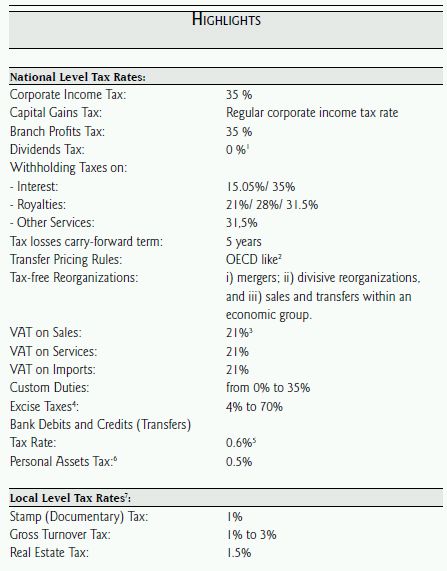

Overview

1.Income Tax

1.1. General Aspects

1.1.1. Income Tax Rate.

The general statutory corporate income tax rate for entities incorporated in Argentina including branches or permanent establishments of foreign companies is 35%.

1.1.2. Taxable Base.

All revenues are subject to income tax unless otherwise excluded by law from the taxable base. Excluded Items of Income are subtracted from Gross Income. The result is the Gross Taxable Income from which all expenses incurred in obtaining taxable income are deducted. The after-deductions result is the Net Taxable Income. The Exempted Items of Income are subtracted, resulting in the Taxable Base to which the 35 % statutory corporate tax rate is applied. The result of applying the 35 % tax rate is the Resulting Income Tax from which applicable Tax Credits are subtracted to find the Income Tax Liability.

[+] Sum of All Revenues

[=] Gross Income

[–] Deductible Expenses

[–] Exempted Items of Income

[=] Net Taxable Income (Minimum Presumptive Income Tax)

[=] Taxable Base

[*] 35% Corporate Tax Rate

[=] Resulting Income Tax

[–] Tax Credits

[=] Income Tax Liability

[=] Income Tax Charge Payable

1.1.3. Deductions.

As a general rule all costs and expenses incurred in obtaining taxable income may be deducted, including organization costs, taxes (other than income tax), donations to certain entities, amongst others. The Argentine ITL includes thin capitalization rules which impose limits on the deduction of interest payments made to affiliated parties in the cross-border context. Expenses are generally allocated to the fiscal year in which they accrue.

The ITL allows for the deduction of the following concepts:

Extraordinary losses resulting from natural hazards, theft or force majeure are deductible to the extent they are not included in insurance or otherwise indemnified, provided they involve assets which generate taxable income.

Losses arising from crimes committed by employees against business property that contributes to the generation of taxable income are deductible to the extent they are not covered by insurance or otherwise indemnified.

Fees paid to resident directors are deductible to the higher of: 25% of the book earnings or the statutory amount. Fees to non-resident directors are deductible up to 12.5% of book earnings if all earnings have been distributed as dividends.

Representation expenses are deductible up to a maximum of 1.5% of the salaries paid during the calendar year.

The ITL sets limits to the deduction of depreciation and other expenses related to automobiles.

Payments for technical assistance from abroad are deductible up to 3% of sales on which the fees are based or 5% of the investment made as a result of the assistance.

Expenses incurred or contributions made to personnel for purposes of sanitation, education and cultural improvement are deductible. In general, all payments made for the benefit of employees are deductible (e.g. end of the year bonus payments).

Start up costs and expenses may be deducted as they are incurred, or capitalized and amortized over a five year period, at the taxpayer's option.

1.1.4. Depreciation.

Buildings used to generate taxable income may be deducted at a 2% annual rate calculated over the cost of such buildings. Other depreciation rates may be used if they are technically supported.

Annual depreciation of all other depreciable assets used to generate taxable income is determined by dividing the acquisition cost of the asset by its estimated years of useful life (straight line depreciation method). The tax law does not provide standard depreciation rates.

Other depreciation methods, such as those based on units of production or time of use, may be used if they are technically justified. Amortization of goodwill, trademarks and similar intangible assets is not deductible, except when they have a set useful life.

At the taxpayer's option, organization costs may be deducted either in the year in which they are incurred or capitalized, and then amortized over a period not exceeding five years.

1.1.5. Transfer Pricing.

Argentina has OECD like transfer pricing rules26 applicable to: i) transactions with related companies, ii) transactions with parties located in tax havens; iii) transactions between Argentine residents and their permanent establishments situated abroad; iv) transactions carried out by permanent establishments situated abroad (owned by

Argentine residents) with companies incorporated in low tax jurisdictions.

In the case of exports of cereal, seeds, hydrocarbons or other commodities, with a set price in transparent markets, where an international middleman who is not the beneficial owner of the good takes part in the transaction, the best method deemed to assess the Argentine source income is the quotation of the value in the transparent market of the good on the day of shipment, or the price agreed upon with the middleman, only if this price was greater.

Under the OECD like transfer pricing rules, the Argentine party must keep and file supporting documentation with the tax authorities; it must also perform a transfer pricing study showing that its prices or profit margins on the transactions are within the comparable arm's-length prices or profit margins ranges for its activity and similar transactions. Parties in tax havens are deemed as related parties for these purposes.

Law 11 ,683, as amended by Law 25 ,795, sets forth penalties aimed at compelling taxpayers to comply with transfer pricing rules. In this sense: i) failure to file a return on the deadline is punishable with a fine of ARS 10,000 (doubled to AR$ 20,000 if committed by companies, trusts, associations, or any other entity formed in Argentina or a permanent establishment, where any of them belong to individuals or companies domiciled or located abroad); ii) failure to fulfill a formal request to file the tax return on international transactions with either related or unrelated parties, leads to a fine ranging from AR$ 500 to AR$ 45 ,000 (for taxpayers having a gross turnover exceeding AR$ 10 million, fines will range from AR$ 90,000 to AR$ 45 0,000 as of the third request). These fines may be imposed together with the penalty imposed for not filing a return at the proper time. In addition, subsequent failures to respond to requests to file the returns will give rise to additional fines; iii) a fine ranging from AR$ 15 0 to AR$ 45 ,000 is imposed on those who fail to a) supply data to the tax authorities for auditing purposes or b) maintain the documentation and any other elements necessary to justify the prices agreed in international transactions; finally iv) failure to pay tax due to having not filed a tax return or to having filed an incorrect tax return is punishable with a fine one to four times the omitted tax when referred to transactions carried out between local companies, enterprises, trusts or permanent establishments located in Argentina and persons or entities domiciled, incorporated or located abroad.

1.1.6. Inflationary Adjustments.

The deductibility of foreign exchange gains and losses was traditionally complemented (though working oppositely) by the inflationary adjustment norms. In this sense, taxpayers were conceptually allowed to net out differences incurred by foreign exchange differences with the inflationary adjustment. The current scenario reflects an anomalous situation in which, in order to optimize income, the government has maintained norms referred to foreign exchange gains and losses but has ceased to publish inflationary adjustment indexes, so that the adjustment is no longer effective. There are a number of judicial claims on this matter. The Federal Supreme Court has recently issued a ruling on this matter, establishing that the Congress had acted within its constitutional powers when it derogated all legal norms and statutes authorizing adjustments, cost variations and any other form of adjusting debts, taxes, prices, services, etc.; because of its authority to determine the value of the currency and to legislate over taxes. The Judicial Branch, according to the Supreme Court, cannot argue over the merits taken into account by Congress when exercising its powers.

However, the limit that should be applied to Income Tax remains unresolved, given that the Supreme Court decided that the effective rate resulting from the ban on inflationary adjustments (62% or 55 %) was confiscatory and therefore unconstitutional, but did not indicate where to draw the line between legality and illegality of the rate.

The majority of the Court found that the rate that was actually being charged to the plaintiff was absorbing a substantial portion of his profits and thus decided in his favor. Clear evidence of a confiscatory rate must be presented for this case law to apply in the future. Note that in Argentina Supreme Court rulings are not mandatory for lower courts and apply to the case subject to analysis. Tax planning is of the essence to avoid pitfalls and to take advantages of circumstantial opportunities.

1.1.7. Tax Loss Carry-forward.

Argentine taxpayers may carry-forward tax losses for a maximum term of 5 fiscal years. There is no carry-back possibility.

Losses arising from the sale or disposal of stock or shares may only be computed against capital gains of the same nature. Furthermore, losses arising from activities not considered to be Argentine source income may only be set off against foreign source income.

Tax losses cannot be transferred to other taxpayers (not even to the shareholders), except as provided in the cases of reorganizations.

The Argentine Tax Law allows for three types of tax-free reorganizations:

i) statutory tax-free mergers;

ii) statutory tax-free divisive reorganizations, and

iii) sales or transfers within an economic group. In these cases, and provided that a number of statutory requirements are complied with (view 1.18 "Tax Free Reorganizations") the tax attributes of the target company are transferable to the surviving or resulting corporation.

A long standing interpretation of the Argentine Tax Authorities is that the associated tax incentives –i.e. transfer of fiscal attributes (e.g. NOLs) and no recognition of gain or loss- are only granted when business reasons are attached to the restructuring, such as the improvement of production, efficiency conditions or productivity, and to optimize the use of production factors. Accordingly, tax-driven reorganizations are not allowed on a tax free basis.

Additionally, in order for the NOLs to be transferred from one entity to another in the context of a tax-free reorganization, at least 80% of the equity of the predecessor companies should have been owned by the same persons for the two years preceding the reorganization date. This is the so-called Preexisting-Identity-of-Interest Requirement.

The carry-forward period is not refreshed by the occurrence of a tax-free reorganization.

1.1.8. Tax-Free Reorganizations.

In order to qualify for a tax free reorganization, requirements are as follows:

(i) Continuity of interest: The majority of the shareholders of the companies subject to reorganization shall remain the same (i.e. a minimum of 80%), for at least two years subsequent to the reorganization date.

(ii) Identity of Activities: At the time of reorganization, the predecessor companies must be effectively performing their corporate purpose (or have ceased to perform it within the last 18 months). The nature of the activities performed by the predecessor companies during the last 12 months prior to reorganization must be identical or related to the activities performed by the surviving company.

(iii) Continuity of Activities: The reorganized company shall maintain the same or related activities of the predecessor companies, for a minimum period of two years as of the reorganization date (as defined below). The goods or services produced and/or rendered by the surviving company shall be substantially similar to the ones produced and/or rendered by the predecessor company. In fact, taking into account this requirement, the local IRS may reasonably understand that the activity to be maintained should be the one previously performed by the predecessor company.

(iv) Notification: The reorganization must be notified to the local IRS within 180 days as of the reorganization date, computed as from the date in which the reorganized entity starts performing the activities of the predecessor.

(v) Compliance with the Corporate Law requirements: the publication and registration requirements set forth by Law 19,550 must be observed.

(vi) Other requirements: Additionally, in order for the NOLs to be transferred from one entity to another in the context of a tax-free reorganization, at least 80% of the equity of the predecessor companies should have been owned by the same persons for the two years preceding the reorganization date. This is the so-called Preexisting-Identity-of-Interest Requirement.

1.1.9. Leasing Tax Treatment.

Pursuant to the amended leasing law, assets which may be subject to leasing include: movables and immovable property, patents, brand names or software.

Income Tax Treatment of assets subject to leasing ultimately depends on the type of leasing. The law provides for three different types of leasing, namely: i) contracts assimilated to financing operations; ii) contracts assimilated to renting operations; and iii) contracts assimilated to installment sales.

A contract is to have a tax treatment of a financing operation whenever the lessee is a financial entity, a financial trust or an enterprise whose main activity is the celebration of these types of contracts and the duration of the contract exceeds 50% of the useful life of the movable asset, 20% of the useful life of real estate property destined for living space or 10% of the useful life of real estate property with commercial purposes.

When a contract is deemed to have the tax treatment of a renting operation, the lessor may amortize the cost of the good, while lessee may deduct rental payments. Whenever the option to buy is exercised, the set amount will be computed as purchase cost for lessee and as sale price for lessor and subject to taxation.

A contract is deemed to have the tax treatment of a sale, whenever the price established for the sale is less than the adjusted basis of the asset for lessor at the time such option is exercised.

1.2. Foreign Exchange Gains and Losses

Since transactions are to be valued in Argentine currency for income tax purposes, fluctuations in foreign exchange currencies generate foreign exchange gains or losses. Income Tax Law provisions that govern the tax treatment of foreign exchange differences do require Argentine resident companies to account both foreign exchange gains and losses on an annual basis, disregarding whether there has been realization or not of the underlying assets or liabilities that trigger such FX results. The ITL Implementing Decree provides that taxpayers should account all FX results related to taxable transactions, as well as those resulting from credits that have been incurred to finance such business activities. Deposits, credits and debts are to be valued according to the applicable foreign exchange rate issued by the Banco de la Nación Argentina on the closing date of the fiscal year. The ITL Implementing decree impedes FXs resulting from the mere conversion of a debt denominated in one currency to another one, unless there was either a novation or the FX results were triggered by the time of payment. The goal of this provision is to prevent taxpayers from artificially manipulating foreign exchange operations, thus triggering tax losses resulting from unsubstantiated transactions in different currencies.

1.3. Payment and Filing.

For any given fiscal year the corresponding income tax return must be filed before the beginning of the fifth month following the end of the taxpayer's fiscal year. Note that for corporations the tax year must not necessarily coincide with the calendar year as is the case with physical persons. Companies, in fact, do have a fiscal year that overlaps the financial statement's year. Corporations and foreign company branches are required to make ten monthly prepayments, as from the sixth month of the fiscal year.

Prepayment amounts are established on the basis of the tax paid in the preceding fiscal year.

1.4. Penalties on Unpaid Tax or Tax Paid Belatedly.

The Tax Procedure Law ("TPL") sets forth certain penalties for incompliance with formal requirements and for incompliance with substantial obligations.

Penalties for incompliance with formal requirements are imposed on account of the following:

i) omitting presentation of sworn statement within the set period is penalized with a fine of two hundred (approximately U$S 62) to four hundred pesos (approximately U$S 124);

ii) omitting presentation of sworn statement referring to third party information (e.g. representatives of foreign incorporated companies) or provision of relevant information within the set period. An amendment to the TPL has increased fines for lack of presentation of sworn statements on the due dates to five thousand pesos (approximately U$S 1,300); the fine may be increased up to ten thousand pesos (U$S 2,600) if the taxpayer is a corporation, trust, or any other type of entity incorporated in Argentina or a foreign owned local company.;

iii) close down of businesses, which may be applied on certain establishments, offices or stores offering goods and services for values exceeding AR$10, and not delivering invoices; for lacking registry books, for requesting or delivering merchandise without the documentary backups or when the taxpayer is not registered as such before the local revenue service.

Amongst penalties for incompliance with substantial obligations: i) tax omission is fined with a penalty from 50%-100% of the omitted tax, whenever the omission is by means of: a) lack of presentation of sworn statement; b) when the sworn statement is inexact; c) withholding agents failing to act as such; ii) furthermore, the TPL sets the penalty for tax fraud at 2 to 10 times the amount of the evaded tax.

The fine amounts may be reduced whenever the incompliance is not repeated and upon rectification or voluntary filing of the tax.

The Penal Tax Law also sets forth that in the case of tax fraud the taxpayer may face 2 to 9 years of prison, depending on the evaded amount and whether third parties or supposed exemptions were used to evade the tax. Interest rates are 2 % monthly and punitive interest rates are 3 % monthly.

1.5. Dividends Tax / Branch Profits Tax.

The distribution of dividends, profits or branches' remittances are generally not subject to taxes in Argentina. Exceptionally and whenever such profits are distributed in excess of a company's net taxable income a withholding rate of 35% is applied (i.e. equalization tax).

1.6. Cross-border Payments

1.6.1. Withholding Taxes

When Argentine source income is remitted abroad to a beneficiary that is a nonresident alien individual or entity, the payment should be subject to a withholding tax. In any of the cases set forth below, if the local payer assumes the obligation to pay the tax for the non-resident recipient, then the net amount must be grossed up in the amount of the tax. Note that the withholding rates set forth below are applicable in the absence of a pertinent double tax treaty.

1.6.1.1. Dividends

If the corresponding profits were taxed at the corporate level then no income tax withholding applies. However, if such profits were not taxed a withholding of 35% applies on account of equalization tax.

1.6.1.2. Royalties.

Royalty payments on account of agreements complying with the Copyright Law are subject to a 12.25%/ 13.96% (with grossing up) withholding tax.

1.6.1.3. Technical Assistance, Engineering and Consulting Services.

If the given contracts refer to services deemed unavailable in Argentina and provided that the contract is registered before the National Institute of Industrial Property ("INPI") according to Transfer of Technology Law, such agreements are subject to a withholding of 21% (26.58% with grossing up). If the contracts are registered pursuant to the Transfer of Technology Law but the given contract is not included amongst the above, then a withholding rate of 28% applies (38.89% with grossing up). Unregistered transfers of technology are subject to 31 .5% withholding.

1.6.1.4.Interest on Loans obtained abroad.

Interest payments on loans obtained abroad are subject to a withholding rate of 35% (53.85% with grossing up). However, if the beneficiary is a bank or financial institution incorporated in a country not considered to be a low tax jurisdiction, or in a jurisdiction which signed agreements providing for the exchange of information and where bank secrecy or secrecy referring to stock exchange cannot be alleged upon request of information by the pertinent tax authorities, then the withholding rate is reduced to 15.05% (17.72% with grossing up).

1.6.1.5. Payments to non-residents:

Payments to non-residents working on a temporary basis in Argentina for a period not exceeding 6 months are subject to a withholding of 24 .5% (32 .45 % with grossing up).

1.6.1.6. Rental Payments on moveable property:

are subject to a withholding rate of 14% (16.28% with grossing up).

1.6.1.7. Rental Payments on real estate property:

are subject to a withholding rate of 21% (26.58% with grossing up).

1.6.1.8. Proceeds from the sale of any type of property:

are subject to a withholding rate of 17.5% (21.21% with grossing up).

1.6.1.9. Others:

The general withholding rate applicable to other cross-border payments not included within those mentioned above are subject to a general withholding rate of 31.5% (45.99% with grossing up).

2. Value Added Tax (VAT)

2.1. General Aspects

2.1.1. Tax Rates.

The general VAT rate is 21%. There are reduced and increased rates for certain goods and services; e.g., a 10.5% rate applies on passenger transport services, health care and certain interest payments, amongst others and an increased rate up to 27% applies on telecommunications amongst others).

There are also some VAT exemptions for specific public entities of the national or local territorial level and for private schools, religious institutions, transportation for less than 100 km, and rent of housing for personal use and of land for agricultural purposes, amongst others.

Moreover, a "technology tax" was passed increasing the rate from 10.5% to 21% of imported technology-related goods considered as "luxury products". Hence, for enterprises engaged in the business of technological importation, the digital, technological and electronic assets considered as "luxury assets" under the tax reform, would be taxed at a higher rate within the VAT, whilst the ones manufactured in the territory of Tierra del Fuego would be exempted.

2.1.2. Taxable Transactions.

Transactions subject to VAT are the sale of goods and the provision of services in Argentina and the importation of goods.

In some cases, services rendered outside Argentina are deemed as subject to VAT because they are effectively used or exploited in Argentina. Imports of services are taxable when the importer is a VAT taxpayer.

VAT is paid at each stage of the production or distribution of goods and services on the value added during each of the stages.

2.1.3. Taxable Base.

The taxable base is the price or value of the consideration paid for the goods or services.

2.1.4. Creditable VAT .

As a general rule the VAT taxpayer has a right to credit against payable VAT all VAT indicated in the invoices of the suppliers of goods and services contracted by the taxpayers.

The VAT paid in the acquisition of goods that the company destines to exempt operations is not creditable against VAT. Acquisition of cars, services rendered by restaurants and hotels are not creditable against VAT either.

2.2. Selected VAT Incentives.

These are some VAT incentives selected among the many incentives available in the VAT law:

2.2.1 VAT Incentive for Purchase of New Capital Assets.

There is a special VAT regime applicable to the acquisition and import of capital assets. Law 24 ,402 provides a financing possibility for the payment of fiscal credit corresponding to the acquisition of capital assets whenever these are to be applied to the productive process destined to the sale in the external market. The applicable entity may receive a financing equivalent to the fiscal credit. The financing is received through a bank or

financing entity, which is later repaid by the state in the applicable amount.

During 2008 new incentives were granted for the acquisition and import of capital assets for the industry as well as infrastructure projects. Law 26.360 provides for either an accelerated recovery of VAT input credits or accelerated depreciation for Income Tax. This benefit may not overlap the ones of Law 24.402.

2.2.2. Investments on Mining Activity.

Investments on physical infrastructure for the mining industry also benefit from the financing possibility set forth in Law 24,402 (later amended by Law 25.429).

2.3.Payment and Filing

VAT returns must be filed on a per month basis. In the case of definitive imports, the tax is determined and paid along with custom duties.

3. Other Taxes

3.1. Minimum Presumptive Income Tax

This is a 1% tax levying company assets (liabilities cannot be deducted). Some assets are tax-exempt, e.g. stocks and other capital share of other entities subject to taxation, or assets of mining companies. The acquisition of new fixed assets –except for automobiles- as well as investments in the construction of new buildings or refurbishing (for the first two years) is excluded from this tax.

IT determined for the same fiscal year is considered payment on account of MPIT provided the income tax obligation does not exceed the amount of the presumed minimum income tax. Otherwise the excess of income tax does not constitute a tax credit.

The excess minimum presumed income tax of a given year over the income tax liability may be carried forward to offset income taxes for ten years.

3.2 Gross Turnover Tax

The Gross Turnover Tax is a local tax applicable on gross income. Although as a local tax the provinces and the City of Buenos Aires set the tax rates, most jurisdictions apply a 1% tax rate on agriculture, cattle ranching and mining activities; a 1.5% tax rate on industrial activities, a 3% tax rate on trade and services and a 5.5% on financial activities. The different jurisdictions have signed an agreement (the "Multilateral Agreement") in order to avoid double taxation whenever activities subject to taxation have been carried out in more than one jurisdiction. The Multilateral Agreement sets forth a formula in order to allocate income between the different provinces.

3.3. Property Taxes

This tax levies the transfer of property rights referred to Argentine real estate property and provided that the owners are physical persons (resident or non-resident) or undivided estates. The tax rate is 1.5% and the tax applies whenever the transaction has not been subject to income tax.

3.4. Debits and Credits in Bank Accounts Tax

This tax is a national level tax withheld by Argentine banks (and other savings institutions). It applies on any deposited funds that are either withdrawn or transferred from checking or savings account. The taxable base is the amount withdrawn or transferred. The tax rate is 6 per thousand. There are very limited exemptions. The tax rate gets doubled in set cases where the elusion of the use of banks accounts is deemed to take place. This tax is partially creditable against other Federal Taxes.

3.5. Stamp Tax

The Stamp Tax is a local tax levying the instrumentation of onerous contracts. In the City of Buenos Aires,27 the tax applies on all contracts and monetary operations as of 1.1.09. Although the rate may vary from jurisdiction to jurisdiction, the general rate is 1% (except in the sale of real estate property where the rate is increased in most jurisdictions to about 4%). The tax is paid by means of sworn statements or fiscal stamps. During 2004, several Federal Supreme Court rulings28 have decreed the inapplicability of the tax whenever acceptance of the contract takes place through unwritten means (e.g. the written offer provides that the contract will be considered accepted if the party performs a certain activity).

3.6. Personal Assets Tax

The Personal Assets Tax ("PAT") is a tax levied on the non-productive assets held by physical persons or undivided estates domiciled in Argentina by December 31, both within the country and abroad. The tax rates vary according to the following schedule: (i) from AR $ 305,000 to AR $750,000 the tax rate is of 0.5%; (i) for assets valued from AR $ 750,000 to AR $ 2,000,000 the tax rate is 0.75%; (iii) for assets valued from AR $ 2,000,000 to AR $ 5,000,000 the tax rate is 1%; and (iv) for assets valued over AR $ 5,000,000 the tax rate is of 1.25%. Taxable assets include both assets held within the country and abroad. Foreign residents shall be subject to a 1.25% rate on the value of all their assets held in Argentina; except for shares and equity holdings in Argentine companies, which are taxed differently.

Non-resident aliens, in general, are subject to an annual 0.5% levy on the net-equity value of their participations in Argentine companies and branches of foreign entities. The same tax applies on Argentine resident individuals -other than local companies who are required to exclude their equity participations in Argentine companies from their annual PAT tax returns. The companies, who issued the stock or shares, or the branches, as the case may be, are responsible to collect and pay the tax to the government. In turn, such withholding agents are entitled to a refund from the equity holders.

3.7. Tax on Donations and on Free Transfer of property in the Province of Buenos Aires.

Any increase in the assets of a person or company domiciled in Buenos Aires over 3 million Argentine Pesos due to a free transfer of property is now taxed at a rate of 5 to 10.5 depending on value of the assets transferred. Donations, legacies, inheritances, anticipated inheritance, are only a few examples of what the law considers a free transfer of property.

4. Customs Regime –General Aspects

4.1. Custom Duties

Importation of goods and the rendering of services abroad which are effectively utilized in Argentina are subject to import VAT at a general rate of 21% plus 10.5% VAT withholding and 3% Income Tax withholding. In addition to import VAT, imports of goods are also subject to custom duties that range between 0% and 35% (i.e. standard ones), also depending on the type of asset imported, and except for assets with special treatment. The Ministry of Economic Affairs may alter rates and does so frequently. Other taxes include a statistics tax, established on the CIF value of the good and excise taxes.

4.2. Taxable Base

As a member of the WTO and having subscribed the Agreement for the Application of Section VII of the GATT, the value of the goods is established on account of the price paid. If this is not possible, other methods of valuation and the corresponding adjustments are applied. Duties are computed on the CIF value of the goods.

4.3. Transfer Pricing

Custom valuation rules are those of the GATT (1994) valuation code

4.4. Filing and Payment

An import return must be filed and the pertinent tax must be paid before the good is nationalized.

4.5. Selected Custom Duties Regimes Available

There are several importation regimes applicable in Argentina:

4.5.1. Ordinary Importation Regime.

It applies to all goods that will remain permanently in Argentine territory without any use or jurisdictional restrictions. Full payment of custom duties and import VAT is required upon nationalization.

4.5.2 Temporary Importation Regime.

It applies to merchandise that is to remain in the country for a given set period of time and with a determined purpose. Once the finality has been fulfilled and thetime span has passed, the asset must be re-exported.

The assets imported under the temporary regime may:

a) remain in the same state. In this case, the maximum term of the temporary import regime depends on the good, but in general is up to 3 years for capital assets and 3 or 8 months for other goods (this would have to be checked on a case by case basis); or

b) be subject to an industrial process of transformation. In this case, the temporary import regime lasts for 1 year (which may be extended for an additional year).

Goods generally subject to this regime include: machinery and equipment for a trial period or for controlling purposes; machinery or equipment for expositions or congresses; vehicles for sporting events; vehicles and other assets to be used by nonresidents in the country.

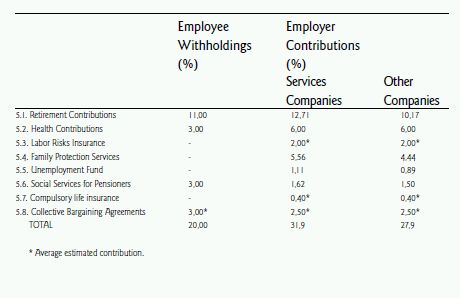

5.Payroll Taxes / Welfare Contributions

Employees are liable for Social Security taxes upon their salaries. Employers are designated withholding agents, thus, at the moment salaries are calculated corresponding withholdings are performed and taxes are paid to competent authorities directly by employers. On the other hand, employers are liable for contributions. Both withholdings and contributions are collected and paid monthly on the basis of the gross remuneration.

5.1. Retirement Contributions

The employee contributes to public pension funds. The employee's withholding for retirement funds equals to 11%, calculated on the employee's wage. This withholding is deposited in a public account of a government agency. Employers whose main activity is to hire or provide services must also contribute to the social security system for retirement funds in an amount equivalent to 12.71% of the monthly wage paid to the employee. Any other employer must contribute to the social security system for retirement funds in an amount equivalent to 10.17% of the monthly wage paid to the employee.

Employees' withholdings in relation to this item have a ceiling: of AR$10,119.08.

5.2. Health Contributions

The employee must be affiliated to general Health Care Plan ("HCP"). Contributions to the HCP administering entity must be equal to 9% of the employee's wage, 6% of which is paid by the employer while the remaining 3% is contributed by the emplo- yee. The employer is responsible for withholding the employee's corresponding 3% and for paying the HCP administering entity 100% of the monthly health contribution. Employees' withholdings contributions for Health Insurance have a ceiling of AR$ 10,119.08.

5.3. Labor Risks Insurance System

Companies must also purchase insurance for labor risks which exclusively refer to labor accidents and a limited number of labor related illnesses. In certain cases, and provided certain conditions are met, the company may opt to self-insure.

The applicable law establishes that, having complied with the referred system (mainly by duly paying the cost of insurance) exempts the employer from civil responsibility, provided no intentional tort by the employer is proven. However, the constitutionality of the norm has been contested ever since its promulgation and a Supreme Court ruling has decreed the unconstitutionality of the referred norm.29 It is important to note that -regardless of the influence this ruling may have on lower court decisions- in Argentina, Supreme Court case law is not mandatory and is applicable only to the case under analysis.

The cost of labor insurance may vary from 1% to 3% depending on the insuring company, and on other parameters such as the type of activity involved, number of workers, etc.

Employer contributions to Labor Risks Insurance System have a ceiling of AR$10,119.08.

5.4. Contributions to Family Protection Services

The employer whose main activity is to hire or provide services must make a contribution equivalent to 5.56% of the monthly wage paid to the employee on account of family protection services. Any other employer contributes to this fund with 4.44% of the employee's salary.

5.5. Unemployment Fund Contribution

During the employment relation, the employer whose main activity is to hire or provide services must contribute an amount equal to 1.11% of the employee's salary to an unemployment fund. Any other employer contributes to this fund with the 0.89% of the employee's salary.

5.6. Social Services for Pensioners

The employer must contribute 1.62% -if its main activity is to hire or provide services- or 1.50% of the employee's salary to the National Institute for Social Services for Pensioners. The withholding of the employee adds up to 3%.

5.7. Compulsory Life Insurance

Employers are compelled to hire a compulsory life insurance in favor of their employees in accordance with Decree 1567/74 and Resolution (SSN) 33860. At present the premium is equal to AR$ 0,205 for each AR$ 1,000, and the assured amount is equal to AR$ 6,750 (subject to modifications introduced by the National Insurance Superintendence). Employers are directly liable for the payment of compensations in cases in which such insurance was not timely hired or is deficient. Designation of beneficiaries of the insurance is performed by the employee at the commencement of the employment relationship.

5.8. Taxes and Contributions pertaining to applicable Collective Bargaining Agreements

A series of Collective Bargaining Agreements establish contributions in favor of the signatory Trade Unions of such Agreements. Contributions may correspond to the employer, the employee, or even both of them. An average contribution rate amounts to 3% of the employees' gross salary or wage.

Synthesis

The following chart exposes a synthesis of Payroll Taxes and Welfare Contributions in Argentina..

Footnotes

1 Dividends and profits distributed by local branches are not subject to tax in Argentina, except for those distributed in excess of the company's net taxable income which are subject to an equalization tax of 35%.

2 Except for commodities, tested party rules and other set exceptions.

3 There are lower and higher differential rates, as set forth below.

4 Goods subject to excise taxes are: leaded and unleaded fuel (62%-70%); cigarettes (60%), alcoholic beverages (4%-25%), cars and certain engines (10%); insurances (0.1%-23%); among others. The National Congress has recently passed a law which taxes with Excise Taxes at a 17% rate the digital, technological and electronic assets considered as "luxury assets".

5 An increased rate of 1.2% applies whenever there has been substitution for the use of a checking account. Partially creditable against other Federal Taxes.

6 This rate applies on the equity interest Argentine individuals and non-residents have in Argentine incorporated entities and local branches. In other cases, the rate schedule varies from 0.5% up to 1.25%, depending on the value of the taxable assets.

7 Reference is made to the most usual rates, but other rates may be applicable in certain jurisdictions.

8 If they are franked, according to Australian income tax laws and subject to a maximum of 15% in other cases. Note that in Argentina dividend distribution is generally not subject to tax.

9 In Belgium, the tax may not exceed 10% of the dividends if the beneficial owner is a company holding at least 25% of the capital and 15% in other cases. Note that in Argentina dividend distribution is generally not subject to tax.

10 This treaty does not establish specific limits on the taxes but rather specifies which country has jurisdiction to impose taxes.

11 This treaty does not establish specific limits on the taxes but rather specifies which country has jurisdiction to impose taxes.

12 In Canada, the tax may not exceed 10% of the dividends if the beneficial owner is a company holding at least 25% of the capital and 15% in other cases. Note that in Argentina dividend distribution is generally not subject to tax.

13 This treaty does not establish specific limits on the taxes but rather specifies which country has jurisdiction to impose taxes.

14 In Denmark, the tax may not exceed 10% of the dividends if the beneficial owner is a company holding at least 25% of the capital and 15% in other cases. Note that in Argentina dividend distribution is generally not subject to tax.

15 In Finland, the tax may not exceed 10% of the dividends if the beneficial owner is a company holding at least 25% of the capital and 15% in other cases. Note that in Argentina dividend distribution is generally not subject to tax.

16 The 10% limit applies if the interests arise from bank loans or from sales of commercial or industrial equipment. The 15% limit applies in all other cases.

17 In Great Britain, the tax may not exceed 10% of the dividends if the beneficial owner is a company holding at least 25% of the capital and 15% in other cases. Note that in Argentina dividend distribution is generally not subject to tax.

18 In the Netherlands, the tax may not exceed 10% of the dividends if the beneficial owner is a company holding at least 25% of the capital and 15% in other cases. Note that in Argentina dividend distribution is generally not subject to tax

19 In Norway, the tax may not exceed 10% of the dividends if the beneficial owner is a company holding at least 25% of the capital and 15% in other cases. Note that in Argentina dividend distribution is generally not subject to tax.

20 The Treaty is yet awaiting notification of Russian government. It will enter into force on the subsequent date on which the Russian government notifies the Argentine government that all Russian internal proceedings for DTT approval are duly fulfilled. This is expected to happen soon.

21 In Russia, the tax may not exceed 10% of the dividends if the beneficial owner is a company holding at least 25% of the capital and 15% in other cases. Note that in Argentina dividend distribution is generally not subject to tax.

22 In Spain, the tax may not exceed 10% of the dividends if the beneficial owner is a company holding at least 25% of the capital and 15% in other cases. Note that in Argentina dividend distribution is generally not subject to tax.

23 In Sweden, the tax may not exceed 10% of the dividends if the beneficial owner is a company holding at least 25% of the capital and 15% in other cases. Note that in Argentina dividend distribution is generally not subject to tax.

24 The Treaty was signed in 1997; however, it was not approved by Congress, reason for which the Treaty was approved three years later by the Argentine Executive through an exchange of notes with Swiss representatives. An additional protocol signed on November 23rd, 2000 put the DTT temporarily in full force and effect. The Additional Protocol stated the DTT would apply on a provisional basis as of January 1st, 2001. The status of the Treaty under the Vienna Convention

of Laws of Treaties of 1969 ("Vienna Convention") and under Argentine law, as of the 1994 Constitutional Amendment has been debated; although in practice the Treaty continues to be applied. In August 2006 significant amendments to the original treaty were made through a new protocol. However, despite the confusing terms of the Protocol, it will apparently come into effect once the Argentine congress finally approves the Treaty.

25 In Switzerland, the tax may not exceed 10% of the dividends if the beneficial owner is a company holding at least 25% of the capital and 15% in other cases. Note that in Argentina dividend distribution is generally not subject to tax.

26 Except for transactions with commodities, tested party rules and other set exceptions.

27 Note that the City of Buenos Aires is an autonomous jurisdiction with taxing powers similar to that of the provinces.

28 See CSJN,15.04.2004, "Shell Compañía Argentina de Petróleo c/ Neuquén, Provincia de s/ acción de inconstitucionalidad", and CSJN, 15.04.2004, "Transportadora de Gas del Sur S.A. (TGS) c. Provincia de Santa Cruz".

29 "Castillo, Ángel Santos c/ Cerámica Alberdi S.A. s/ recurso de hecho deducido por La Segunda Aseguradora de Riesgos del Trabajo S.A.", 09.07.2004

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.